Download

1 / 72

720 likes | 726 Views

Learn about the New Mexico Mortgage Finance Authority's Tax Credit Program, including housing priorities, program background, eligibility requirements, and partnership structures. Gain insights on how to submit a successful application.

E N D

MFA 2017 Qualified Allocation Plan and Application Workshop December 8, 2016 New Mexico Mortgage Finance Authority

Presentation Overview Page • Tax Credit Program Overview 3 • 2017 Qualified Allocation Plan Review 18 • Application Process 53 • What Makes a Successful Application 66 New Mexico Mortgage Finance Authority

TAX CREDIT PROGRAM OVERVIEW New Mexico Mortgage Finance Authority

Housing Priorities • Increase the supply of decent, affordable rental housing; • Expand housing opportunities and access for individuals with special needs; • Expand the supply of housing and services to assist the homeless; and • Preserve the State’s existing affordable housing stock. New Mexico Mortgage Finance Authority

Background • LIHTC Program created by Tax Reform Act of 1986 as an incentive for individuals/ corporations to invest in the construction or rehabilitation of low income housing. • The Tax Credit provides a dollar-for-dollar reduction in personal or corporate federal income tax liability for a 10 year period. New Mexico Mortgage Finance Authority

Internal Revenue Code §42 • IRC §42 sets forth the requirements and process for the Tax Credit program. • §42(m) states the housing credit agency must make Tax Credit allocations pursuant to a Qualified Allocation Plan, which: • Sets forth project selection criteria; • Gives preference to those serving lowest income tenants for the longest period of time; • Provides a procedure for monitoring compliance. New Mexico Mortgage Finance Authority

Background, Continued • Credit Ceiling: $2.35 per capita allocation + any returned or unused credits + any National Pool credits – forward allocations • MFA allocated $4.738mm in 2016 • MFA will allocate approx. $5mm in 2017 • Tax Credits are the deepest Federal Subsidy that funds up to 70% of total development cost New Mexico Mortgage Finance Authority

Affordable Use • Minimum set aside: • 20% of units for tenants earning no more than 50% of median income (20/50 election) - Requires that all restricted units be at 50% AMI or below to be eligible for credits OR • 40% of units for tenants earning no more than 60% of median income (40/60 election) • This election is irrevocable. • Use restriction for 30 years required (income and rent limits) New Mexico Mortgage Finance Authority

Applicable Fraction • The percentage of the Project that is dedicated to Low Income use • Employee units excluded from calculation Applicable Fraction: 80.56% New Mexico Mortgage Finance Authority

Eligible Basis • The sum of the eligible cost elements that are subject to depreciation. • 70% Eligible Basis (9% Tax Credits) for new construction or rehabilitation costs. • 30% Eligible Basis (4% Tax Credits) for acquisition costs and projects with federal subsidy. • Exclusions- federal grants, land acquisition cost, commercial, etc. • “Basis Boost” – Increases Eligible Basis up to 30% if project is in a HUD Defined QCT, DDA or SADDA. New Mexico Mortgage Finance Authority

Basis Boost • Basis Boost – Up to 30% increase to Eligible • Basis for new construction and rehabilitation costs • only (acquisition costs not eligible). • For Projects in HUD designated QCT, DDA or SADDA (30%). • MFA designation of need for Financial Feasibility (up to 30%) and: • 1. Not Financed with Tax Exempt Bonds; and • 2. Serve a target population. New Mexico Mortgage Finance Authority

Applicable Percentage • The amount of the low-income housing credit for any taxable year in the credit period shall be an amount equal to: (1) the applicable percentage of (2) the qualified basis of each qualified low-income building. IRC §42(a). • Determination of Applicable Percentage: Percentages which will yield over a ten-year period amounts of credit which have a present value equal to: • 1. 70% of the Qualified basis of non-federally subsidized new construction and rehab costs (9% fixed); and • 30% of the Qualified basis of acquisition costs and/or projects that are federally subsidized. • Applicant may elect to lock Applicable (Tax Credit) Percentage at either Carryover or at PIS. New Mexico Mortgage Finance Authority

Tax Credit Calculation Eligible Basis $2,250,000 x Basis Boost (if applicable) 130% $2,925,000 x Applicable Fraction 80.56% = Qualified Basis $2,356,380 Qualified Basis $2,356,380 x Applicable (Tax Credit) % __9% = Annual Tax Credit $ $212,074 New Mexico Mortgage Finance Authority

