Download

1 / 29

290 likes | 298 Views

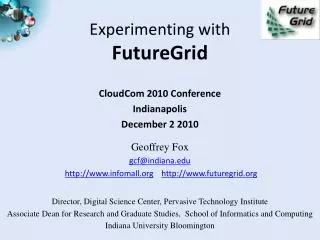

Experimenting with mobile money. William Jack Georgetown University Based on research with Alev Gurbuz , James Habyarimana and Tavneet Suri. Africa Growth Forum, 2015 UNCC, Addis Ababa, Ethiopia. The solution:. The problem:. Customer and Agent growth. 2011. 2009. 2010. Agents.

E N D

Experimenting with mobile money William Jack Georgetown University Based on research with AlevGurbuz, James Habyarimanaand TavneetSuri Africa Growth Forum, 2015 UNCC, Addis Ababa, Ethiopia

The solution: The problem:

Customer and Agent growth 2011 2009 2010 Agents Customers Customers 2008 Agents 2007

Visualizing financial inclusion (Gurbuz) Excluded Informal Formal

M-PESA as a risk spreading tool (Suri) • Four-year panel survey of 3,000 households, 2007-2010 • Negative shocks reduce consumption by about 7% - 10% • But M-PESA users see no fall in consumption • That is, M-PESA users are fully insured

Long run effects of M-PESA (Suri) • Can M-PESA change the level of consumption, not just it’s variance? • Possible impacts on: • Occupational choice: farming business? • Migration: seasonal or permanent? • Use a long-run follow up survey of our sample in 2014 to assess these impacts

Mobile financial services • Savings • Credit • Subsidies

Savings: High Hopes(Habyarimana) • How can savings be boosted? • Increase salience of saving • Provide information about future costs • Reduce transaction costs • Mobile Money savings account • Reduce temptation • Commitment Savings Account • Increase awareness • Regular text reminders

Mobile savings solutions Lock Savings Account Interest bearing mobile money bank account Mobile money transfer service • Additional 1% interest • 1-6 month maturity • Goal set • Early withdraws: • Lose bonus interest • 48 hour waiting period • 1-5% interest • Loan facility

Context of our study • Three counties in Kenya • Kisumu, Nyeri, Kilifi • Geographic, ethnic, and linguistic diversity • Target parents of final year primary school students • Six month window ahead of transition to high school

Design: school-based randomization • All groups received information on the importance of saving for high school

Sampling and randomization Kisumu Nyeri Kilifi 3 Counties • 3 x 120 school meetings • 13 without Std 8 • 2 refused • 7 with no parents 338 x ~14 parents

School meeting • Introduction to High Hopes and consent • Parental engagement • Importance of high school • Thinking about the costs of high school • Encouragement to save • 15 minute baseline survey • Treatment administration • Members of T1 and T2 assisted in opening accounts if desired • T2 invited to convert maturity to January 5, 2015

Timeline Primary school exams end High school starts { { Endline school-based interviews n = 3,215 Endline invitation letters sent Lock boxes mature Jan 5, 2015 Baseline and recruitment n = 4,713 Endline invitation calls and SMSs Endline phone interviews n= 934 Re-contact rate: 88%

M-Shwari take-up Post- Post- Post- Pre- Pre- Pre-

M-Shwari opening dates Control Treatment 2 Treatment 1

LSA take-up Post-

LSA Maturity Dates January 5, 2015 Control Treatment 2 Treatment 1

Results Stay tuned

Credit (Suri) • Sustainable credit requires screening of bad risks • But group-based lending and high deposits can choke off demand • Asset collateralization is rare – especially for small, easy to hide, assets

Mobile credit:making credible the threat of repossession dis • Small solar power units purchased on credit • Cost: $75 • Down-payment: $5 • Repayment via mobile money • Remote penalties and shut-off both feasible

Design Sample: 1,850 small retailers Ex ante assignment Control I. PAYG II. Weekly repayments Ex post assignment II(a). Full enforcement II(b). No penalty III(c). No enforcement

Results • Penalties increase repayment somewhat • Even with complete lack of enforcement, many people still repay • Reputations important? • Kerosene use falls – health benefits

Subsidies delivered over the mobile network • Maternal health care vouchers and transfers (both conditional and unconditional) • Implemented in rural western Kenya • Meaningful impacts on assisted deliveries • CCTs just as effective as maternal vouchers