Download

1 / 9

100 likes | 187 Views

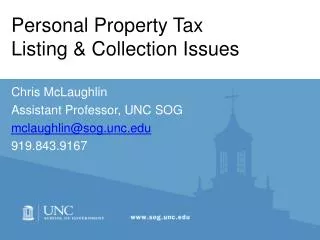

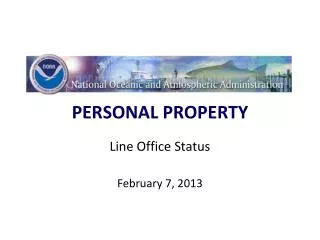

REFORMING. personal property tax. THE PLAN. NEW GF REVENUE. STATE USE TAX TRANSFER TO LOCALS. EXPIRED. LOCAL USE TAX. GENERAL FUND. STATE USE TAX. CREDITS. STATE + USE TAX. LOCAL. cannot exceed 6%. under the Constitution. WHAT IS USE TAX?.

E N D

REFORMING personal property tax

THE PLAN NEW GF REVENUE STATE USE TAX TRANSFER TO LOCALS EXPIRED • LOCALUSE TAX GENERAL FUND • STATE USE TAX • CREDITS

STATE + USE TAX LOCAL cannot exceed 6% under the Constitution

WHAT IS USE TAX? Use tax is sales tax on: - out of state purchases - telecom • lodging • - 4¢ general fund • 2¢ school aid fund

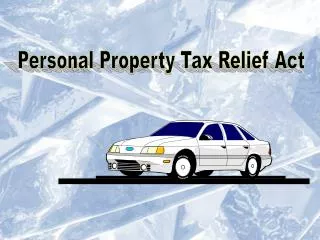

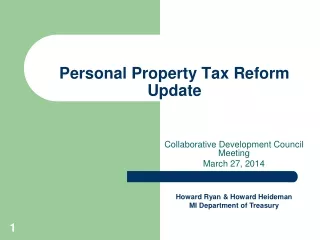

REIMBURSEMENT 100% 80% POLICE FIRE AMBULANCE JAILS K-12/ISDOPERATING AND DEBT LOSS LOST TIF CAPTURE EVERYTHING ELSE

REIMBURSEMENT FY 2014 AND 2015 LOCAL TAXING UNIT LOCAL SCHOOL DISTRICT ISD FY 2016 AND BEYOND Calculate essential services loss – up to 100% of that amount made up through locally levied Essential Services Assessment (ESA) Basic operating loss - 100% of that amount made up through SAF The legislature shall appropriate an amount to cover all debt loss Calculate debt/operating loss – 100% of that amount made up through use tax distribution Calculate debt loss and hold harmless/out-of-formula operating loss – 100% of that amount made up through use tax distribution Calculate remaining loss amount, not including loss eligible for reimbursement through ESA – 80% of that amount made up through use tax distribution Calculate sinking fund/recreational mill loss – 80% of that amount made up through use tax distribution

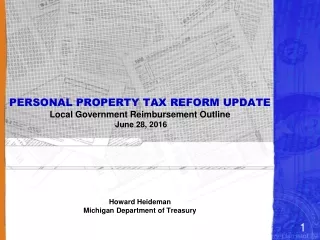

UNREIMBURSED EXEMPTIONS VS. TOTAL LOCAL REVENUEFY 2023 (EST) Amount Not Reimbursed $64.9 M Total PPT Cut $576.6 M 0.137% of General Revenue Total Reimbursement $511.7 M Total General Revenue $47.4 B

PROJECTED GROWTH OF EXEMPT PP REVENUE VS. USE TAX REVENUE 2023-2033 Projected growth in revenue from exempt personal property, assuming no exemption: $30.3 M $600 Projected growth in Use Tax revenue: $582 M $400 $200 $0 2023 2033

REFORMING personal property tax