Download

1 / 42

430 likes | 501 Views

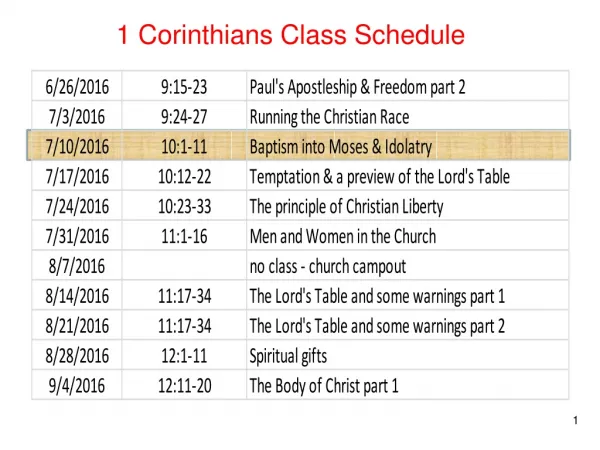

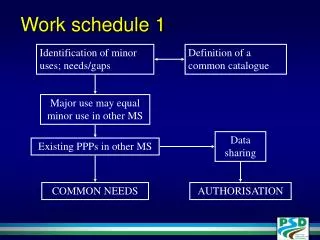

Schedule K-1. Entire Lesson. Pub 4491 – Part 3. Schedule K-1. Reports taxpayer’s share of income, other distributions, deductions, and credits from Estates and Trusts (Form 1041) Domestic Partnerships (Form 1065) S Corporations (Form 1120S)

E N D

Schedule K-1 Entire Lesson Pub 4491 – Part 3 NTTC Training – 2014

Schedule K-1 • Reports taxpayer’s share of income, other distributions, deductions, and credits from • Estates and Trusts (Form 1041) • Domestic Partnerships (Form 1065) • S Corporations (Form 1120S) • K-1s for Foreign Partnerships (Form 8865) are out of scope NTTC Training – 2014

Intake and Interview • Look for K-1s • Verify in scope! NTTC Training – 2014

Schedule K-1 • In-scope K-1s contain ONLY • Interest income (taxable and tax-exempt) • Dividends (ordinary and qualified) • Capital gains or losses (long or short) • Royalty Income • Foreign Tax paid for passive activities • Anything else is Out-of-Scope NTTC Training – 2014

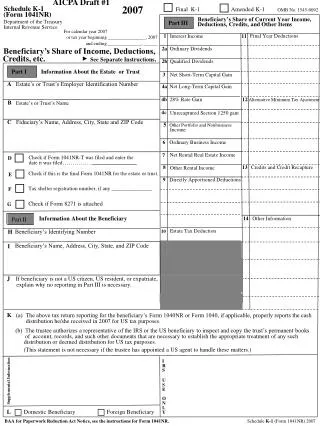

Schedule K-1 (Form 1041) Note: may be Prior year form but be current income for taxpayer when entity is on a fiscal, not calendar, year. 15 NTTC Training – 2015

Schedule K-1 (Form 1065) 15 NTTC Training – 2015

Schedule K-1 (Form 1065) • If end of year capital account is negative, return is out of scope NTTC Training – 2014

Schedule K-1 (Form 1120S) 15 NTTC Training – 2015

K-1 Interest Income • Also look for exempt interest income • Box number varies by form • Look on the back of the form for the code descriptions NTTC Training – 2014

Reporting Income from K-1 Pub 4012, pg D-3 et seq • Do NOTuse TaxWise K1 worksheet • Interest or Dividend Stmt – list payer as [Company] K1 • Net Capital Gain/Loss – Sch D Line 5 for short-term, line 12 for long-term using scratch pad NTTC Training – 2014

Reporting Income from K-1 Pub 4012, pg D-27 • Schedule E for royalties • Foreign Tax paid on Form 1116 NTTC Training – 2014

Foreign Tax on K-1 • Box number varies by form • Must be coded as Passive income • Will be covered in later lesson NTTC Training – 2014

Quality Review • Verify in scope • Verify tax year • Verify entries • On respective worksheets and forms • Not on K-1 in TaxWise NTTC Training – 2014

Exit Interview • Will need to explain if out of scope NTTC Training – 2014

TY 2015 Scope Sch C Schedule C – Profit or Loss from Business (Sole Proprietorship) NTTC – Dallas 2015

Schedule C Key References • Schedule C – Profit or Loss from Business (Sole Proprietorship) Guidelines for Preparing Schedule C…. • Publication 4491 Part 3 Lesson 10 • Form 1040 Line 12 • TY 15 NTTC Training Files #16 NTTC – Dallas 2015

Schedule C Profit From Business (Sole Proprietorship) • Sole proprietorship • Independent Contractor* • *Reference: • Publication 926 Household Employer’s Tax Guide NTTC – Dallas 2015

Schedule C Input • Use Schedule C (do not use Schedule C-EZ) • Must be for either Taxpayer or Spouse • Jointly run business must be split into two Schedules C • Self employment tax implications NTTC Training - TY2015

