Download

1 / 31

310 likes | 392 Views

The Tax Levy Cap and Its Implications for School Budgets. January 2012. The Board of Education supports tax relief. The Board has consistently sought to develop prudent budgets that reflect an appreciation of the need to limit increases in property taxes.

E N D

The Tax Levy Cap and Its Implications for School Budgets January 2012

The Board of Education supports tax relief. The Board has consistently sought to develop prudent budgets that reflect an appreciation of the need to limit increases in property taxes. The tax levy cap does not offer meaningful solutions to address the biggest cost drivers in school district budgets.

The Tax Levy Cap is NOT… • A limit on the tax increase in dollars that an individual property owner might pay • A limit on assessment changes • A direct control on the tax rate • An end to voting on school budgets • A 2% cap on property tax increases or any tax increase • A one-year issue • An effective way to control costs and ensure high quality

Property Tax Levy Cap • Not exactly a “cap” • Instead, requires a high level of voter approval (“supermajority”) if the proposed property tax levy increase goes beyond the “tax levy limit” • “Supermajority” = 60% of voters must approve • There is an 8-step formula for determining the “tax levy limit"

What Is Exempt from the Tax Levy Limit? • Debt service for capital projects (bonds) • Pension contributions rate increases above 2% (This year’s TRS rate increase is 1.2%, and the ERS rate increase is 2.6%. Only .6% of the ERS increase is exempt.) • Extraordinarily high legal settlements (Garden City has no such settlements.) • There are also 2 “adjustments” that can be made to the district tax base calculation • Tax base growth factor: adjusts for increases in “brick and mortar” development -- actual growth in the number of properties in the school district, not increases in property value. Garden City has no growth factor for 2012-13 • Costs and/or savings from the transfer of function(s) from one local government to another, to be determined by the Office of the State Comptroller (OSC ) Garden City has not been advised of any transfer of function changes

School District Tax Levy Cap vs. Other Government Tax Levy Caps • The School District increase may differ from the Village increase • The School District cannot initiate special fees (for athletics or clubs, for example) to supplement revenues provided by property taxes • Only school districts are required to have their budgets approved by a majority—or supermajority—of voters • Other municipalities need have only a majority—or supermajority—of the “governing body”

It is likely that many school districts and other levels of government will present budgets that exceed the 2% figure that is now commonly associated with the tax levy cap. This will be accomplished not by manipulating loopholes, but by following the law as it was intended.

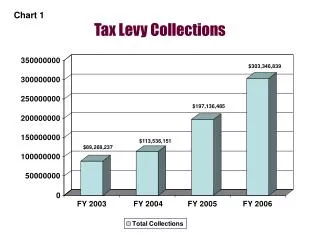

Hypothetical ‘Capped’ Garden City Public Schools Budget(in millions) • Year 06-0707-0808-0909-1010-1111-12 • Budget $85.37 90.44 94.51 95.22 97.99 101.12 • Tax Levy $76.67 79.81 83.71 85.02 88.58 90.65 • 2% Cap 78.21 79.77 81.37 82.99 84.65 • Reduction: • 1 Year $(1.60) (3.93) (3.66) ( 5.59) ( 6.00) Cumulative $(1.60) (5.54) (9.19) (14.78) (20.78) • Had the tax levy cap been in effect over the last five years, over $20,000,000 less in available resources would have been available to be used for school district programs!

Budget Vote • The property tax levy cap establishes a threshold for the minimum level of voter approval required to adopt the budget. • Is the Board of Education allowed to propose a budget that would require a tax levy increase that exceeds the tax levy limit? • Yes, the Board of Education can propose a budget with a greater increase, but for such a budget to pass, a simple majority (more than 50% of votes cast) would not be sufficient • Instead, the budget would have to pass by a “supermajority” of at least 60% of votes cast

Budget Vote Options Summary • What options does the Board of Education have regarding the budget vote? • Option 1: Propose a budget requiring a tax levy at or below the tax levy cap. The tax levy increase could be higher than 2%. Majority vote required for passage. • Options 2: Propose a budget requiring a tax levy that exceeds the tax levy cap: • Requires a “supermajority” of 60% for passage • Requires a statement on the ballot indicating that the tax levy exceeds the cap

What Will Happen If The Budget Is Not Approved? • If the budget proposal is not approved at the May vote, the Board of Education would have 3 options: • Adopt a contingency budget (“austerity budget”) immediately, with all the restrictions a contingent budget imposes • Schedule a second vote for June with a budget that is within the tax levy limit. This would require a majority vote for approval. • Schedule a second vote for June with a budget that still exceeds the tax levy limit. The would require a 60% “supermajority” for passage.

