Download

1 / 44

440 likes | 537 Views

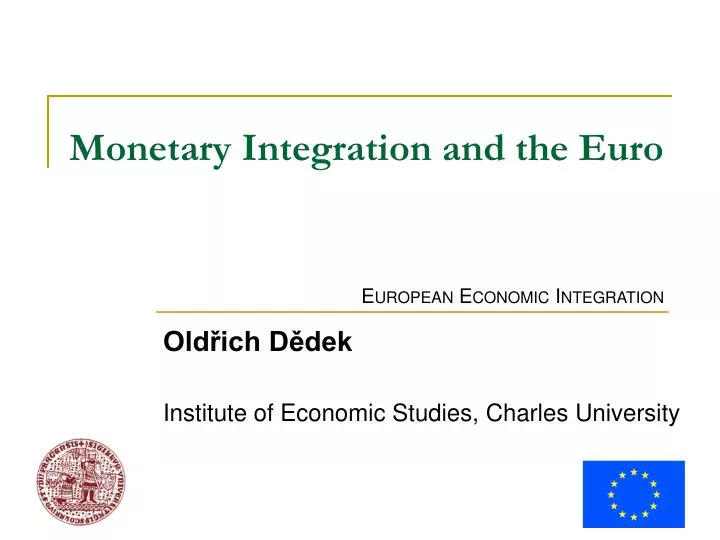

Monetary Integration and the Euro. Oldřich Dědek Institute of Economic Studies, Charles University. Major themes in cost-benefit debate. Absorption of asymmetric shocks Restoration of external price competitiveness Autonomous monetary policy in face of growing capital mobility

E N D

Monetary Integration and the Euro Oldřich Dědek Institute of Economic Studies, Charles University

Major themes in cost-benefit debate • Absorption of asymmetric shocks • Restoration of external price competitiveness • Autonomous monetary policy in face of growing capital mobility • Theory of optimum currency areas

Asymmetric shock – SD diagram P P SG SF • DF, DG … French, German demand curves (rising prices P discourage demanded quantity Q) • SF, SG … French, German supply curves (rising prices P encourage supplied quantity Q) • EF, EG … French, German market equilibrium EF EG DG DF Q Q France Germany

Asymmetric shock – primary adjustment P P SG SF • Autonomous demand shift from French to German goods • France: declining production, rising unemployment pressure for lower wages and lower inflation • Germany: rising production inflationary pressures EG’ DG’ EF EG EF’ DG DF DF’ Q Q France Germany

Asymmetric shock – use of exchange rate P P SG SF • Devaluation of FRF and revaluation of DEM (fixed exchange rate) • Cheaper French exports in Germany and more expensive German exports in France • Rising demand for French goods and declining demand for German goods • Return to initial equilibria prevailing before asymmetric shock EG’ DG’ EF EG EF’ DG DF DF’ Q Q France Germany

Asymmetric shock – absence of exchange rate SF P • Primary effects: drop in demand lower production and higher unemployment pressure on wages cheaper production output expansion (supply curve moves to south-east) • Secondary effects: lower wages lower household expenditure contraction in output (demand curve moves to south-west) • Danger of self-strengthening spiral of deflation and contraction EF DF ED Q France

Asymmetric shock – secondary adjustment SF’ P SF EF’ • Devaluation increases prices of imports (including investment goods), higher production costs supply curve moves to left (new equilibrium EF’ removes part of positive effects of devaluation) • Devaluation is accompanied by monetary tightening in order not to undo price pillow too fast • Pass-through of devaluation is faster the more open the economy is DF’ EF DF Q France

Asymmetric shock – vs. symmetric shock P P SG SF • Symmetric shock hits all members of monetary union • Danger of competitive devaluation (solving French problems at expense of Germany) • Danger of retaliating competitive devaluations, which destabilise mutual trade and push up inflation only • Difficult distinction between symmetric and asymmetric shocks in practice EF EG DG DF DF’ DG’ Q Q France Germany

Asymmetric shock – other practical considerations • Dubious circumstances for using the exchange rate as policy response • Devaluation may weaken pressure for necessary restructuring (sleeping on the exchange rate pillow) • Creation of tensions in other trading sectors (green rates in CAP) • Permanent vs. transitory asymmetric shocks • Outdated model of fixed but adjustable exchange rates • Movements of floating exchange rate need not be linked to the occurrence of asymmetric shocks • Overshooting in exchange rate changes