Equity Calculation Annual Tax Credit $ 212,074 x Years of Credit x 10 = Total Credit Amount $2,120,742 x Price per Credit Dollar x $ 0.96 = Equity to Project $2,035,912 New Mexico Mortgage Finance Authority

Partnership Structure XYZ PROJECT GENERAL PARTNERSHIP General Partner .01% Limited Partner Investor 99.99% New Mexico Mortgage Finance Authority

Partnership Structure • General partner has 0.01% ownership, provides guarantees and operates the project • General partner retains 0.01% of the tax credits, income and losses • Limited partner has 99.99% ownership • Limited partner receives 99.99% of the tax credits, income and losses • Investor equity reduces the need for other financing which reduces debt service, and enables rents to be affordable New Mexico Mortgage Finance Authority

Apply for credits Receive a tax credit reservation Receive carryover allocation, indicate lock-in election Incur 10% of estimated project basis and start construction by August 31 of the following year Complete project and place in service within two years of carryover Apply for 8609’s Record land use restriction agreement Project Lease-up: Qualify Tenants Begin claiming credits: PIS year or following year Keep tax credit units in compliance ** See 2016-2017 LIHTC Calendar on website Tax Credit Timeline New Mexico Mortgage Finance Authority

2017 Qualified Allocation Plan Review New Mexico Mortgage Finance Authority

Qualified Allocation Plan What is it? • The QAP is the State of NM’s plan for allocating its tax credits • It is prepared annually, consistent with IRC §42(m). Approval Process – Pending Approval by Governor Where is it? http://www.housingnm.org/low-income-housing-tax-credits-lihtc-allocations New Mexico Mortgage Finance Authority

Threshold Review All Applications must meet each of the following and include all required materials: • Site Control • Zoning • Minimum Project Score • Applicant Eligibility • Financial Feasibility • Fees New Mexico Mortgage Finance Authority

Site Control • Fully executed purchase contract or option • Written governmental commitment to transfer property by deed or lease • Recorded deed or long term lease. New Mexico Mortgage Finance Authority

Site Control, Continued • Transfer Commitment must: • Provide an initial term lasting until at least July 31, 2017; • Be binding on seller through initial term; and • Have names, legal description, and acquisition cost that match application. • **Initial term must not be conditioned upon any extensions requiring seller consent, additional payments or financing approval. New Mexico Mortgage Finance Authority

Zoning • Evidence that multifamily housing is not prohibited by the existing zoning and dated < 6 months before application deadline. • No pending litigation or unexpired appeal process relating to zoning for project. • Only exemption, a site that is not zoned or which is zoned agricultural. New Mexico Mortgage Finance Authority

Fees • All fees owed to MFA for all Tax Credit Projects in which Principal(s) participate must be current. • 2017 Fees remain unchanged: Application Fee $500 or $1,000 Deposit of $8,500 Processing Fee** of 7.5% (9% Award) or 3.5% (4% Award) **Applicable if a reservation is received New Mexico Mortgage Finance Authority

Applicant Eligibility All members of the development team of the proposed Project must be in good standing with MFA and all other state and federal affordable housing agencies. New Mexico Mortgage Finance Authority

Financial Feasibility • Applications must demonstrate, in MFA’s reasonable judgment, the Project’s financial feasibility. • QAP Section IV.C.2, Section IV.D, and Section IV.E. summarize MFA’s financial feasibility considerations. • Additional Underwriting Details in the Initial Application Underwriting Supplement. New Mexico Mortgage Finance Authority

Per Unit Costs Limits • Based on average per unit costs of new construction and adaptive re-use projects submitted in the round. • Purchase price attributed to land, costs related to commercial space, and reserves will be excluded. • In 2016 the average was $186,332 and in 2015 it was $191,211. • Per project maximum Tax Credit award is $1,150,000 and any entity (including affiliates) may not receive more than 2 awards. New Mexico Mortgage Finance Authority

Minimum Project Score • Two Scoring Tracks: 115 points for Rehab,100 points for New Construction; 80 points for bond projects; • Partial points will not be awarded; • Applicant self-scores application; MFA scores application; • Scoring criteria and information needed to obtain points in QAP and checklist; • Deficiency Correction used only to correct incomplete application or meet threshold – not scoring or Allocation Set Aside requirements. New Mexico Mortgage Finance Authority

