Download

1 / 55

550 likes | 553 Views

Learn the differences between managerial and financial accounting, manufacturing cost terms, cost accounting systems, and job order costing for both manufacturing and service businesses.

E N D

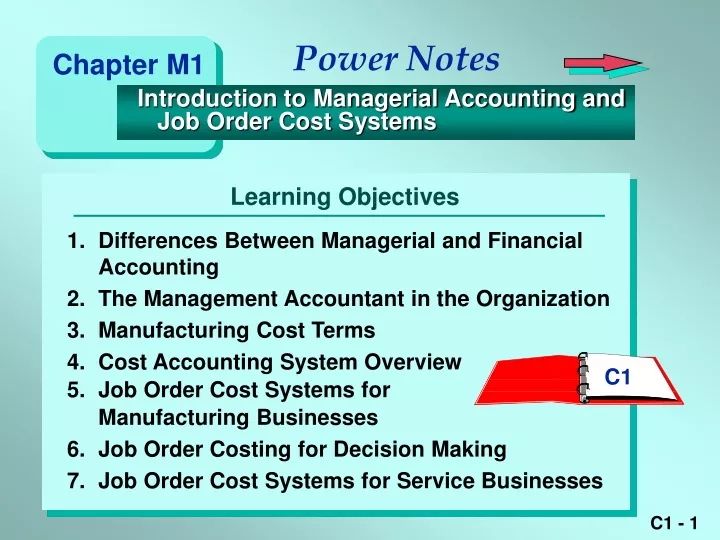

Power Notes Chapter M1 Introduction to Managerial Accounting and Job Order Cost Systems 1. Differences Between Managerial and Financial Accounting 2. The Management Accountant in the Organization 3. Manufacturing Cost Terms 4. Cost Accounting System Overview 5. Job Order Cost Systems for Manufacturing Businesses 6. Job Order Costing for Decision Making 7. Job Order Cost Systems for Service Businesses Learning Objectives C1

Power Notes Chapter M1 Introduction to Managerial Accounting and Job Order Cost Systems Slide # Power Note Topics • 3 • 10 • 18 • 29 • 33 • 51 • Financial and Managerial Accounting • Manufacturing Costs • Cost Accounting Systems • Materials, Labor, Factory Overhead • Predetermined Factory Overhead • Journal Entries in a Job Order Cost System Note: To select a topic, type the slide # and press Enter.

Financial and Managerial Accounting Financial Accounting Managerial Accounting Reports Based Primarily On Usefulness to External Users Usefulness to Management

Financial and Managerial Accounting Financial Accounting Managerial Accounting Users of Accounting Information Shareholders Creditors Government General Public Management Management

Financial and Managerial Accounting Financial Accounting Managerial Accounting Reporting Characteristics Objective Objective and subjective Standard reporting format according to generally accepted accounting principles Flexible reporting formats according to management needs Reports prepared to provide information about the business as a whole Reports prepared to provide information about business segments, divisions, products, etc.

Organization Chart – Line and Staff Responsibilities Board of Directors President, CEO Vice-President Finance, CFO Vice-President Personnel Vice-President Sales Vice-President Production

Organization Chart – Line and Staff Responsibilities Board of Directors President, CEO Vice-President Finance, CFO Vice-President Personnel Vice-President Sales Vice-President Production Controller Manager Conyers Plant Manager Union Point Plant Manager Norcross Plant Treasurer

Organization Chart – Line and Staff Responsibilities Board of Directors President, CEO Vice-President Finance, CFO Vice-President Personnel Vice-President Sales Vice-President Production Controller Manager Conyers Plant Manager Union Point Plant Manager Norcross Plant Treasurer Staff responsibilities Line responsibilities

Organization Chart – Line and Staff Responsibilities Board of Directors President, CEO Vice-President Finance, CFO Vice-President Personnel Vice-President Sales Vice-President Production Controller Manager Conyers Plant Manager Union Point Plant Manager Norcross Plant Treasurer Staff responsibilities Line responsibilities

Cost Classifications Direct Materials Product Costs Direct Labor Factory Overhead Selling Expenses Period Costs Administrative Expenses

Manufacturing Costs Direct Materials: 1. Enters directly into the product. 2. Is significant amount of total product cost. 1. Enters directly into manufacturing the product. 2. Is significant amount of total product cost. Cost other than direct materials cost and direct labor cost incurred in the manufacturing of product. Direct Labor: Factory Overhead:

Manufacturing Cost Flows and Classifications Costs Product Costs Balance Sheet Materials Purchases Direct Labor Factory Overhead Income Statement Period Costs Selling and Administrative

Manufacturing Cost Flows and Classifications Costs Product Costs Balance Sheet Materials Inventory Materials Purchases Direct Labor Factory Overhead Income Statement Period Costs Selling and Administrative

Manufacturing Cost Flows and Classifications Costs Product Costs Balance Sheet Materials Inventory Materials Purchases Direct Labor Work in Process Inventory Factory Overhead Income Statement Period Costs Selling and Administrative

Manufacturing Cost Flows and Classifications Costs Product Costs Balance Sheet Materials Inventory Materials Purchases Cost of Goods Manufactured Direct Labor Work in Process Inventory Factory Overhead Income Statement Finished Goods Inventory Period Costs Selling and Administrative

Manufacturing Cost Flows and Classifications Costs Product Costs Balance Sheet Product costs flow through the balance sheet to the income statement Materials Inventory Materials Purchases Direct Labor Work in Process Inventory Factory Overhead Income Statement Finished Goods Inventory Cost of Goods Sold Period Costs Selling and Administrative

Manufacturing Cost Flows and Classifications Costs Product Costs Balance Sheet Materials Inventory Materials Purchases Period costs flow directly to the income statement Direct Labor Work in Process Inventory Factory Overhead Income Statement Finished Goods Inventory Cost of Goods Sold Period Costs Selling and Administrative Selling and Administrative

Cost Accounting Systems Focus Information to manage manufacturing operations. 1. Product costs to be used for pricing and other management decisions. 2. Costs incurred by each department or process to be used for cost control. 3. Inventory and Cost of Goods Soldbalances to be reported on financial statements. Information Provided

Cost Accounting Systems Job Order Cost System 1. Many different jobs are worked on during each period and unit costs are computed by job. 2. Costs are accumulated using a job cost sheet. 1. A single product is produced on a continuous basis and unit costs are computed by department. 2. Costs are accumulated and reported using a departmental production report. Process Cost System

DM Direct materials used in production Flow of Costs in Perpetual Inventory Accounts Materials Work in Process Finished Goods DM DM Materials Purchased Cost of Goods Sold Factory Overhead Wages Payable Total Wages

Flow of Costs in Perpetual Inventory Accounts Materials Work in Process Finished Goods DM DM Materials Purchased IM Cost of Goods Sold Factory Overhead Wages Payable IM Total Wages IM Indirect materials used in production

DL Direct labor used in production Flow of Costs in Perpetual Inventory Accounts Materials Work in Process Finished Goods DM DM Materials Purchased DL IM Cost of Goods Sold Factory Overhead Wages Payable IM DL Total Wages

Flow of Costs in Perpetual Inventory Accounts Materials Work in Process Finished Goods DM DM Materials Purchased DL IM Cost of Goods Sold Factory Overhead Wages Payable IM DL Total Wages IL IL IL Indirect labor used in production

Flow of Costs in Perpetual Inventory Accounts Materials Work in Process Finished Goods DM DM Materials Purchased DL IM Cost of Goods Sold Factory Overhead Wages Payable IM DL Total Wages IL IL OFOH OFOH Other factory overhead costs incurred during production

FOHA Factory overhead applied to work in process Flow of Costs in Perpetual Inventory Accounts Materials Work in Process Finished Goods DM DM Materials Purchased DL IM FOHA Cost of Goods Sold Factory Overhead Wages Payable IM DL FOHA Total Wages Based on predetermined overhead rate IL IL OFOH

COGM Cost of goods manufactured and transferred to finished goods Flow of Costs in Perpetual Inventory Accounts Materials Work in Process Finished Goods DM DM Materials Purchased COGM COGM DL IM FOHA Cost of Goods Sold Factory Overhead Wages Payable IM DL FOHA Total Wages IL IL OFOH

SOLD Finished goods sold Flow of Costs in Perpetual Inventory Accounts Materials Work in Process Finished Goods DM DM SOLD Materials Purchased COGM COGM DL IM FOHA Cost of Goods Sold Factory Overhead Wages Payable SOLD IM DL FOHA Total Wages IL IL OFOH