Competitiveness – purchasing power parity • Phillips curve postulates trade-off between inflation and unemployment (or growth rate) • Different countries may have different preferences about inflation-unemployment mix (lower unemployment at cost of a higher inflation and vice versa) • At different inflation rates, exchange rate helps restore price competitiveness • Static PPP: PI = EI/Gx PG • Dynamic PPP: πI = eI/Gx πG

Competitiveness – equilibrium devaluation πI Italian PC German PC eI/G πG uG uI Existence of national currencies: devaluation of lira against mark restores price competitiveness of Italian exporters Absence of national currencies: national inflations must be equal (eI/G = 0 πI = πG) Resulting inflation-unemployment mix need not be optimal in any country (too high unemployment in Italy and too high inflation in Germany)

Competitiveness – monetarist view • Market agents adjust prices and wages according to expected inflation monetary policy inefficiency in medium run (impossible to suppress unemployment below natural level) • Only unexpected inflation (caused by unexpected devaluation) may have stimulating effects temporary effect due to adaptation of inflation expectations • Phillips curve in medium run is vertical (no inflation-unemployment menus are available)

Competitiveness – vertical PC • Creation of monetary union does not involve long-run costs (natural unemployment rate is not related to inflation) • Higher-inflation country receives one-off bonus from importing low inflation (loss of exchange rate tool should not be seen as cost of monetary union) • Problems can arise during adjustment to new equilibrium (termination of formal or informal indexation schemes) German PC (long-run) Italian PC (long-run) πI πG uGn uIn

Monetary autonomy – Impossible Trinity Impossible Trinity means that no monetary arrangement can reconcile simultaneously Fixed exchange rates Autonomous monetary policy (in setting interest rates) Free capital movements Uncovered interest rate parity Practical examples Intrinsic instability of fixed but adjustable exchange rates (single currency solves the dilemma) Currency mismatches in foreign borrowing 14

Theory of optimum currency areas (OCA) • OCA is theoretical basis of whether countries should form monetary union = one authority responsible for conduct of monetary policy • The author of OCA theory is Robert Mundell (Nobel prize winnerin 1999) • Other contributors: Peter Kenen, Ronald McKinnon, Jacob Frenkel • OCA criteria (ability to adjust smoothly to asymmetric shocks): • Flexible labour markets(avoids painful drop in real wages in reaction to asymmetric shocks) • Structural similarity (makes occurrence of asymmetric shocks less likely) • Trade openness (diminishes efficiency of exchange rate adjustment)

Endogenous OCA • Endogenity principle • Creation and maintenance of monetary union among countries which do not form OCA accelerates integration processes and contributes to achieving OCA faster • Countries may form a monetary union even though they do not form optimum currency area • Elimination of exchange rate risk boosts mutual trade • Exchange rate stability improves efficiency of investment decisions • Costly hedging with financial instruments (lack of long-term contracts) • Absence of exchange rate risk leads to deeper integration • Price transparency enhances competition in product markets (complications due to price regulation, different tax system, consumer preferences) • Easier capital mobility contributes to easier overcoming of asymmetric shocks • Asymmetric shocks are made more symmetric (through more diversified ownership of assets)

Post-war monetary order • Bretton-Woods arrangement as reaction to unprecedented inter-war instability (deep economic recession, protective practices, competitive devaluations) • Pivotal role of US dollar (guarantor of store of value through link to gold, 1 oz = 35 $) • Regime of fixed but adjustable exchange rates (fluctuations ± 1%) • International Monetary Fund as overseer of world monetary order • Extends loans to countries with temporary balance-of-payments problems • Monitors exchange rate realignments

European Payment Union (1950-1958) • System for multilateral settlement of bilateral trade transactions • No direct debtor-creditor relationship among EPU members (only debtor-creditor positions vis-à-vis EPU) • Makes for easier removal of bilateral trade restrictions • EPU wound up after making member currencies convertible

