Download

1 / 12

130 likes | 347 Views

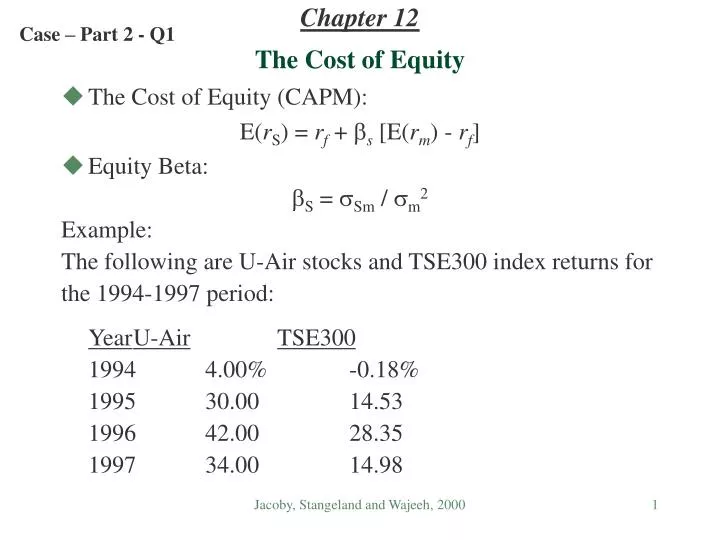

Chapter 12. Case – Part 2 - Q1. The Cost of Equity. The Cost of Equity (CAPM): E( r S ) = r f + b s [E( r m ) - r f ] Equity Beta: b S = s Sm / s m 2 Example: The following are U-Air stocks and TSE300 index returns for the 1994-1997 period: Year U-Air TSE300

E N D

Chapter 12 Case – Part 2 - Q1 The Cost of Equity • The Cost of Equity (CAPM): E(rS) = rf + bs [E(rm) - rf] • Equity Beta: bS = sSm / sm2 Example: The following are U-Air stocks and TSE300 index returns for the 1994-1997 period: YearU-AirTSE300 1994 4.00% -0.18% 1995 30.00 14.53 1996 42.00 28.35 1997 34.00 14.98 Jacoby, Stangeland and Wajeeh, 2000

Calculating the Equity Beta • Calculating average returns: • Calculating the covariance: • Calculating the market variance: • Calculating beta:

Case – Part 2 – Q2 Calculating the Cost of Equity • U-Air’s Cost of Equity (CAPM): Given a 5.09% average T-bill rate, the average historical market risk-premium for the 1994-1997 period is By the CAPM, if the current T-bill rate is 4%, then the cost of U-Air’s equity is given by: E(rs) = rf + bs [E(rm) - rf] = =

An alternative Method for Calculating the Cost of Equity • For U-Air it is given that: YearDividend 0 $0.39 (1+g)4 D-4 = D0 -1 $0.37 (1+g)4 0.33 = 0.39 -2 $0.36 => g = -3 $0.34 -4 $0.33 Also: D1 = Do(1+g) = 0.39%1.0427 = 0.41 Since P0 = $3.65, by the dividend growth model: rs = (D1/P0) + g = • For the remainder of the case, we will assume that the Cost of Equity is that obtained by the CAPM, i.e. 16.6% Jacoby, Stangeland and Wajeeh, 2000

Case – Part 2 – Q2 The Investment Decision • Suppose that U-Air is an all equity firm. Recall that the new Bahamas project generates the following CFs ($Ks): YearCF 0 (41,600) 1 4,740 IRR = 10.95% 2 11,180 3 15,185 4 25,954.375 Assume: • U-Air is an all equity firm • The Bahamas project beta is the same as U-Air’s beta (1.35) Decision: • NPV = -$5,690.98 < 0 => reject the project. Or: • Since by the CAPM (SML) the required return for beta of 1.35 is 16.6%, and IRR=10.95%<16.6% => reject the Bahamas project

The SML and the Investment Decision Expected Return (%) SML * U-Air 16.6 * Bahamas Project IRR = 10.95 4 Beta 1.35 Jacoby, Stangeland and Wajeeh, 2000

Determinants of Beta • Factors affecting Equity Beta: • Business Risk • Cyclicity of Revenues • Operating Leverage • Financial Risk • Financial Leverage Jacoby, Stangeland and Wajeeh, 2000

Financial Leverage • When the firm is not “All Equity” • Recall: the beta of a portfolio (p) with N assets is given by: • The Firm’s Assets are financed by Equity and Debt • Firm’s Assets = Portfolio with Equity and Debt: bASSETS = bEQUITY [S/(S+B)] + bDEBT [B/(S+B)] Assets Equity (S) Debt (B) Jacoby, Stangeland and Wajeeh, 2000

The Cost of Capital of a Levered Firm • Recall: the return of a portfolio (p) with N assets is given by: • The Weighted Average Cost of Capital(WACC): WACC = rASSETS = rS[S/(S+B)] + rB (1 – Tc) [B/(S+B)] after-tax cost of debt Jacoby, Stangeland and Wajeeh, 2000

Case – Part 2 – Q3 • Assuming that a project has the same beta and financial leverage as the whole firm: • calculate the NPV of the project based on the firm’s WACC • compare the IRR of the project to its WACC It is given that: Equity/Assets = 0.53, and Debt/Assets = 0.47 • Recall: by the CAPM: rS= 16.6% • U-Air’s Long-Term bonds are traded with YTM = 6.04% • Recall that Tc = 0.4 • Then, U-Air’s Weighted Average Cost of Capital(WACC) is: WACC = rS[S/(S+B)] + rB (1 – Tc) [B/(S+B)] =

Case – Part 2 – Q4 WACC of the Bahamas Project • If the Bahamas project has the same beta and financial leverage, then • Also: IRR=10.95%>10.5% => accept the Bahamas project Jacoby, Stangeland and Wajeeh, 2000

Case – Part 2 – Q5 & Q6 When the Firm’s beta Differs from the Project’s Beta • The project and the firm may have different betas • when the project and the firm are not from the same line of business - use industry beta (not always available, e.g. Amazon.com) • when the project’s risk is inherently different (even if same industry) • Suppose that the beta of the Bahamas line is 1.8 (higher than U-Air). By the CAPM: rBAHAMAS= rf + bs [E(rm) - rf] = • Then, the WACC of the Bahamas project is: WACCBAHAMAS= rBAHAMAS[S/(S+B)] + rB (1 – Tc) [B/(S+B)] = • Or: IRR=10.95%<12.72% => reject the Bahamas project