Download

1 / 25

250 likes | 367 Views

Growing Your Retirement Savings Without Growing Your Tax Burden:. HOW TO CREATE TAX-FREE INCOME IN RETIREMENT (presenter). Overview of Today’s Presentation. WE HAVE MONEY SAVED FOR RETIREMENT IN: Traditional IRAs 401(k)’s 403(b)’s Other retirement accounts that defer taxes.

E N D

Growing Your Retirement SavingsWithout Growing Your Tax Burden: HOW TO CREATE TAX-FREE INCOME IN RETIREMENT(presenter)

Overview of Today’s Presentation WE HAVE MONEY SAVED FOR RETIREMENT IN: • Traditional IRAs • 401(k)’s • 403(b)’s • Other retirement accounts that defer taxes

Overview of Today’s Presentation Over time, we want and expect our savings to grow.

Overview of Today’s Presentation But as our retirement savings grows, so does the tax burden associated with it. That’s because taxes are deferred, not eliminated.

Overview of Today’s Presentation WHO PAYS THESE TAXES? YOU – when you take withdrawals YOUR HEIRS – when they receive the money … and as your balance grows, so do the deferred taxes.

Overview of Today’s Presentation What we really want is our savings to grow, but the taxes to not grow.

Overview of Today’s Presentation HOW DO WE DO THAT? How do we grow our retirement savings … while not growing the deferred tax burden? Answer: By doing a Roth IRA Conversion today

Overview of Today’s Presentation A Roth IRA conversion generally entails paying taxes on the accumulated IRA balance now … and thereby stopping the tax burden from continuing to grow … because once the money is in a Roth IRA, you create the opportunity to owe no taxes on any future growth in the IRA balance.

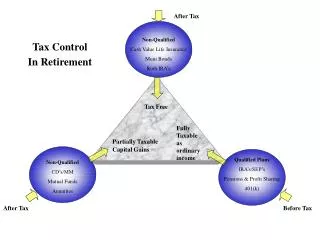

Your Current Tax Treatment • TAX TREATMENT OF TRADITIONAL IRAS • Withdrawals of deductible contributions and growth are taxable • Withdrawals are required starting at age 70½ • At death, beneficiaries are taxed on the IRA balance • Less favorable if you are in a higher tax bracket when you take withdrawals than you are now

Will Tax Rates Increase? No one can say for certain, but let’s look at two key facts: Source: Tax Policy Center

Will Tax Rates Increase? No one can say for certain, but let’s look at two key facts: Source: Office of Management and Budget

Let Me Ask You … If you believed that tax rates were going to go up in the future … If there was a way to pay taxes now on the existing balance of your IRA (at a lower rate) to avoid paying taxes on that balance later (at a higher rate) … And if doing so also provided an opportunity to avoid incometaxes altogether on the future growth of your IRA … Would you be interested?

Your Future Tax Treatment • TAX TREATMENT OF ROTH IRAS • Withdrawals are not taxable if the balance is held in the Roth IRA for at least five years and not withdrawn prior to age 59½ • Withdrawals are not required starting at age 70½ • At death, beneficiaries are not taxed on the IRA balance • More favorable if you are in a higher tax bracket when you take withdrawals than you are now

Your Future Tax Treatment Roth IRAs can provide a cash flow in retirement that is 100% free of income taxes Future interest and investment gains are not taxed at all as long the rules are followed

Roth IRA Conversion SO, HOW DO I GET FROM WHERE I AM …

Roth IRA Conversion … TO WHERE I WANT TO BE?

Roth IRA Conversion BY DOING … A ROTH IRA CONVERSION. Pay taxes now on your current IRA balance to prevent paying taxes later on your future balance.

Roth IRA Conversion WHY HASN’T ANYONE MENTIONED THIS TO YOU BEFORE? Because prior to 1/1/2010, If your household taxable income exceeded $100,000, You were not allowed to do it! Thanks to the Tax Increase Prevention and Reconciliation Act of 2005, you now can!

Roth IRA Conversion IN FACT … Also thanks to the Tax Increase Prevention and Reconciliation Act of 2005… You can do a conversion in 2010 And report the income ½ on your 2011 return and ½ on your 2012 return

Roth IRA Conversion LET’S DO IT!

Roth IRA Conversion WHAT ARE THE MECHANICS OF GETTING THIS DONE? • Let’s meet one-on-one to plan this properly • We’ll evaluate whether this is the right move for you • We’ll calculate the amount you would need to pay in taxes upon conversion • We’ll make sure you have funds outside the IRA to pay the taxes • We’ll plan whether you should do this all in 2010 or spread it out over time

Roth IRA Conversion WHAT ARE THE MECHANICS OF GETTING THIS DONE? • We’ll set up a Roth IRA • And we’ll handle the funds as a trustee-to-trustee transfer so the money doesn’t get lost and so you don’t have to pay any more taxes than required

Roth IRA Conversion WHAT ARE THE MECHANICS OF GETTING THIS DONE? • We’ll make sure you understand the rules to get all of the future interest and investment gains in the Roth IRA tax-free • In general, the rules are: • No withdrawals prior to age 59½ • No withdrawals until the Roth IRA account has been established for 5 years • Any money you need prior to that 5-year mark, we’ll leave in your traditional IRA

Thank You LET’S SCHEDULE AN APPOINTMENT!

The information provided here has been taken from third party sources and is deemed to be reliable, but is not guaranteed. It is believed to be accurate at the time of printing, but is subject to change at any time. It is provided for informational purposes only, and you should consult with a tax/legal advisor for further information. Please note that neither Insurance Insight Group LLC nor the presenter provide tax or legal advice. No party assumes liability for any loss or damage resulting from errors or omissions in the use of this material. This material is intended to provide general information only. It is not intended to render tax, legal, accounting, or investment advice, and the services of qualified professionals should be sought.