Rome Treaty • No explicit attention paid to potential creation of monetary union or fixed exchange rate arrangement • Laid down some important prerequisites for eventual monetary union (full convertibility of currencies, abolition of capital controls, coordination of economic policies) • No acute problem at time of well functioning of Bretton-Woods system • Rising tensions in the end of 1960s brought forward debate about benefits of stable currency (strong perception of advantages of single currency) • Devaluation of British pound in 1967(UK is not EEC member yet) • Devaluation of French frank in 1967 (instabilityfor CAP) • Growing tensions of US dollar leading to the collapse of B-W system

Werner Report (1971) • Ambitious plan proposing a three-stage move to monetary union starting in 1980 (irrevocably fixed exchange rates, eventual introduction of single currency) • Clash of two approaches • Monetarist school: narrowing exchange rates fluctuations first that would promote deeper economic convergence (France, Belgium, Italy) • Economist school: first economic coordination and convergence of economic performance and only then planning of monetary union (Germany, Netherlands) • Compromise solution: both tracks followed simultaneously • WR agenda shelved under pressure of acute economic problems • Oil shock (1971) made visible different approaches to policy priorities • Collapse of Bretton-Woods system (1973) • Conspicuous divergence in inflations and unemployment rates • European Monetary Cooperation Fund (EMCF) established in 1973 • Extension of short-term credits with the aim to stabilize balance of payments

Snake in the tunnel • Tunnel: European currencies fluctuate vis-à-vis US dollar in a range of ± 2¼ % around dollar central parities mutual fluctuations of up to 9 % ● ● +2¼ DEM/USD dollar parity -2¼ FRF/USD ● ● Snake: European currencies fluctuate in a range of ± 2¼% around mutual bilateral central parities mutual fluctuations of up to 4½% +2¼ FRF/DEM bilateral parity -2¼

Historical moments of monetary snake • 24/4/72: Founding members Belgium, France, Italy, Luxemburg, Netherlands, West Germany • 1/5/72: Denmark, United Kingdom enter • 23/5/72: Norway associates • 23/6/72: United Kingdom exits • 27/6/72: Denmark exits • 10/10/72: Denmark returns • 13/2/73: Italy exits • 19/3/73: Sweden associates • 19/3/73:Collapse of Bretton-Woods system • 3/4/73: Creation of European Monetary Cooperation Fund • 19/1/74: France exits • 10/7/74: France returns • 15/3/76: France exits Source: Gros & Thygesen: European Monetary Integration.

European Monetary System (EMS) • EMS launched in March 1979 • All EC members took part, but not in all components (integration à la carte) • Major components of EMS • European Currency Unit (ECU) • Exchange Rate Mechanism (ERM) – voluntary membership • European Monetary Cooperation Fund (system of credit facilities to defend fixed exchange rates) • Divergence indicators

European Currency Unit – ECU • Basket currency composed of given quantities of all EC currencies (not only those participating in ERM) • Weights derived from economic strength of member countries (share in intra-EC trade, share in GDP) • Regular updates at 5 year intervals • Maastricht Treaty locked the composition of ECU • Non-cash (scriptual) currency (no physical ECU banknotes and coins) • Initial value set at 1 ECU = 1 USD • Functions of ECU (official ECU) • Unit for defining central rates in parity grid • Accounting unit for EC budget • Means of payment in official transactions (EC authorities, member states, international organisations) • Political symbol (harbinger of possible monetary union) • Private ECU • Financial market instruments denominated in ECU that tracked composition of ECU currency basket (deposits and loans, international bonds, foreign exchange contracts)

ERM – parity grid • ERM as pegged but adjustable exchange rate system • Each ERM currency has its central parity vis-à-vis ECU • Bilateral parities organised into matrix called parity grid • Central parity as centre of fluctuation band with width ± 2¼% (Italy ± 6%) • European nature (system functioning without any link to dollar or gold) – joint float vis-à-vis dollar • Formal symmetry (absence of dominantcurrency) versus factual asymmetry (different pressures on debtor and creditor central banks duringinterventions)

ERM – illustration of parity grid B … buying point, S … selling point, P … parity

ERM – operational features • Symmetric support • Central banks of both weak and strong currencies must take part in interventions • Unlimited support • System of credit facilities urges central bank with strong currency to provide sufficient amounts of liquidity to central bank with weak currency • Fixed deadlines for repayment of borrowed funds • Collective realignments • Changes in parities based on agreement of all ERM members (protection against competitive devaluations) • Divergence indicators • Early warning indicators of exchange rate pressures with presumption to act (interest rate changes, budgetary measures, initiation of realignment, etc.) • Set at 75% distance of ± 2¼*×(1-w) % from central parity (w is the weight of a given currency in ECU)

