Download

1 / 5

E N D

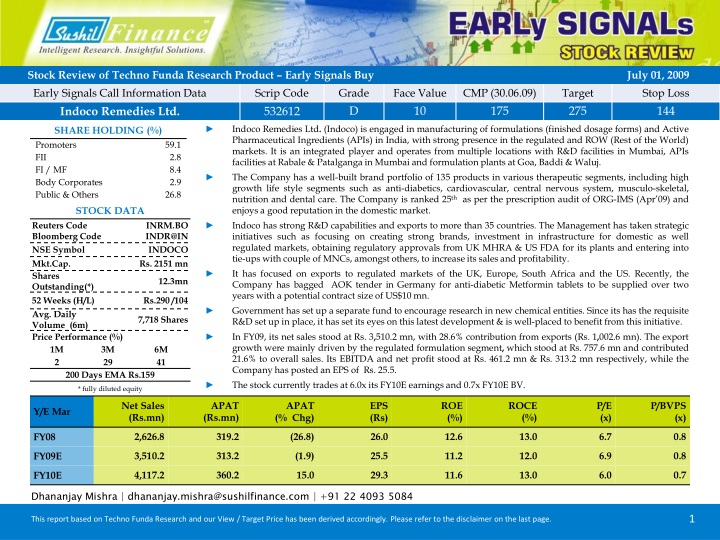

Indoco Remedies Ltd. (Indoco) is engaged in manufacturing of formulations (finished dosage forms) and Active Pharmaceutical Ingredients (APIs) in India, with strong presence in the regulated and ROW (Rest of the World) markets. It is an integrated player and operates from multiple locations with R&D facilities in Mumbai, APIs facilities at Rabale & Patalganga in Mumbai and formulation plants at Goa, Baddi & Waluj. • The Company has a well-built brand portfolio of 135 products in various therapeutic segments, including high growth life style segments such as anti-diabetics, cardiovascular, central nervous system, musculo-skeletal, nutrition and dental care. The Company is ranked 25th as per the prescription audit of ORG-IMS (Apr’09) and enjoys a good reputation in the domestic market. • Indoco has strong R&D capabilities and exports to more than 35 countries. The Management has taken strategic initiatives such as focusing on creating strong brands, investment in infrastructure for domestic as well regulated markets, obtaining regulatory approvals from UK MHRA & US FDA for its plants and entering into tie-ups with couple of MNCs, amongst others, to increase its sales and profitability. • It has focused on exports to regulated markets of the UK, Europe, South Africa and the US. Recently, the Company has bagged AOK tender in Germany for anti-diabetic Metformin tablets to be supplied over two years with a potential contract size of US$10 mn. • Government has set up a separate fund to encourage research in new chemical entities. Since its has the requisite R&D set up in place, it has set its eyes on this latest development & is well-placed to benefit from this initiative. • In FY09, its net sales stood at Rs. 3,510.2 mn, with 28.6% contribution from exports (Rs. 1,002.6 mn). The export growth were mainly driven by the regulated formulation segment, which stood at Rs. 757.6 mn and contributed 21.6% to overall sales. Its EBITDA and net profit stood at Rs. 461.2 mn & Rs. 313.2 mn respectively, while the Company has posted an EPS of Rs. 25.5. • The stock currently trades at 6.0x its FY10E earnings and 0.7x FY10E BV. Dhananjay Mishra | dhananjay.mishra@sushilfinance.com | +91 22 4093 5084 This report based on Techno Funda Research and our View / Target Price has been derived accordingly. Please refer to the disclaimer on the last page.

