Download

1 / 36

360 likes | 576 Views

Options. Stefano Grazioli. Critical Thinking. Last BI homework Course pack Lab at normal hour on Fri Easy meter. BI in Action. Homework. Divisions (e.g., Asia) Departments (e.g., Accounting) Categories (e.g., Compensation) Items (e.g., Bonuses) Month. You Are a Business Analyst….

E N D

Options Stefano Grazioli

Critical Thinking • Last BI homework • Course pack • Lab at normal hour on Fri • Easy meter

BI in Action Homework

Divisions (e.g., Asia) Departments (e.g., Accounting) Categories (e.g., Compensation) Items (e.g., Bonuses) Month You Are a Business Analyst… We need to figure out why we missed our global budget for the year… please find any significant variations between budgeted costs and actual costs… get the data from the DW and prepare a report on what you find We should be doing this every month…

A Data Warehouse (DW) is a database that is designed for informational use: • Subject-oriented (e.g., budget) • Integrated (e.g., across branches) • Time variant • Non-volatile DWfor ACME

Inside a DW • Star Schema • “Fact Table” Fact table: contains basic measures Dimension table: contains categorizations

The Homework Dimension: Category Dimension: Organization Item • Category Department • Division Fact Table Department Item Month Budget Actual Dimension: Time “Flat” file to you Month

BI in Action Demo

Suggestions • Give yourself plenty of time • “Play” with the pivot table, figure out how it works by trial and error

Options An introduction(spans two lectures)

Managing Risk Risk Mitigation Auditing Disaster planning Business continuity Riskmanagement Insurance Hedging & Options Diversification

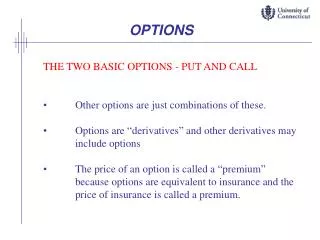

Option is a contract giving the buyer the right, but not the obligation, to buy or sell an underlying asset (for example a stock) at a specific price on or before a specified date • Options are derivatives.

CBOE trades options on 3,300 securities.More than 50,000 series listed. 1/4 of US option trading 4.4 million contracts, $2.3Bil. value traded per day Hybrid market: 97% total (68% volume)is electronic CBOE Source: CBOE & OCC web site

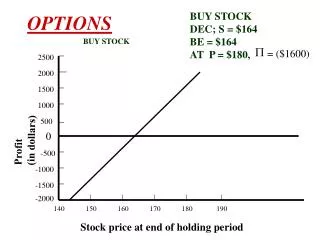

Example Scenario • You own 100,000 GOOGLE stocks. • @ $1,200 -> $120,000,000. • You are pretty happy. • But you are also worried. What if the price drops to $1,000? • You need some kind of insurance against that. • Somebody is willing to commit to buying your GOOGLE stock at $1,200 (if you want), two years from now. • But she wants $10 per stock. Now. • You decide that it is a good deal. So, you buy 100,000 contracts that give you the choice to sell your stock at the agreed price two years from now. • You have bought 100,000 put options.

Put Options • A put option gives to its holder the right to sell the underlying security at a given price on or before a given date. • "Insurance" analogy

Types of Traders • Speculators • Arbitrageurs • Hedgers (us)

Another Scenario • You are an executive at the Coca Cola Company. • You make $1,000,000 a year. • You are pretty happy. • The Board wants to make sure that you will do your best to keep the price of the CocaCola stock up. • Rather than giving you a well-deserved raise, they offer to you a deal. They promise that in three years they will give you the chance to buy 200,000 stocks at $40. • Right now the stock is valued at $40. • If the company does well, the stock price could go as up as $50. • So you think: “In three years I could just get my 200,000 @ $40 and then immediately sell them back to the market for $50....” • You conclude that an extra $2,000,000 in your pocket is a good thing. • You have been given 200,000 call options.

