Download

1 / 8

80 likes | 220 Views

Forward contract. Or 365 days. F=The forward rate in terms of payment currency. S=The spot rate in terms of payment currency. (R1=Interest on payment currency (yearly. (R2=Interest on basic currency (yearly. Forward contract-Example. Indirect quote. F=The £ Forward rate -BID.

E N D

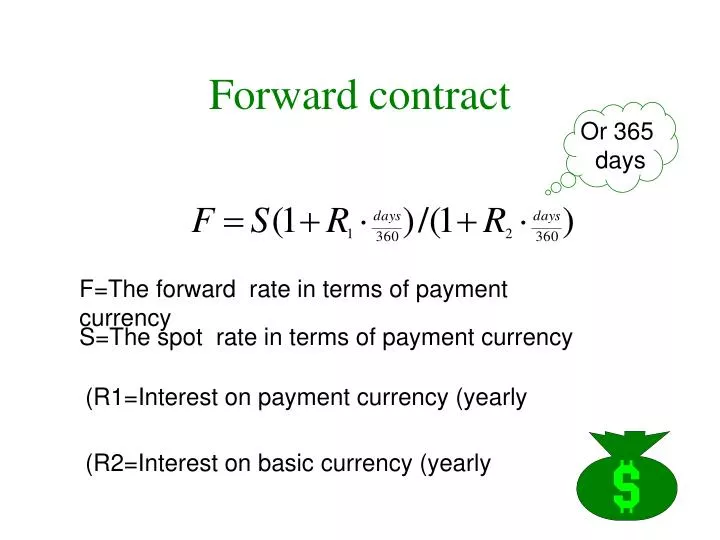

Forward contract Or 365 days F=The forward rate in terms of payment currency S=The spot rate in terms of payment currency (R1=Interest on payment currency (yearly (R2=Interest on basic currency (yearly

Forward contract-Example Indirect quote F=The £ Forward rate -BID S=The £ Spot rate-BID $ R$= Yearly interest on a Deposit in £R £ = Yearly interest on a Loan in

Hedge strategy with forward Canceling the risk by getting to opposite position * If we long the currency - we would sell the forward contract If we have a loan in the currency - we would buy the forward contract *

Example A U.S.A company expects to get 2 millioneuro in 3 months The spot rate is 0.8426 $/Euro The cost of product is 1.4 Euro The company expects a profit of $285,200 The company is exposed to market risk

The strategy With Forward Short a Forward contract on the Euro The company will sell a forward contract for 3 month on the Euro The forward rate is 0.8456 $/Euro The company locked a profit of $291,200

Short fwd ASSET 0.823 0.8456 0.891 Profit Graph Euro/$ (Asset in Euro (long Short the fwd on the Euro

Synthetic Forward With Options Short a Euro Forward = Buy a Euro call and sell a Euro put, the same .strike and the expiry date Buy a Euro put vanilla option, strike .8380 ,expiry 3 months from today Sell a Euro call reverse knock in, strike .8380 with trigger of .887 ,expiry 3 months from today The price of the strategy - zero cost

Short fwd ASSET TRIGGER 0.8456 0.823 0.838 0.887 Profit Synthetic Forward Euro/$ Buy a Euro put vanilla option 0.838 and sell Euro call reverse knock in 0.838 ; trigger 0.887 to the same expiry date at zero cost