Download

1 / 30

300 likes | 474 Views

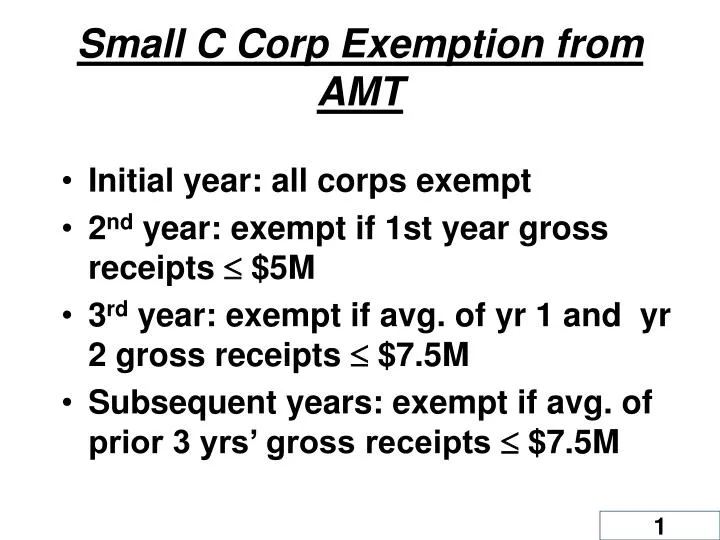

Small C Corp Exemption from AMT. Initial year: all corps exempt 2 nd year: exempt if 1st year gross receipts $5M 3 rd year: exempt if avg. of yr 1 and yr 2 gross receipts $7.5M Subsequent years: exempt if avg. of prior 3 yrs’ gross receipts $7.5M. Definitions (1 of 2).

E N D

Small C Corp Exemption from AMT Initial year: all corps exempt 2nd year: exempt if 1st year gross receipts $5M 3rd year: exempt if avg. of yr 1 and yr 2 gross receipts $7.5M Subsequent years: exempt if avg. of prior 3 yrs’ gross receipts $7.5M

Definitions(1 of 2) • Alternative minimum taxable income • Tax base for AMT prior to applying the statutory exemption • Statutory exemption amount • $40,000 • Reduced by 25% x (AMTI - $150,000) • Fully phased out when AMTI ≥ $310,000

Definitions(2 of 2) • Tentative minimum tax • Tax liability based on AMTI less AMT exemption and AMT tax rate • Reduced by AMT FTC • Regular tax • Regular income tax liability less FTC and possessions credits • AMT • TMT less regular tax

Problem C:5-36a Preadjustment

Problem C:5-36b Preadjustment Preadjustment

Problem C:5-36c and d Preadjustment Preadjustment

Problem C:5-36 e &f This formula is far too simple; as the TMT goes down, the regular tax normally increases.

Tax Preference Items(1 of 2) • Preference items always increase AMTI • Include the following • Excess depletion • Depletion deduction – adj. depletable basis • Intangible drilling cost deduction less 65% of net income from such property

Tax Preference Items(2 of 2) • Include the following (continued) • Tax exempt interest of certain private activity bonds • Excess of ACRS over straight-line depreciation on real estate

Adjustments to Taxable Income(1 of 3) • May increase or decrease AMTI • Depreciation • Different methods and/or recovery periods used to compute AMTI • Basis calculations • AMT basis based on AMT depreciation

Adjustments to Taxable Income(2 of 3) • Installment sales • Corp may use installment method for noninventory property • Long-term contracts • Must use % of completion for AMT • Loss limitations • At-risk and passive activity losses must be computed using AMTI

Adjustments to Taxable Income(3 of 3) • NOL deductions • Must use AMT NOL • U.S. production activities deduction • Different computation for AMT

Adjusted Current Earnings (ACE) Adjustment • ACE based on E&P concept • Adjustment • (Preadjustment AMTI – ACE) X 75% • Make all positive adjustments • Negative adjustments • Only when ACE < AMTI • Limited to cumulative net positive and negative adjustments • Cannot have a cumulative net negative adjustment

AMT Formula(1 of 3) Taxable income before NOL + Tax preference items +/- Adjustments to taxable income other than ACE adjustment and AMT NOL deduction (see TR C5-1) = PreadjustmentAMTI

AMT Formula(2 of 3) Preadjustment AMTI +/- 75% of difference between pre- adjustment AMTI and ACE - AMT NOL deduction = AMTI before US prod activity ded - Adj for US prod activity ded = AMTI

AMT Formula (3 of 3) AMTI - Statutory exemption (max $40,000) = Tax base x 20% tax rate = Tentative minimum tax before credits - AMT FTC = Tentative minimum tax (TMT) - Regular income tax liability = AMT due (if any)

Minimum Tax Credit Corp may take a credit in future years for AMT paid in previous years if computed regular tax less all non-refundable credits is larger than that year’s TMT

Compliance and Procedural Considerations • Alternative minimum tax • Form 4626 • Review the comprehensive example on page 5-13 and compare with filled-in forms in Appendix B.

Financial Statement Implications • SFAS No. 109 requirements for accounting for AMT in fin stmts • Measure deferred taxes using regular tax rate • Measure total DTA for min tax credit arising from AMT • Reduce DTA for min tax credit by valuation allowance if “more likely than not” standard met See Textbook Pg. 5-38 (compare with NOL)