Scoring Criteria Criterion 1: Nonprofit, New Mexico Housing Authority , or Tribally Designated Housing Entity (0-10 points) • Requirements in application and checklist must be provided for points • Requirement for points different than requirements for set-aside • Net worth/net assets must be substantiated by reviewed or audited financial statements • Document fee split agreement among parties • Entity required to attend training within 6 months prior to application • Indicate on checklist if submitting as a qualified nonprofit, NMHA, or TDHE New Mexico Mortgage Finance Authority

Scoring Criteria Continued [2016] Criterion 2: Projects that Benefit the Environment (0-18 points) Deleted, but see 2017 Design Standards for HERS and other requirements Criterion 2: Locational Efficiency (0-4 points) Projects located in proximity and connected to: 1) services 2) public transportation New Mexico Mortgage Finance Authority

Scoring Criteria Continued Criterion 3: Rehabilitation Projects (up to 15 points) • Twenty (20) year requirement; limited exception • Scaled scoring- 10 points + up to 5 additional points • Scope of work required at Application New Mexico Mortgage Finance Authority

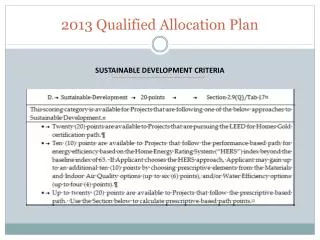

Scoring Criteria Continued Criterion 4: Sustaining Affordability (0-15 points) • Use restrictions are to expire on or before December 31, 2021, or • Federal Rental Assistance Contract covering at least 75% of all Units • 5 points for Projects that have/will have a federal rental assistance contract covering at least 20 percent of all Units [Minimum # of units deleted] New Mexico Mortgage Finance Authority

Scoring Criteria Continued Criterion 5: Average Gross Median Income (AGMI) (0-40 points) • Calculate a weighted average based on the number of units set aside at each income level • Market rate units treated as if they were set aside at 100% • Round to nearest whole number • Three tiers • Points differ for counties with AMI less than or equal to $53,300 New Mexico Mortgage Finance Authority

AGMI Calculation % of Total Set Aside Income Weighted Av Weighted Av Units Level (before rounding) (Final) 7% X 30% = 2.1% 21% X 50% = 10.5% 55% X 60% = 33% 17% X 100% = 17% Total AGMI: AGMI for Scoring 62.6% 63% New Mexico Mortgage Finance Authority

Scoring Criteria Continued Criterion 6: Average Gross Median Rent (AGMR) (0-30 points) • Weighted Average based on the number of units set aside at each rent level • A project can restrict rents at a lower level than the targeted income level for any given units • Market rate units treated as if they were set aside at 100% • Round to nearest whole number • Three tiers New Mexico Mortgage Finance Authority

AGMR Calculation % of Total Set Aside Income Weighted Av Weighted Av Units Level (before rounding) (Final) 7% X30% =2.1% 62% X 50% = 31% 14% X 60% = 8.4% 17% X 100% = 17% Total AGMR: AGMR for Scoring 58.5% 59% New Mexico Mortgage Finance Authority

Scoring Criteria Continued Criterion 7: Market rate units (10 points) • Minimum 15% of the total Units. • Maximum points for AGMI, AGMR and market rate units combined is 65. Criterion 8: Extended Use Period (0-5 points) • Maximum points for 35 year Extended Use Period. New Mexico Mortgage Finance Authority

Scoring Criteria Continued Criterion 9 Special Needs (0-15 points) • 20% of the total units reserved and 50% of reserved units rent restricted at 30% AMI or 30% of tenant income for 15 points. • 5% of units reserved and rent restricted at 30% AMI for 5 points (only available for Projects Financed with Tax Exempt Bonds). • Signed commitment to set aside units and execute agreement with Local Lead Agency or marketing & service plan. • Section 811 Project Rental Assistance may be available. See MFA website for more info. New Mexico Mortgage Finance Authority

Scoring Criteria Continued Criteria 10 & 11: Senior Housing, Individuals with Children (0-15 points) • 100% of total units reserved for Senior Housing. • 25% of the total units reserved for Individuals with Children. • Points range from 7 to 15 based on services provided; list modified for 2017. • Design requirements – mandatory for points. • On-site service coordinator – required for service points. • The proposed Project annual operating budget must include at least $2,500 for the provision of social services. New Mexico Mortgage Finance Authority