If the Budget Is Not Approved… • If the budget proposal is not approved, a contingency budget (“austerity”) must be put into place. It does not matter if the original budget proposal was “over” or “under” the cap. • The contingency budget may not include a tax levy higher than the prior year’s levy. The cap would be 0% • The property growth factor and the pension, bond interest and tort exemptions would not apply in a contingency budget, resulting in even steeper reductions than originally anticipated • In Garden City’s case, this would mean that the district could raise through property taxes no more revenue than raised for the current school year (approximately $87.3 million) • All previously enforced contingent budget rules would still apply

Challenges for the School District Budget Educational Plan Expenditure Plan Revenue Plan 21

Challenges for the School District Budget • Garden City relies extensively(90%) on property taxes for the funds that allow it to operate its programs. • Eligible for little federal aid, and these grants have been declining in value • State aid provides only 4.40% of total revenues. State aid has been reduced by over 25% just since 2008. • Garden City receives no Race to the Top funding • It does not appear that Garden City will receive a substantial increase in state aid for the 2012-13 budget year

Challenges for the School District Budget • Little has been done to help the school district address the current expenses that are driving up costs like pensions and unfunded mandates • Even with the tax levy cap, new mandates have been imposed on school districts • Printing scoring and scanning of every student response sheet for grades 3-8 testing (approx. $4.15 per answer sheet) • Printing of 3 versions of the Reference Tables for science Regents and use during the school year (to be bid) and essay booklets for English Regents • Printing of ballots for new electronic voting machines (57¢ per ballot) and renting of new voting machines • Additional student testing required for new teacher evaluation system ($28-30,000) • Staff development and textbook costs associated with new curriculum requirements, new tests and new teacher evaluation system ($10,000+ to date just for workshops for one-third of the required training for administrators on evaluation system) • New asbestos abatement standards

Challenges for the School District Budget • School districts are prohibited from “piggybacking” on many other government contracts • Other levels of government have tried shifting costs to school districts, like the Nassau County sewer tax (approximately $100,000) and cost of preschool special education (in Governor’s current budget proposal) • Tax certiorari refunds will be responsibility of school districts, and these costs—by law—cannot be exempted from the property tax levy cap • The tax levy cap gives “no” votes more weight (1.2) than “yes” votes • No adjustments permitted for enrollment • No adjustments for inflation above 2% • The cap limits the decision-making capacity of elected local officials

Examples of Program Costs • Primary Schools $ 6,900,000 (approx.) • Transportation $ 5,560,000 (approx.) • Special Education $12,300,000 (approx.)

Estimated Expenditure Increases 2012-13 • Pension • TRS (teachers and administrators) $572,000 • ERS (everyone else) $315,000 • Health care $454,000 Total$1,341,000

New York’s Cap vs. Massachusetts’ Cap • New York’s property tax levy cap is said to be modeled on the one adopted in Massachusetts. • However, there are several key differences • Massachusetts set the cap at 2.5%, not 2% • No vote required for budgets under the cap • No 0% cap • The cap in Massachusetts can be overridden by a simple majority vote • Massachusetts accompanied the adoption of the cap by significant increases in state aid

Nassau County Tax Rates There are 56 school districts in Nassau County

Comparison of Per Pupil Costs These are the schools to which Garden City is often compared

The Challenge • Maintain high quality in the face of limited revenues • Keep Garden City as a “destination location”: A community of choice • Ensure that current and future students enjoy the same opportunities provided to former students

What is a focus group? A focus group is a carefully planned discussion to obtain perceptions, opinions, beliefs and attitudes regarding a defined interest area. • A group interview guided by a moderator • A way of listening to people and learning from them • A discussion around a predetermined set of topics

Benefits of a Focus Group • Facilitates collection of information from a group of people in a short time • Provides a tool for eliciting information about people’s attitudes and perceptions • Provides information to assess needs and identify gaps • Guides program development • Communicates valuable information and ideas for assessing programs and services

Structure of the Focus Group • Small group comprised of participants, facilitator and recorder • Participants will be asked to respond to a series of questions • Comments from each of the groups will be compiled • The administration will review comments and discuss their implications with the Board of Education • Comments will be considered when making recommendations to the Board of Education concerning short and long-term planning

Focus Group Assignments and Expectations • Each participant has been assigned to a focus group. The color of the dot on your name tag directs you to the appropriate area. • Members of the administration and faculty will facilitate the discussion • All comments will be treated with the utmost respect— “There are no wrong answers” • Participants should not evaluate the comments of others • Try to be as specific as possible in your comments—Use examples when possible • The discussion must be brought to a close by 9:30 p.m.