Flow of Costs in Perpetual Inventory Accounts Materials Work in Process Finished Goods DM DM SOLD Materials Purchased COGM COGM DL IM FOHA Cost of Goods Sold Factory Overhead Wages Payable SOLD IM DL FOHA Total Wages Based on predetermined overhead rate IL IL OFOH Summary of cost flows

Materials Information and Cost Flows Job 71 1,000 units of American History Balance $ 3,000 Direct Materials Direct Labor Factory Overhead Materials Requisitions Job 72 4,000 units of Algebra Direct Materials Direct Labor Factory Overhead

Materials Information and Cost Flows Job 71 1,000 units of American History Balance $ 3,000 Direct Materials 2,000 Direct Labor Factory Overhead Materials Requisitions Job 72 4,000 units of Algebra Direct Materials $11,000 Direct Labor Factory Overhead

Labor Information and Cost Flows Job 71 1,000 units of American History Balance $ 3,000 Direct Materials 2,000 Direct Labor Factory Overhead Time Tickets Job 72 4,000 units of Algebra Direct Materials $11,000 Direct Labor Factory Overhead

Labor Information and Cost Flows Job 71 1,000 units of American History Balance $ 3,000 Direct Materials 2,000 Direct Labor 3,500 Factory Overhead Time Tickets Job 72 4,000 units of Algebra Direct Materials $11,000 Direct Labor 7,500 Factory Overhead

Estimated total factory overhead costs Predetermined factory overhead rate = Estimated activity base Predetermined Factory Overhead Rates 1. Direct labor hours 2. Direct labor dollars 3. Machine hours 4. Direct materials 5. Other Activity base examples

Estimated total factory overhead costs Predetermined factory overhead rate = Estimated activity base Predetermined Factory Overhead Rates It is a tradeoff between accuracy and timeliness. If a company waited until the end of an accounting period, when all overhead costs are known, the allocated factory overhead would be accurate but not timely. Why is the predetermined overhead rate calculated from estimated numbers at the beginning of the period?

Estimated total factory overhead costs Estimated activity base $50,000 estimated factory overhead costs 10,000 estimated direct labor hours Predetermined Factory Overhead Rates Predetermined factory overhead rate = =

Estimated total factory overhead costs Estimated activity base $50,000 estimated factory overhead costs 10,000 estimated direct labor hours Predetermined Factory Overhead Rates Predetermined factory overhead rate = $5 per direct labor hour =

Estimated total factory overhead costs Estimated activity base $50,000 estimated factory overhead costs 10,000 estimated direct labor hours Predetermined Factory Overhead Rates Predetermined factory overhead rate = $5 per direct labor hour = For each direct labor hour worked, factory overhead applied is $5. Direct Factory Labor Overhead Hours Applied Job 71 350 x $5 = $1,750 Job 72 500 x $5 = $2,500

Assigning Factory Overhead to Jobs Job 71 1,000 units of American History Balance $ 3,000 Direct Materials 2,000 Direct Labor 3,500 Factory Overhead Time Tickets Predetermined Overhead Rates Job 72 4,000 units of Algebra Direct Materials $11,000 Direct Labor 7,500 Factory Overhead

Assigning Factory Overhead to Jobs Job 71 1,000 units of American History Balance $ 3,000 Direct Materials 2,000 Direct Labor 3,500 Factory Overhead 1,750 Time Tickets Predetermined Overhead Rates Job 72 4,000 units of Algebra Direct Materials $11,000 Direct Labor 7,500 Factory Overhead 2,500

Summary of Job Cost Sheets Job 71 1,000 units of American History Balance $ 3,000 Direct Materials 2,000 Direct Labor 3,500 Factory Overhead 1,750 Total Job Cost $10,250 Job 72 4,000 units of Algebra Direct Materials $11,000 Direct Labor 7,500 Factory Overhead 2,500 $21,000 Total of debits to Work in Process

Recording Factory Overhead Factory Overhead $4,400 ACTUAL Based on actual costs incurred

Recording Factory Overhead Factory Overhead $4,400 $4,250 ACTUAL Based on actual costs incurred APPLIED Based on estimated rate ($5 x 850 hrs) What account is charged (debited)? Is factory overhead overapplied or underapplied?

