Download

1 / 37

370 likes | 541 Views

Exploring the UAA Budget Process (How do we Allocate Resources?). By Kelly Thorngren, Budget Director, 786-4636. Goals for Today- to Understand:. General Budget Concepts Responsibilities of Major Budget Units UAA’s budget request process for allocating r esources

E N D

Exploring the UAA Budget Process(How do we Allocate Resources?) By Kelly Thorngren, Budget Director, 786-4636

Goals for Today- to Understand: • General Budget Concepts • Responsibilities of Major Budget Units • UAA’s budget request process for allocating resources • How the University tracks budget status through management reports • How changes in budget climate have impacted budget available

Goals for Today • FUN! • (Ask Questions • Throughout!)

Enough Fun • Let’s take a Quiz!

Budget Basics • Budget distributes authority to spend for a full year per a departments financial plan. • By projecting budget for a year’s worth of revenue to be earned, you pre-fund and facilitate spending. • Your starting “Base budget” is increased each year by salary rate and benefit increases, plus any new budget increment awards. • “Adjusted Budget” includes one-time transfers made during the year. • Budget projections are never perfect, so budget revisions are done during the year to accommodate changes.

UAA Tuition Sharing Policy • Community Campuses keep 100% of their tuition and pay for their own personnel increases, incremental increases and other fixed costs. • Anchorage Colleges keep 80% of their tuition, the amount of the rate increase is pulled back to help pay for all departments salary and benefit increases. • 20% kept centrally to pay $5M employee and spouse tuition waivers, $3M payments to SW for Computing, Insurance, and $1M for bond debt service

Major Budget Units • Budget is distributed to Major Budget Units (MBU), who have the responsibility and authority to distribute budget among their departments. • One-Time: Can distribute extra salary budget (salary savings) or excess revenue earned to buy equipment, or do an industry needs survey for a new program… • On-going: Can reorganize positions to distribute general fund to high priority needs, like advising positions or distance delivery technology support position or faculty for new degree… • MBU manages budget, cannot be deficit, and reports on budget status through the management report process.

Major Budget Units- Total FY14 Budget Size Varies $33.8M $68.6M $24.3M $10.5M $19.3M $3.0M $7.8M $1.4M $6.1M $6.9M $12.8M $15.8M $16.6M $5.0M $10.9M $7.6M

Management Report Process • Each MBU submits monthly budget status reports beginning in October (no reports Xmas and Spring Break) • Balance to end of Cycle financial reports • Budgeting is all about projections…. to June 30! • Macro and Leave Formula help to automate • Balance at end of year can return to department in the next fiscal year (end of October.) Carry forward now called unreserved fund balance.

MBU- Equal Expense and Revenue Budget • Each MBU receives equal Expense and Revenue Budget. • Equal E/R budget for each Program Code function Examples: IN, RO, PS, AS, SS, GA, OM, FA, UX) (Orgs beginning with 11, 12, 13, 14, 15, 16, 17, 18, 19) • Expense Budget is the Authority to Spend • Revenue Budget is the Responsibility to Earn • if the projected revenue isn’t earned, then expenses may need to be curtailed

Must Earn Revenue to Spend it • Only one type of revenue, General Fund from the State,comes “pre-earned” (YTD revenue is there already, always the same as the budget) • In acct 9210 • When GF Revenue budget moves, the ytd will move with it… eventually. (SW does the JV later) • Let’s see how that works on the Mgmt Report.

Budget Methods • UAA uses a continuation budget aka incremental budget method (just as the State of Alaska does.) • Basically means that at the start of a new budget year MBUs continue with the Base Budget they got last year, plus fixed cost increases for personnel (salary rate and staff benefit increases) • In March the Major Budget Units will start to work on their Position Control Number (PCN) List which will be used to distribute Personnel budget and calculate rate increases on the different personnel categories.

Continuation Budget Method • The State gives us our Base Budget General Fund from last year plus 50% of the personnel increases (not for temps or students.) It was 60%. • The State also give us the authority to earn the non-GF revenue. If we earn too much, we have to ask for more “receipt authority” • Then we submit increment requests for specific proposals • Don’t have to justify the entire budget each year (as with zero based budgeting method), just the requests for incremental increases.

Who Makes the Allocation Decisions at UAA for additional (increment) Budget? • Where does the process start? • How many times must a budget request compete with other requests and be seen as a high priority? • If you wanted a group of people to make budget priority decisions, who would you want to represent you? • What can improve the chances for a request to be approved? Excellent story telling data.