Scoring Criteria Continued • Individuals with Children – Unit Mix Calculations Total Units 68 Units with 3/3+ bdrms and 1.75 bathrooms 10 Units with 2 bdrms and 1.75 bathrooms 50 3 bedroom percentage of total Units 14.7% 2 bedroom percentage of total Units 73.5% *See Scoring Criterion for unit requirements New Mexico Mortgage Finance Authority

Scoring Criteria Continued Criterion 12: Contribution from state, local or tribal government entity (0-10 points) • Cash flow loans eligible contributions but cannot have hard payments. • The value of the contribution must be listed as a source on Schedule A-1 and, when not a cash contribution, the corresponding cost must be listed as a cost on Schedule A. • Expanded to include federal funds, 3rd party contributions and permit fee waivers. • Does not include off-site improvements and tax abatements. New Mexico Mortgage Finance Authority

Scoring Criteria Continued Criterion 13: Complete Application (5 points) Applications that do not require any deficiency corrections. See Section IV.A.4 in the QAP: • One omnibus signature page- blue ink signed by all General Partners • Don’t forget the CD, DVD or flash drive and doc’s scanned in color • Brown Classification Folder • All Attachments, Current MFA forms • Do not rely solely on Application Checklist New Mexico Mortgage Finance Authority

Scoring Criteria Continued Criterion 14: Commitment to market units to public housing authority waiting lists (2 points) Criterion 15: QCT/Concerted Community Revitalization Plan (0-5 points) • Projects that contribute to a Concerted Community Revitalization Plan or are located within ½ mile of a New Mexico designated Main Street are eligible for 3 points. • If the Project meets one of the above criteria and is located in a QCT, it is eligible for 5 points. New Mexico Mortgage Finance Authority

Scoring Criteria Continued Criterion 16: Projects with Units Intended for Eventual Tenant Ownership (5 points) • Cannot be combined with Extended Use Period Points [2016] Criterion 18: Financial Literacy Programs (2 points)- Deleted – moved to services Criterion 17: Historic Significance (5 points) Criterion 18: Blighted Buildings or Reuse of Brownfield Site (5 points) New Mexico Mortgage Finance Authority

Scoring Criteria Continued Criterion 19: Projects Located in Areas of Statistically Demonstrated Need (0-10 points) • Tier 1 Areas (10 points) • Bernalillo, Chaves*, Cibola*, Curry*, Eddy, Lea*, McKinley, Otero, Sandoval, Santa Fe and Taos*. All Projects on Native American Trust Lands or Native American-owned lands within the tribe’s jurisdictional boundaries. • Tier 2 Areas (5 points) • Colfax, Dona Ana, Grant, Lincoln, Los Alamos, Luna, Rio Arriba*, Roosevelt, San Juan*, San Miguel, Socorro, Torrance and Valencia. New Mexico Mortgage Finance Authority

Scoring Criteria Continued Criterion 20: Efficient Use of Credits (0-20 points) • Points increased to 10, 15 or 20. • Scoring criterion now includes Projects that involve Substantial Rehabilitation or Moderate Rehabilitation. • Scoring criterion now includes Adaptive Reuse which is scored as if it were new construction. • Scoring thresholds and related points vary depending on type of project (see next slide). New Mexico Mortgage Finance Authority

Scoring Criteria Continued New Mexico Mortgage Finance Authority

Scoring Criteria Continued Criterion 21: Non-Smoking Properties (4 points) • Projects which will be non-smoking properties and participate in the American Lung Association in New Mexico Smoke Free @ Home program are eligible for 4 points. Criterion 22: Adaptive Reuse Projects (5 points) • In combined new construction and Adaptive Reuse Projects, converted space must account for at least 20 percent of the sum of each Building’s Gross Square Feet. New Mexico Mortgage Finance Authority

Additional 2017 QAP Changes • Equalization of project types: two scoring tracks/categories: New Construction (includes adaptive reuse) or Rehabilitation. • 2017 Mandatory Design Standards- updated- see website. • Submission Date: Feb 1 to Feb 15, 2017. • Builder Profit reduced where identity of interest exists. • Allocation set-asides- USDA rehab deleted. • Project narrative expanded to up to 3 pages. New Mexico Mortgage Finance Authority

Other Areas Covered in QAP • Quiet Period- Section IV.A.5. • Affirmative Actions after Reservation- Section IV.G. • Termination of Reservations- Section IV.H. • Changes to the Project- Section IV.I. • Tax Credit Monitoring & Compliance- Section X. New Mexico Mortgage Finance Authority