Download

1 / 16

160 likes | 307 Views

Real Estate Investment Trusts REITs. Cody Draper Valiant Evans Ryan Weight. Congressional Act.

E N D

Real Estate Investment TrustsREITs Cody Draper Valiant Evans Ryan Weight

Congressional Act Congress created REITs in 1960 to enable small investors to make investments in large-scale, income-producing real estate. Congress decided that the only way for the average investor to access investments in significant commercial properties was through pooling arrangements. As a result, Congress designed REITs to unite the capital of many into a single economic enterprise. That enterprise is geared to the production of income through commercial real estate ownership and finance.

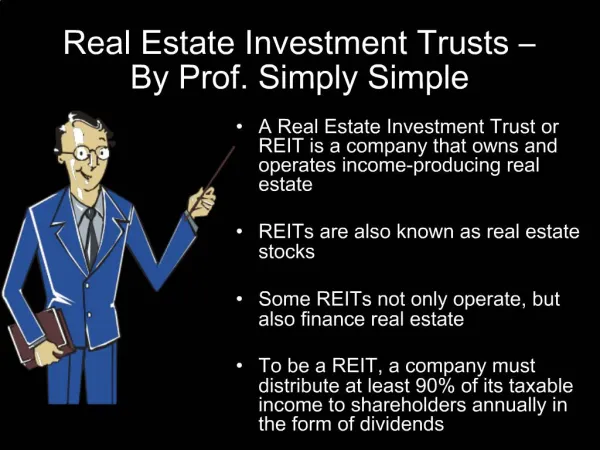

What are REITs? • A REIT is a company that buys, develops, manages and sells real estate assets. • REITs allow participants to invest in a professionally-managed portfolio of real estate properties. • REITs qualify as pass-through entities, companies who are able to distribute the majority of income cash flows to investors without taxation at the corporate level (providing that certain conditions are met). • Managed by a board of directors or trustees • Minimum of 100 shareholders • Pays dividends of at least 90 percent of REIT's taxable income • At least 75 percent of total investment assets must be in real estate • Derive at least 75 percent of gross income from rents or mortgage interest • Dividend Yield = Dividend per share / Price per share = 8% – 12%

Type of REITs • Equity REITs (96.1%) own and operate income-producing real estate. Their revenues come principally from their properties' rents. • Mortgage REITs (1.6%) lend money directly to real estate owners and operators or extend credit indirectly through the acquisition of loans or mortgage-backed securities. Their revenues are generated primarily by the interest that they earn on the mortgage loans. • Hybrid REITs (2.3%) both own properties and make loans to real estate owners and operators.

Other Classifications • Type of property ... Some REITs invest in a variety of property types: shopping centers, apartments, warehouses, office buildings, hotels, etc. Other REITs specialize in one property type only, such as shopping centers or factory outlet stores. • Geographic focus ... Some REITs invest throughout the country. Others specialize in one region only, or even a single metropolitan area.

What to look for… • Check the prospectus or annual report for REITs with established track records. • Look for managers who have weather several real estate cycles. • Look for management teams that have been together for awhile. • Look for REITs that have recently added a new source of funding (the institution must feel comfortable with management).

What to look for… • Focus on REITs with high levels of institutional and insider ownership. A minimum of 10% of outstanding shares is recommended. Inside ownership averages 18% for the REITs tracked by New York-based Cohen & Steers Capital Management. • Is executive compensation tied to appreciation in the stock price? • It's important that the individual REITs are diversified by property type and geographic location.

What to look for… • Don't be lured by high yields alone. • A good measure to look at is Funds From Operations (does not include depreciation). Be sure to look at the age of the companies assets. • Check the debt levels. Institutional investors suggest debt levels no higher than 35% of total capitalization. Also, REITs with a lot of variable-rate debt will be hurt if rates keep rising. • When analyzing prices use the funds for operations to calculate a cash flow multiple. Current cash flow multiples range from 8 to 15, depending on the properties.

Strengths and Weaknesses • Strengths: • Dividends are higher than those of common stocks. • The performance of a REIT follows the real estate market closer than the stock market. • Weaknesses: • Dividends are taxed at the same rate as income tax, so the higher dividends mean you will likely pay more taxes on it. • Mortgage REITs tend to do poorly as interest rates are rising.

REIT Clienteles • People with low marginal tax rates • Individuals interested in fixed income securities • Pension funds and insurance companies • People in high marginal tax brackets who can put REITs in tax-advantaged accounts

References • http://www.nareit.com/ • http://www.investopedia.com/categories/realestate.asp • http://www.reitnet.com/main.phtml

? Too Bad…. Save them for later!!!