Schedule C Income • Forms 1099-Misc Box 3 (Other income) or Box 7 (non-employee compensation) • Form 1099-K (Merchant Card and Third Party Payments) • Tax payer records or cash receipts NTTC – Dallas 2015

Business Income – 1099-MISC • Reported to Taxpayer on Form 1099-MISC • Box 7: Non-employee compensation • Box 3: Other income (?) (Ask what income was for - payer may have used wrong box) • Very important to use 1099-MISC that is linked with Sch C NTTC Training - TY2015

Business Income – 1099-MISC Not Sch C Not Sch C OOS OOS OOS OOS OOS OOS OOS OOS OOS OOS OOS OOS OOS NTTC Training - TY2015

Understanding Form 1099-K • Payment from card transactions and/or • In settlement of 3rd party networks • Gross payments > $20,000 and • > 200 such transactions • One form from each payment entity NTTC – Dallas 2015

Form 1099-K NTTC – Dallas 2015

Form 1099-K Gross Receipts • Schedule C Part I Select Scratch pad • Enter individual respective 1009-K Box 1 value(s) or summary of all 1099-Ks on detail line(s) • Enter appropriate descriptive Information for the detail sheet NTTC – Dallas 2015

Form 1099-K Tax Withheld …. • Enter all Box 4 Federal Income Tax values, as appropriate • Enter all Box 8 State Income Tax values, as appropriate NTTC – Dallas 2015

Schedule C Expenses- Basics • Increased from $10,000 to $25,000 • Simplified Home Office Deduction Still out of Scope. NTTC – Dallas 2015

Business Expenses • Ordinary and necessary to the business • Not against public policy • Cannot deduct fines or penalties • All permissible expenses should be claimed • If not claiming an expense results in a tax benefit that would not otherwise occur, then it must be claimed (i.e. if it improves EIC for example) NTTC Training - TY2015

Schedule C Expenses- Additional • Does not file Form 1099-Misc for payments of $600 for services performed by people not considered employees • No prior year un-allowed passive activity losses • Is not required to file Form 4562- Depreciation and Amortization NTTC – Dallas 2015

Business Expense –e.g. Computer • Out of scope • Requires depreciation or write-off using Form 4562 • May claim supplies (paper, toner) used for business NTTC Training - TY2015

What can be Depreciated • 1: Owned by the taxpayer • 2: Used in a trade or business or income producing activity, and • 3: Have a useful life that extends beyond the year placed in service NY3 Instructor WorkshopNovember2015

Leased Property • Depreciable only if the taxpayer retains incidents of ownership • Legal title to the property • Legal obligation to pay for the property • Pay maintenance and operating expenses • Responsibility for taxes • Risk of loss if property is lost/damaged NY3 Instructor Workshop- November 2015

Schedule C Conditions • Uses cash method of accounting for business • Does not have net loss from business • Does not have any employees • Has no cost of goods sold & no inventory at any time during the year NTTC – Dallas 2015

Schedule C Conditions ….. • Claims mileage at standard rate rather than actual maintenance, repair, fuel, insurance costs for vehicle • Has no out of scope expenses NTTC – Dallas 2015

Schedule C Expenses- Special Consideration • Net cost of health insurance on Schedule A on behalf of family/dependents • 1040 Line 29 as adjustment to income for health insurance is OUT OF SCOPE • Expenses for equipment NTTC – Dallas 2015

TY 2015 ABLE Accounts Pending NYS Instructions NTTC – Dallas 2015

Scope – ABLE [Section 529A] Accounts(Achieving a Better Life Experience) • States can offer specially designed, tax-favored ABLE accounts to people with disabilities who became disabled before age 26 • For federal tax purposes • Contributions are after-tax dollars and can be made by any person • Contributions (reported on new Form 5498-QA) must be in cash and are not deductible for federal income tax purposes (states may differ) NY3 Instructor Workshop – November 2015

ABLE Accounts • Total annual contributions cannot exceed the gift tax exclusion in a single year, currently $14,000 for 2015 • Distributions from an ABLE account (reported on new Form 1099-QA) that are used for qualified disability expenses of beneficiary during tax year are excluded from gross income NY3 Instructor Workshop – November 2015

ABLE Accounts • Distributions that exceed qualified disability expenses of beneficiary • Subject to an additional tax of 10% on amount not used for qualified expenses • Included in gross income of beneficiary (Form 1040, Line 21) • Non qualified Distributions are Out of Scope Sep 2015 Regional Meetings

ABLE Accounts • Most states have not completed process to create their state programs • SPEC believes taxpayers who are able to create this type of account will generally not be taxpayers we customarily see • Non qualified distributions are out of scope Sep 2015 Regional Meetings

Form 5498-QA ABLE Account Contribution Information NTTC – Dallas 2015

Form 1099-QA Distributions from ABLE Accounts NTTC – Dallas 2015