Download

1 / 10

100 likes | 304 Views

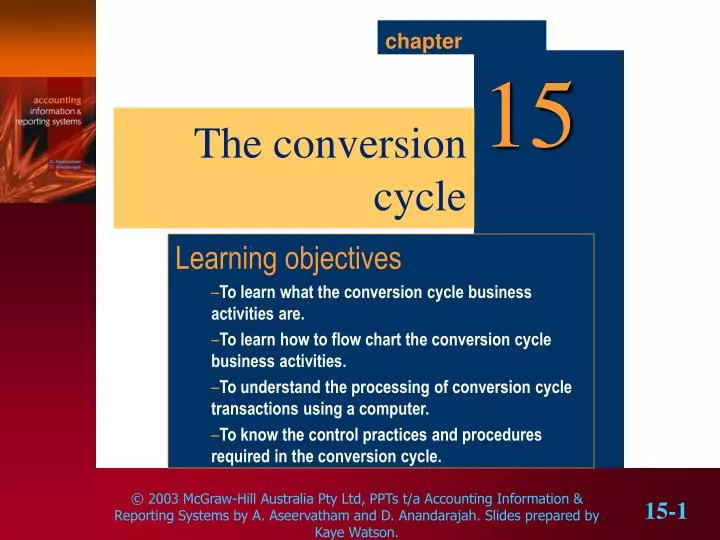

The conversion cycle. Learning objectives To learn what the conversion cycle business activities are. To learn how to flow chart the conversion cycle business activities. To understand the processing of conversion cycle transactions using a computer.

E N D

The conversion cycle Learning objectives To learn what the conversion cycle business activities are. To learn how to flow chart the conversion cycle business activities. To understand the processing of conversion cycle transactions using a computer. To know the control practices and procedures required in the conversion cycle.

key terms • direct labour cost • direct material cost • job order costing • just-in-time inventory system • material requirements planning • overhead cost • process costing • work in process

Conversion cycle business activities Transactions in the conversion process: • acquisition of materials • acquisition of labour • transfer of materials, labour and overheads into production • transfer of finished goods to inventory • sale of inventory

Major groups in the conversion cycle • Inventory • Payroll • Cost accounting

Inventory • Main activity is to keep records of inventory levels: • raw materials • finished goods • Valuation methods used: • periodic inventory method • perpetual inventory method

Payroll system • Records labour transactions • Payroll system interfaces with conversion cycle providing information on labour transactions

Cost accounting Records transactions of conversion cycle classifying three major elements: • Direct material costs • Direct labour costs • Overhead costs These are recorded in a ‘Work in process account’

Non-accounting systems Systems necessary to the conversion cycle: • Product design • Production planning and scheduling systems • Material requirements planning • Just-in-time systems • Computer-aided manufacturing

Internal control procedures for the conversion cycle • Material requisitions properly authorised • Approved production schedules • Finished goods transferred to storeperson’s care • Inventory records checked for accuracy • Physically verify stocks to check for losses and accuracy of records • Investigate differences in physical and accounting records and take appropriate action • Monitor defective production • Investigate customer complaints