Recording Factory Overhead Factory Overhead $4,400 $4,250 ACTUAL Based on actual costs incurred APPLIED Based on estimated rate ($5 x 850 hrs) Work in Process is charged (debited). $150 BALANCE Underapplied How would this balance be closed at year end?

Recording Factory Overhead Factory Overhead $4,400 $4,250 ACTUAL Based on actual costs incurred APPLIED Based on estimated rate ($5 x 850 hrs) Work in Process is charged (debited). $150 BALANCE Underapplied An immaterial balance is closed to Cost of Goods Sold at year end.

Job Cost Sheets and Work in Process Job 71 1,000 units Balance $ 3,000 Direct Materials 2,000 Direct Labor 3,500 Factory Overhead 1,750 Total Job Cost $10,250 Job 72 4,000 units Balance $ 0 Direct Materials 11,000 Direct Labor 7,500 Factory Overhead 2,500 $21,000 WORK IN PROCESSBalance Date Item Debit Credit Debit Credit Dec. 1 Balance 3,000 31 Direct materials 13,000 16,000 31 Direct labor 11,000 27,000 31 Factory overhead 4,250 31,250 31 Jobs completed 10,250 21,000

Job Cost Sheets and Work in Process Job 71 1,000 units Balance $ 3,000 Direct Materials 2,000 Direct Labor 3,500 Factory Overhead 1,750 Total Job Cost $10,250 Job 72 4,000 units Balance $ 0 Direct Materials 11,000 Direct Labor 7,500 Factory Overhead 2,500 $21,000 WORK IN PROCESSBalance Date Item Debit Credit Debit Credit Dec. 1 Balance 3,000 31 Direct materials 13,000 16,000 31 Direct labor 11,000 27,000 31 Factory overhead 4,250 31,250 31 Jobs completed 10,250 21,000

Job Cost Sheets and Work in Process Job 71 1,000 units Balance $ 3,000 Direct Materials 2,000 Direct Labor 3,500 Factory Overhead 1,750 Total Job Cost $10,250 Job 72 4,000 units Balance $ 0 Direct Materials 11,000 Direct Labor 7,500 Factory Overhead 2,500 $21,000 WORK IN PROCESSBalance Date Item Debit Credit Debit Credit Dec. 1 Balance 3,000 31 Direct materials 13,000 16,000 31 Direct labor 11,000 27,000 31 Factory overhead 4,250 31,250 31 Jobs completed 10,250 21,000

Job Cost Sheets and Work in Process Job 71 1,000 units Balance $ 3,000 Direct Materials 2,000 Direct Labor 3,500 Factory Overhead 1,750 Total Job Cost $10,250 Job 72 4,000 units Balance $ 0 Direct Materials 11,000 Direct Labor 7,500 Factory Overhead 2,500 $21,000 WORK IN PROCESSBalance Date Item Debit Credit Debit Credit Dec. 1 Balance 3,000 31 Direct materials 13,000 16,000 31 Direct labor 11,000 27,000 31 Factory overhead 4,250 31,250 31 Jobs completed 10,250 21,000

Job Cost Sheets and Work in Process Job 71 1,000 units Balance $ 3,000 Direct Materials 2,000 Direct Labor 3,500 Factory Overhead 1,750 Total Job Cost $10,250 Job 72 4,000 units Balance $ 0 Direct Materials 11,000 Direct Labor 7,500 Factory Overhead 2,500 $21,000 WORK IN PROCESSBalance Date Item Debit Credit Debit Credit Dec. 1 Balance 3,000 31 Direct materials 13,000 16,000 31 Direct labor 11,000 27,000 31 Factory overhead 4,250 31,250 31 Jobs completed 10,250 21,000

Job Cost Sheets and Work in Process Job 71 1,000 units Balance $ 3,000 Direct Materials 2,000 Direct Labor 3,500 Factory Overhead 1,750 Total Job Cost $10,250 Job 72 4,000 units Balance $ 0 Direct Materials 11,000 Direct Labor 7,500 Factory Overhead 2,500 $21,000 WORK IN PROCESSBalance Date Item Debit Credit Debit Credit Dec. 1 Balance 3,000 31 Direct materials 13,000 16,000 31 Direct labor 11,000 27,000 31 Factory overhead 4,250 31,250 31 Jobs completed 10,250 21,000