EMS stages – turbulent start (1979-1985) • Unstable international environment (following second oil shock) diverging inflations and policy responses • ERM acted primarily as prevention against unilateral competitive devaluations • Frequent realignments (9 during 1st stage) • Large number of countries involved • Systemic problems • Political tensions when big currencies were to be realigned (political cost of devaluation, opposition of business people against revaluation) • High predictability of realignments waves of speculative activity • Realignments caused by external events (weak dollar capital flows to Germany pressure on mark compulsory interventions)

EMS stages – German mark anchor (1986-1991) • Monetary leadership of Germany • EMS members tended to coordinate interest rate changes with those of Germany (effect of borrowed credibility) • Period of converging inflations and higher financial discipline • No say of other countries in formulating German monetary policy • Illusion of approaching quasi monetary union • In 1987-1992 no realignments took place (except for techical ones) • Apart from Greece all EC currencies became ERM members • All currencies within narrow fluctuation band ± 2¼% • Other currencies pegged to ECU (Sweden, Finland) • Plans to form EMU once again at top of agenda • June 1988: Hanover European Council (EMU project launched) • April 1989: Delors Report (plan to reach monetary union in 3 stages) • December 1990: Intergovernmental conferences about EMU and political union • December 1991: Agreement reached about Maastricht Treaty

Plan to reach EMU in three stages • Stage 1: from July 1990 to December 1993 • Full liberalization of capital movements • Closer coordination of monetary policies • Fostering economic convergence • Stage 2: from January 1994 to December 1998 • Establishment of European Monetary Institute responsible for technical preparations for single currency • Countries are fulfilling Maastricht convergence criteria (opt-out for UK and Denmark) • Granting independence to national central banks • Stage 3: from 1st January 1999 onwards • Irrevocably fixed exchange rates among participating countries • ECB conducts single monetary policy • ERM replaced by the successor regime ERM-II • Stability and Growth Pact takes effect

EMS stages – currency crisis in 1992-1993 • Reunification of Germany sparked inflation pressures, high German rates criticised by other countries • Less than perfect convergence accompanied by suspension of realignments perception of misaligned currencies (Italy, United Kingdom, Spain) • Battered credibility of EMU (failed referendum about MT in Denmark, uncertainty about outcome in France) • Consequences of crisis • British pound and Italian lira forced to withdraw from ERM at high costs • Heavy speculation against currencies of Spain, Portugal, Denmark, Ireland, France • August 1993: ERM fluctuation bands widened from ± 2¼% to ± 15% (wide bands not very different from floating)

EMS stages – heading towards euro (1994-1998) • Crisis in 1992-1993 strengthened arguments of Impossible Trinity • Choice among corner solutions: free floating versus single currency • Promotion of exchange rate stability within wide bands • Lower risk of exchange rate speculation due to higher exchange rate uncertainty within wide bands • Attacked currency moved back into narrow corridors • Italy returned into ERM in 1997, UK and Sweden stayed permanently outside • Austria and Finland entered ERM in 1995 after becoming members of EU • Orderly transition to Stage 3 in spite of turbulences on global financial markets • 1988: crisis in South-East Asia, Russian rouble crisis • Those interested in EMU membership focused on fulfilling nominal convergence criteria remarkable improvement in public finances

Three phases of Stage 3 • Madrid Summit (December 1995) • Beginning of Stage 3: 1 January 1999 at latest • ECU renamed euro • Phase 1 (1999-2001): circulation of euro in non-cash form • National currencies became non-decimal representations of euro • Principle „no compulsion – no prohibition“ • Phase 2 (Jan-June 2002): dual circulation • Introduction of euro in physical form in coins and banknotes • National currencies are withdrawing from circulation • Logistically successfully managed changeover process • Phase 3 • Euro is the only legal tender in Eurozone countries