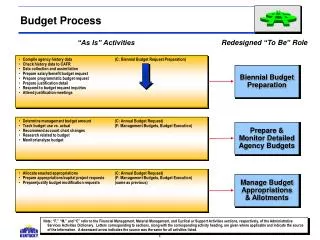

Department Writes Request Dean or Director Prioritizes Dept Requests Chancellor & his Cabinet Make Final Decisions Dean or Director submit requests to PBAC PBAC deliberates and recommends to Chancellor

P Department Writes Request P P Dean or Director Prioritizes Dept Requests Chancellor & his Cabinet Make Final Decisions Dean or Director submit requests to PBAC P PBAC deliberates and recommends to Chancellor

PBAC-Planning and Budget Advisory Council • Co-chairs: Provost Bear Baker and VC Admin Services Bill Spindle • Members from: • 3 Deans, 1 Dean of Students, 1 Institute Director, 2 faculty at large, 1 Community Campus Director, 1 staff-at-large, 5 PBAC council staff, 1 staff from University Advancement and 5 Reps from Faculty/Staff/Student Governance. • Academic Affairs, Admin Services, Alaska Native Studies, College of Business & Public Policy, College of Education, College of Arts and Sciences, College of Health, Community & Technical College, Prince William Sound Community College, Student Affairs, ANSEP, Alumni Relations, Faculty Senate, Union of Students, APT Council, Classified Council, Budget, Financial Systems, Facilities, Provost Office, and Institutional Research.

UAA PBAC Process Timeline • February: Budget Guideline Document issued • March: MBUs start work on PCN list • April: MBUs turn in Increment Budget Requests and present to PBAC April 17/18 • May: MBUs work on Base Budget details • May: PBAC finalizes UAA distribution decisions, submits to Chancellor • June: When State/UA approve, Budgets finalized

Annual PBAC Instructions-Handy! • Provide guidance on upcoming budget climate • Provide guidance on UAA focused strategic goals • Provide Forms needed

How many requests can UAA consider funding? • How much new money is available for allocation depends on many factors… • We depend on two types of revenue to fund our largest fixed cost increase first, then $ can be available for increment awards • In addition, money can be re-allocated from one department to another • UAA has distributed across-the-board cuts to General Fund in 7 of the last 9 years (1 to 2% each year) $8.3M • In two of those years only Administrative depts were cut • Every 1% cut equals approx. $1M which can be used to balance the budget • Requests not funded at UAA level, can be forwarded to BOR/State Legislature for funding. • In FY14, we received $1.3M of our $4M original request

Annual Decreases to General Fund Distributed to Major Budget Units

Two Reasons Budgets are Tighter Now When the State reduced it’s support of the University’s salary increases, tuition rates went slightly higher for two years, then dropped. For two years the impact of the decrease in the State support was buffered. But in FY14 we began to live with a new reality.

Simple? • So, University budgets are pretty simple: Basically the tuition rate increases are used to pay for 50% of the personnel increases (the State pays for the other 50%) • So, the setting of the tuition rate increase is important if not vital to the budget plan • As is enrollment! student retention and recruitment

Why not use other sources of revenue to cover personnel increases you ask? FY14 Unrestricted, Restricted and Auxiliary Base Budget, total $317M

University Budget Balancing- If it wasSimple • FY14: Cover $3.8M Salary Increase Expense with Tuition and GF Revenue $3.1M • Personnel Salary Rate and Benefits $3.8M • Tuition @ 2% $881 • General Fund $2,200.0 • Net Deficit would be $700.0 • But, it’s more complicated…. Of course.

FY14 Budget Update • Total Expense $8.1M • Personnel Expense $3.8M • Dept Budget Distributions: $2.7M • Cover remaining $1M deficit from FY12 • Cover fixed cost increase for $10M Deferred Maintenance Bond payments $620.0 • Total Revenue $5.1M • Tuition 880.7 • General Fund $2.2M • Internal Reallocation (20% tuition) $2M • Net Deficit $3M • Carry forward $2M deficit • Distribute 1% across-the-board cut to General Fund for all major budget units

Why carry forward $2M Deficit? • Would need to cut dept GF 3% rather than 1% • Across the Board cuts not the best • Depts like HR continue to be cut whether they are understaffed or not… • All admin departments do not earn tuition and therefore have less excess funding to cover cuts • Hold for more hopeful budget environment • Tuition Rate Increase was an unknown for FY15 when budget was finalized… it could have been 7% or 10% ( is now known to be avg 3.2%)

FY15 Budget Requests to the Legislature Must be Prioritized and Approved by: • UAA PBAC Recommendation to Chancellor • UAA Chancellor and Chancellor’s Cabinet • UA President Gamble, his Cabinet and SW Budget • Board of Regents • Governor • Legislature • House and Senate Budget Committees • House and Senate • Conference Committee • Governor’s Veto

FY15 Budget Planning • By now we know that there are 3 major factors when planning for FY15…. • What is the tuition rate increase? • What are the salary rate increases for each employee group? • Need to cover that $2M from FY14 eventually…

FY15 Personnel Increases being Proposed • Staff (XR and NR) 2% increase with an additional personal day off • UAFT faculty extended current contract to December 31, 2014 (so rate increase may be the same 2.5% as in FY14… but not officially announced yet) • UNAC and Adjunct union expire Dec. 31, 2013- being negotiated

We should remain positive, while understanding that the more information we have about programs and functions, the better we can prove we are worthy of funding increases • UAA has a $10M to $12M carry forward that can be used to supplement budget • Annual Cost Savings and Efficiencies report shows the BOR and the State we are good stewards • Enrollments could increase in response to the many retention and recruitment measures • We are still getting salary rate increases • UA could return to slightly higher tuition rate increases

Review Quiz and • Any Final Questions?