Download

1 / 7

70 likes | 219 Views

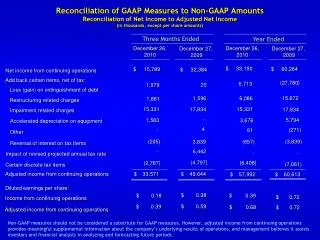

d. Income from Continuing Operations. d. Income from Continuing Operations. The section “income from continuing operations” includes all revenues, expenses, gains, and losses that are not required to be reported in other sections of an income statement.

E N D

d. Income from Continuing Operations • The section “income from continuing operations” includes all revenues, expenses, gains, and losses that are not required to be reported in other sections of an income statement. • There are two formats for the presentation of income from continuing operations: • The single-step format • The multiple-step format

d. Income from Continuing Operations, cont’d • In the single-step format, items are classified into two groups: • Revenues • Expenses

Example of Single-Step Format: • Revenues: • Sales (net of discounts and returns and allowances) $xxx • Gain on sale of equipment xxx • Interest income xxx • Dividend income xxx $xxx • Expenses: • Cost of goods sold $xxx • Selling expenses xxx • General and administrative expenses xxx • Interest expense xxx • Income from continuing operations xxx $xxx • Income from continuing operations = $xxx + $xxx

d. Income from Continuing Operations, cont’d • In a multiple-step format, operating revenues and expenses are separated from nonoperating revenues and expenses to provide more information concerning the firm’s primary activities.

Examples of common intermediate income components: • Gross profit (margin) • Operating income • Income before income taxes (Example of a multiple-step format on next slide.)