Download

1 / 14

140 likes | 257 Views

OVERSIGHT & CONSULTATION. KEY ACCOUNTABILITY OVERSIGHT CONSULTATION/ADVICE. IESBA’s Mission. To serve the public interest, by: Setting high quality ethical standards, including independence standards Facilitating convergence of international and national standards

E N D

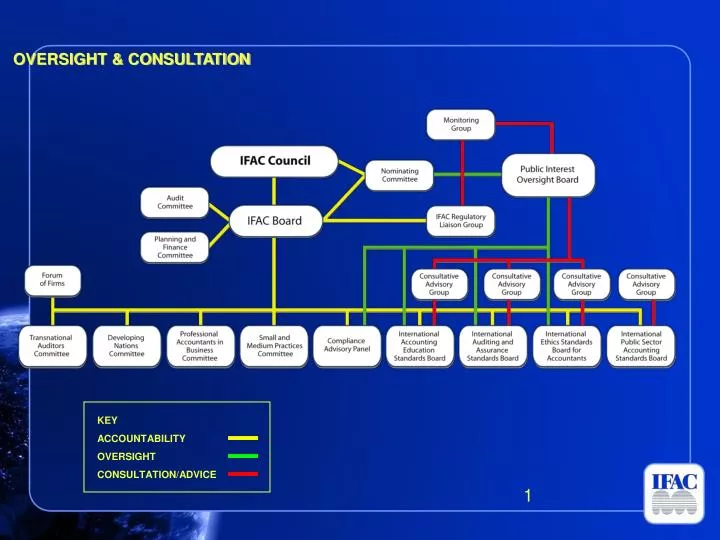

OVERSIGHT & CONSULTATION KEY ACCOUNTABILITY OVERSIGHT CONSULTATION/ADVICE

IESBA’s Mission • To serve the public interest, by: • Setting high quality ethical standards, including independence standards • Facilitating convergence of international and national standards • Result = enhanced quality of services and strengthened confidence in the accounting profession

2003 IFAC Reforms • Ensure that IFAC activities are responsive to the public interest • Increased transparency • Greater public and regulatory input • Increased dialogue with regulators • Created the PIOB, IESBA CAG, and the Monitoring Group

Monitoring Group • International regulators/organizations • International Organization of Securities Commissions • Basel Committee on Banking Supervision • European Commission • International Association of Insurance Supervisors • World Bank • Financial Stability Board • Monitors 2003 IFAC Reforms • Works closely with the PIOB • Provides consultation to the CAG and PIACs

Consultative Advisory Group Provides advice on IESBA’s agenda, work plan, and priorities Provides technical advice on projects Members interested in development of high quality ethical standards for professional accountants CAG Chair attends IESBA meetings and is a member of the IESBA’s Planning Committee Meets twice a year, meetings are public

Members of the CAG • Asian Financial Executives’ Institutes • Auditing Practices Board • Basel Committee on Banking Supervisions • BusinessEurope • CFA Institute • European Federation of Accountants and Auditors for SMEs

Members of the CAG (continued) European Federation of Financial Executives' Institutes Fédération des Experts Comptables Européens Gulf State Regulatory Authorities Graduate School of Finances and Management, Russia IAASB CAG Institute of Internal Auditors International Organization of Securities Commissions (IOSCO) 7

Members of the CAG (continued) International Organization of Supreme Audit Institutions (INTOSAI) North American Financial Executives Institutes Public Company Accounting Oversight Board (PCAOB) Sri Lanka Accounting and Auditing Standards Monitoring Board (SLAASMB) World Bank World Federation of Exchanges 8

PIACs • The IESBA is one of three “public interest activity committees” • PIACs are IFAC standard-setting bodies that have the greatest impact on the public interest • Other PIACS are • IAESB • IAASB

IESBA • 18 voting members • 9 practitioners and 9 non practitioners • 10 member bodies, 5 forum of firms, 3 public representatives • 2/3 members required for approval • 4 observers • CAG Chair • European Commission • Japanese FSA • Public Company Accounting Oversight Board

IESBA Planning Committee • Ken Dakdduk, Chair • Michael Niehues • Isabelle Sapet • Bob Franchini • Volker Röhricht • Richard Fleck

Forum of Firms Association of international networks of accounting firms Currently 21 members Conducts its business through Transnational Auditors Committee (TAC) Membership obligation – for transnational audits, including all listed entities, have policies and methodologies that conform to the Code

Other • Definition of public accountant – need for consistent definition within IFAC • Corporate governance – IFAC focus • European Commission – current priorities 13