Actual versus perceived inflation Source: European Commission

Explanation of perceived inflation Consumers attach a higher importance to price developments of goods and services that they buy more frequently (out-of-the-pocket expenditures) Consumers are more influenced by upward price movements than by downward changes Consumers pay high attention to exceptional price increases despite a very low weight of products in consumer basket Prices in national currencies remained reference units for price comparisons with euro prices that were exposed to accumulated yea-to-year inflation Public fails to differentiate between different reasons for higher inflation Accusation for price increases were amplified by media coverage (preference for bad news) 36

Maastricht convergence criteria • Creation of monetary union perceived as “coronation” of convergence process towards price stability • Binding deadlines for start of Eurozone, not later than 1 January 1999 even with smaller group of countries • Limited inspiration by OCA principles when qualification criteria were formulated; stress on operability and intelligibility

Convergence criteria – inflation • Maximum admissible limit: average of three lowest inflations in EU countries plus 1.5 percentage points • Indicator: Twelve month average HICP (Harmonised Index of Consumer Prices) • Motivation • Substantial inflation differentials make single monetary policy difficult to operate • Erosion of price competitiveness without recourse to realignments • “Value of price stability” adhered to by all Eurozone members (guarantee for Germany) • Objections • Why inflation in countries outside Eurozone? • Who are outliers (countries with extremely low inflation)? • Too restrictive for catching-up countries (Balassa-Samuelson effect)?

Convergence criteria – long-term interest rates • Maximum admissible limit: average of interest rates in three EU countries with lowest inflation plus 2 percentage points • Indicator: Average monthly yield on 10-year government bonds • Motivation • Sustainability test of low inflation in longer term • Avoiding large instability in pricing debt securities when they are converted from national currency to euro • Objections • Elimination of exchange rate risk in monetary union makes interest rate differentials unsustainable (consequence of uncovered interest rate parity) • Automatic convergence of bond yields as a result of approaching Eurozone membership • Caveat: elimination of exchange rate risk does not eliminate credit risk

Convergence of long-term interest rates Source: Eurostat. 40

Convergence criteria – exchange rate • Content: Membership for at least two years in ERM II, keeping exchange rate within normal bands without severe tensions and devaluation of central parity • Motivation • Test of appropriateness of central parity before it is irrevocably fixed (ERM II as a training field) • Preventing competitive devaluations prior to fixing (conversion rate should be close to market exchange rate) • Objections • Outdated concept of a normal band (former narrow bands ±2¼ % were abolished during 1992-93 crisis) • ERM II as a compulsory waiting room • Exchange rate stability assessed from the perspective of more criteria • Properties of ERM II • Central rates are defined bilaterally in terms of euro • Fluctuation margins ±15 %, narrower margins can be negotiated with ECB or set unilaterally • Automatic interventions on the margin provided they do not jeopardize price stability in Euro Area • Exchange rate regimes incompatible with ERM II membership: free or managed float, unilateral euroization, exchange rate pegged to other currencies than euro

Convergence criteria – fiscal stance • Government deficit • Deficit-to-GDP ratio shall not exceed the reference value of 3%, unless • The ratio is steadily declining and approaching the reference value • Exceeding the reference value is modest, exceptional and temporary • Government debt • Debt-to GDP ratio shall not exceed the reference value of 60%, unless • The ratio is declining and approaching the reference value in satisfactory way • Exceptions vital for Belgium, Italy and Greece

Links between debt and deficit (size of deficit ≈ change in debt) dt … ratio of deficit to GDP bt… ratio of debt to GDP gt … growth rate of nominal GDP 3% deficit and 60% debt are roughly consistent with 5% nominal GDP growth (approx. 2% inflation and 3% real GDP growth)

Multi-speed Europe • Eurozone members • Founders: Austria, Belgium, Finland, France, Germany, Ireland, Italy, Netherlands, Luxembourg, Portugal, Spain • Enlargements: Greece (2001), Slovenia (2007), Cyprus and Malta (2008), Slovakia (2009), Estonia (2011) • EU members and Eurozone non-members with permanent exception (opt-out) • ERM-II members: Denmark • ERM-II non-members: United Kingdom • EU members and Eurozone non-members with temporary exception (derogation) • ERM-II members: Latvia, Lithuania • ERM-II non-members: Sweden (euro rejected in referendum), Czech Republic, Hungary, Poland, Bulgaria, Rumania • European countries outside EU using euro as national currency • National euro coins: Monaco, San Marino, Vatican City • Others: Andorra, Kosovo, Monte Negro