Indoco Remedies Ltd. • Q4FY09 PERFORMANCE • During Q4FY09, its revenues declined by 2.3% YoY to Rs. 849.9 mn, mainly on account of a 5.6% YoYdegrowth registered in domestic formulations segment at Rs. 576.5 mn. Exports registered 4.4% YoY growth to Rs. 241.4 mn, primarily due to 34.2% YoY growth in semi-regulated formulations segment at Rs. 58.8 mn. However, the regulated formulations and API segments witnessed a fall of 1.1% & 25.6% YoY respectively. • Its EBITDA margins declined by 322 bps to 7.9%, mainly on account of increase in Employee costs as percentage of sales. • The net profit stood at Rs. 39.2 mn. The lower net profit can be attributed to the drop in net sales and contraction in EBITDA margins. while its EPS for the period under review stood at Rs. 3.2. • OTHER BUSINESS UPDATES • In Q4FY09, the domestic formulations Revenues declined by 5.6% over corresponding period last year. However, the products that did well are Sensodent-K, Sensodent-KF, Sensoform, Amclaid, Clamchek, Megachek, Cital, Sperogest. During the quarter, the Company also launched Cef-Vepan 250 mg and 500 mg. • Q4FY09 ended on a historic note with Indoco achieving export sales of Rs. 1 bn for the FY09. Irrespective of the setback to the overall export growth for the country, Indoco registered a growth of 24% for FY09 for the formulation exports. • During the quarter, Tanzania Regulatory Authorities inspected Indoco’s manufacturing plant in Waluj, which now will be used for supplies to Tanzania, and reduces the burden on its Goa manufacturing facility as the until Goa facility was used for such Exports. • Indoco bagged a tender from CMS Sudan worth US$0.34 mn for Lignox 2% to be supplied over a period of 2 years. • Its sterile facility was audited by Slovenian Regulatory Authorities for Carprofen Injection and the Injectable area, now stands approved for supplies in the entire Europe, since Slovenia is a part of EC. • The biggest breakthrough during Q4FY09 came through with an award of AOK tender in Germany for Metformin. The tender award covers all the 3 strengths, viz., 500mg/850mg and 1,000mg, and all the five territories covering the entire Germany. The supplies will be spread over a period of two years and the Company expects a business of over US$10 mn during this period. The 1st supply against the AOK tender has already been dispatched. July 01, 2009

Indoco Remedies Ltd. • R&D ACTIVITIES • The Company has set its eyes on the latest development on a separate fund being created by the Government to encourage research in new chemical entities. With the requisite set up in place, the Company is well-placed to venture into this new area in the near future. • Indoco’s ultra modern R&D centre is spread over an area of 70,000 square feet. The R&D centre has strength of 100 scientists including eight doctorates. • On the formulation front, the Company is developing a strong pipeline in the slow release technology and will provide value added products to the generic companies worldwide. With a strong position in solid dosages and ophthalmic, Indoco has also developed the technology of deciphering the reference products in the quickest and scientific manner to pave a way for the successful introduction for submission and clinical trials of topical and liquid orals. These dosage forms will add substantial value in the future, as Indoco will be one of the few companies offering this expertise. • The Company has also shifted its strategy from going with partners in the US (for filing the ANDAs) to filing on its own. During the next couple of years, Indoco expects to file over a dozen ANDAs in its name. • To increase production capacity & accommodate more products, the Company has successfully expanded its manufacturing facility at Patalganga & Baddi and is on the look out for setting up new plants to augment the rising demands. • The Company has filed COS/DMF in Europe & USA for Metformin (anti-diabetic), Allopurional (anti-hyperuricemia), Ciprofloxacin (antibacterial), BrimonidineTartrate (alpha-2 adrenergic agonist for ophthalmic use), Dicyclomine (anti-spasmodic), Glimepiride (anti-diabetic). The 11 more products are under development & various stages of filing. July 01, 2009

Indoco Remedies Ltd. BALANCE SHEET STATEMENT (Rs.mn) PROFIT & LOSS STATEMENT (Rs.mn) July 01, 2009

Disclaimer As the title suggests, the objective of this report is to provide early signals to investors about stocks, which are likely to witness price up move in medium to long term. Companies are selected based on certain Fundamental / Technical indicators and it may be possible that our view on these stocks may have been formed without meeting the company management. We advise caution as far as investing / disinvesting in these stocks since these stocks are not strictly based on detailed technical / fundamental analysis. All the data appearing in this report is from sources believed to be reliable but we do not guarantee that it is correct or accurate. Additional information with respect to any securities referred to herein will be available upon request. This report is prepared for the exclusive use of Sushil Group clients only and should not be reproduced, re-circulated, published in any media, website or otherwise, in any form or manner, in part or as a whole, without the express consent in writing of Sushil Financial Services Private Limited. Any unauthorized use, disclosure or public dissemination of information contained herein is prohibited. This report is to be used only by the original recipient to whom it is sent. This is for private circulation only and the said document does not constitute an offer to buy or sell any securities mentioned herein. While utmost care has been taken in preparing the above, we claim no responsibility for its accuracy. We shall not be liable for any direct or indirect losses arising from the use thereof and the investors are requested to use the information contained herein at their own risk. This report has been prepared for information purposes only and is not a solicitation, or an offer, to buy or sell any security. It does not purport to be a complete description of the securities, markets or developments referred to in the material. The information, on which the report is based, has been obtained from sources, which we believe to be reliable, but we have not independently verified such information and we do not guarantee that it is accurate or complete. All expressions of opinion are subject to change without notice. Sushil Financial Services Private Limited and its connected companies, and their respective directors, officers and employees (to be collectively known as SFSPL), may, from time to time, have a long or short position in the securities mentioned and may sell or buy such securities. SFSPL may act upon or make use of information contained herein prior to the publication thereof. July 01, 2009