Call Options • A call option gives to its holder the right to buy the underlying security at a given price on or by a given date • "security deposit" analogy

Call Option can buy 1 IBM stock@ $180.00 on 5 Mar 2014 Nomenclature option price = premium underlier IBM Stock Price: $185.00 Put Option can sell 1 IBM stock@ $190.00 on 18 Apr 2014 strike price “spot” (i.e., market) price expiration:European vs. American

Call Option can buy 1 IBM stock@ $180.00 today Call Option can buy 1 IBM stock@ $185.00 today Call Option can buy 1 IBM stock@ $190.00 today Nomenclature In the money IBM Stock Spot Price: $185.00 At the money Out of the money

WINIT What Is NewIn Technology?

Options Valuation

Evaluating Options • On expiration day, value is certain and dependent on (= strike – spot) • On any other dayvalue is not deterministic,because of uncertaintyabout the future. ?

The current value of a Put Option depends on: 1) the current price of the underlier -2) the strike price +3) the underlier volatility +4) the time to expiration +5) the risk-free interest rate - Evaluating PUT Options Question:what is the valueof the optionright now? Bought a put option on IBM for $1x = $200 Put Option:Can sell IBM for $200 IBM’s price is $205 a) IBM’s market price is $190 b) IBM’s market price is$210 PAST NOW EXPIRATION

P = –S[N(–d1)] + Xe-rt[N(–d2)] d1 = {ln(S/X) + (r + s2/2)t} st d2 = d1 - st P = value of a European put option, S = current spot price, X = option “strike” or “exercise” price, t = time to option expiration (in years), r = riskless rate of interest (per annum), s= spot return volatility (per annum), N(z)= probability that a standardized normal variable will be less than z. In Excel, this can be calculated using NORMSDIST(d). Delta for a Call = N(d1) Delta for a Put = N(d1) -1 The Black-Scholes Formulas

Example: S = $ 42, X = $40t = 0.5r = 0.10 (10% p.a.)s = 0.2 (20% p.a.) Output: d1 = 0.7693d2 = 0.6278N(d1) = 0.7791N(d2) = 0.7349C = $4.76 and P=$0.81 Formulas

BS Assumptions • Unlimited borrowing and lending at a constant risk-free interest rate. • The stock price follows a geometric Brownian motion with constant drift and volatility. • There are no transaction costs. • The stock does not pay a dividend. • All securities are perfectly divisible (i.e. it is possible to buy any fraction of a share). • There are no restrictions on short selling. • The model treats only European-style options.

The current value of a call Option depends on: 1) the current price of the underlier +2) the strike price -3) the underlier volatility +4) the time to expiration +5) the risk-free interest rate + Evaluating Call Options Question:what is the valueof the optionright now? Bought a call option for $2.00, x=40 Call Option:Can buy CocaColafor $40 CocaCola’s price is $40 a) CocaCola’s price is $45 b) CocaCola’s price is $35 PAST NOW EXPIRATION

C = S[N(d1)] – Xe-rt[N(d2)] d1 = {ln(S/X) + (r + s2/2)t} st d2 = d1 - st C = value of a European call option S = current spot price, X = option “strike” or “exercise” price, t = time to option expiration (in years), r = riskless rate of interest (per annum), s = spot return volatility (per annum), N(z)= probability that a standardized normal variable will be less than d. In Excel, this can be calculated using NORMSDIST(z). Delta for a Call = N(d1) Delta for a Put = N(d1) -1 The Black-Scholes Formulas

Market Mechanics • Market listed: bid & ask • Buyer & seller: holder & writer • Long & short positions • Blocks of 100 – NOT FOR THE TOURNAMENT • Option class: defined by the underlier and type • Option series: defined by an expiration date & strike example: APPL May Call 290 • Expiration: Sat after the 3rd Friday of the month • America vs European (TOURNAMENT) • Transaction costs: commissions on trading and exercising.

You do the talking • Name, Major • Objectives from the class • Things you like about the class • Things that can be improved • Strengths / Attitude towards the Tournament