Download

1 / 10

E N D

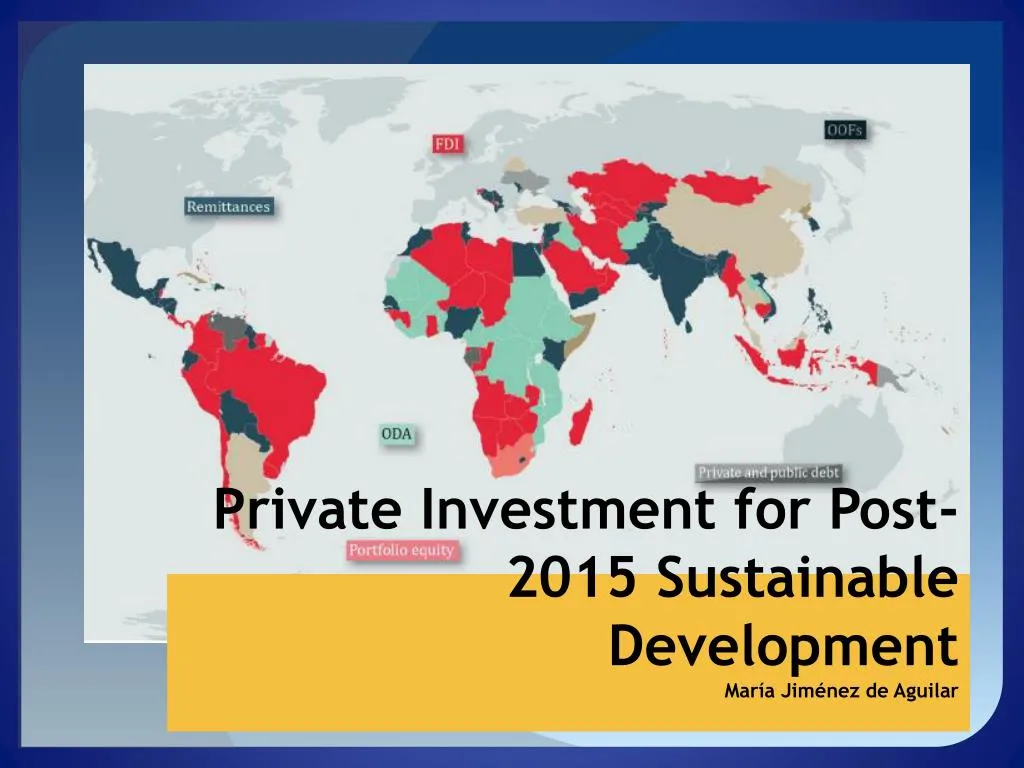

Private Investment for Post-2015 Sustainable DevelopmentMaría Jiménez de Aguilar

Achieving Post-2015 developmentgoalswillrequirethemobilization of resourcesfromprivatesourcesincluding FDI, bankloans, bond issuance, institutionalinvestorsand privatetransfers Source: Financing for Development Post-2015, WBG Paper, Oct 2013. ThemostimportantflowistheForeignDirectInvestment

HOW TO ATRACT PRIVATE INVESTMENT ? • The drivers of privatefinance are distinctlydifferentfromthemotivations of domesticpublicfinance. • Itisnecesarytotalk in terms of risk and return. • At thesame time, businessesrealizethatunmetsocietalneeds, notjusteconomicneeds, define markets HOW MUCH IS THE COST OF PRIVATE INVESTMENT ? • Itisneededcalculatethereturnthatprivateinvestmentexpectedtoearnwhentheyinvest in emergentcountries. • Onemodelwhich combines returns and riskis Capital AssetsPricingModel

Returns and RiskCAPM MODEL The Capital AssetsPricingModel (CAPM) proposedbyWilliam Sharpeisusedtocalculatetherequiredrate of returnforanyriskyasset. The doctrine has introducedsomechangesrelatedtoemergentmarkets, butthismodelisusefultoexplaintherelationbetweenrisk and returns. Yourrequiredrate of returnedistheincrease in valueyoushouldexpecttoseebasedontheinherentrisklevel of theasset. In thismodel, thereturnexpected , E(Ri) , dependson : E(Ri) = Rf + β x ( Rm-Rf) + Rp • Rf – Risk free rate. • Rm –Expectedmarketreturn • β - Risk of asset. • Rp– SovereignRisk.

GOVERNMENTS COULD INCREASE PRIVATE INVESTMENT DECREASING SOVEREIGN RISK The sovereign risk is measured by Ratings Agencies as Moodys and Standars & Poors. They focus their analysis in these critical points which governments have to control:

POLICY MEASURES The governments could act in these critical points with policy measures. For instance, these are some, but not the only ones:

InvestmentCategories • Infraestructure – Comprised energy investments, transport and water. • Agriculture and food systems. There is often a need for complementary investments in transport, rural credit systems, climate risk insurance, and for streamlined mechanisms to coordinate public and private sector activity. • Extractive industries. • Social sector investments, such as in health services and education. • The service sector of the real economy, including the financial sector.

GAPS AND PRIORITIES FOR ENHANCED PRIVATE INVESTMENT Concerning investment categories, these are policy measures to make: Source: MobilizingPrivateInvestmentfor Post-2015 SustainableDevelopment By: Homi Kharas and John McArthur

Credits: • From Billions to Trillions: Transforming Development Finance, WBG, joint with IMF and MDBs, Apr 2015. (Pages 12-17) • Mobilizing Private Investment for Post-2015 Sustainable Development, By Homi Kharas and John McArthur, Brookings Institute, Briefing Note, Jul 2014. • Financing for Development Post-2015, WBG Paper, Oct 2013. • Harnessing All Resources to End Poverty, Development Initiatives Working Paper, Mar 2013.