Download

1 / 24

240 likes | 376 Views

COMPETITION ISSUES AND PRICING POLICY. Nonkululeko Nyembezi-Heita CEO, ArcelorMittal South Africa 19 October 2009. Agenda. Introduction Competition Commission Our Cases Our Pricing Compliance Our Vision.

E N D

COMPETITION ISSUES AND PRICING POLICY Nonkululeko Nyembezi-HeitaCEO, ArcelorMittal South Africa19 October 2009

Agenda • Introduction • Competition Commission • Our Cases • Our Pricing • Compliance • Our Vision

There are several reasons to believe that the steel industry of today has cleaned up its act. The main player, ArcelorMittal SA, is now owned by the Mittal Group, which faces international scrutiny and has entirely changed its local pricing structure to one that is more transparent and impossible to manipulate. Bottom Line Column, Business Day, 25th September 2009

Introduction • We have been in the spotlight recently regarding competition issues. • Present cases relate primarily to legacy issues. • An opportunity to explain our stance openly and transparently. • Previously an incumbent state firm, today a modern competitive multinational. • ArcelorMittal has rigorous compliance practices in place, including regular training to help prevent and prohibit anti-competitive practices. • Our leadership upholds the highest ethical standards and will not tolerate any behaviour that is at odds with our code of business conduct or detracts from the sustainable long term success and vision of the company. • Financial performance indicates our vulnerability to market forces.

Agenda • Introduction • Competition Policy • Our Cases • Our Pricing • Compliance • Our Vision

Competition law has become stricter in the past 10 years and the competition authorities have become more aggressive in their investigation of potential collusion. SA has moved away from the “laager mentality” of the apartheid years and is trying to uphold international standards. Bottom Line Column, Business Day, 25th September 2009

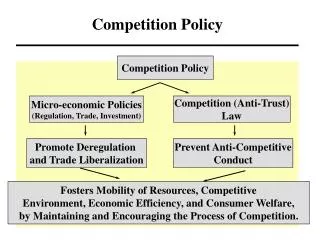

SA Competition Law Background to the Commission’s actions 2009: Competition Law Amendment Act 1998: Competition Act, 1998 (Act No, 89 of 1998) passed by Parliament. Competition Commission,Tribunal & Appeal Court established. • In the 1990’s there were only 14 functioning competition authorities in the world • Today there are nearly 100 • With them, a new broad culture in regard to competition • Competition Commission was tasked with addressing market dominance • Authorities today are driven by the need to introduce competition to the market 1994: White Paper on Reconstruction & Development signals need to review local competition law 1979 Act: Competition Board established Growing mandate… 2000 1980 1990 2010 1986 review: Competition Board empowered to act against new concentrations of economic power & existing monopolies and oligopolies 1995: DTI embarks on 3 year project to arrive at a new competition policy framework

Increased Enforcement in SA • Peak of cases referred in the 2006/07 reporting year. • There has been a substantial increase in the number of section 4 contraventions referred, especially of the hardcore cartel contraventions of 4(1)(b). • The size of administrative penalties imposed by the Tribunal has also increased substantially over time. • Increased emphasis on cartels in South Africa is in line with developments globally, as competition authorities have stepped up their enforcement efforts.

Agenda • Introduction • Competition Commission • Our Cases • Our Pricing • Compliance • Our Vision

ArcelorMittal South Africa’s competition cases *Referral by Commission cites 2008 as end-date

ArcelorMittal’s approach to Competition Legacy Issues • The long steel market collusion and price fixing investigation relates mostly to activities between 2000 and 2004 but the Commission argued that the practice continued until 2008. We can confirm that these practices have stopped. • The company co-operates with the Competition authorities and will present its case to the regulatory authorities in due course. • Most of the cases relate to legacy issues but there are exceptions • IPP pricing replaced with the basket method in 2006 with greater transparency in pricing policy. The company has changed its formula, communicates price changes regularly and is today far more transparent about the reasons for price adjustments. Engineering News, 25 September 2009

Agenda • Introduction • Competition Commission • Our Cases • Our Pricing • Compliance • Our Vision

ArcelorMittal South Africa Today: Pricing/Market Behaviour • As a business that operates in both South African and international markets our prices are market driven and globally competitive. • In 2006, ArcelorMittal changed its pricing model from import parity pricing to a system benchmarked against a basket of domestic prices from a range of international markets. • Openly publish prices to all customers and other stakeholders, including the volume discounts per product. • All our customers are treated on an equal commercial basis and have access to the same information. • Despite drastic cost cutting initiatives, our current loss-making situation shows that our pricing can flow either way and underlines the adaptability of the basket model, which is vulnerable to market conditions. • Commitment to competitive behaviour and training of executives and sales & marketing staff. • Rigorous internal compliance policies.

Previous Model: Import Parity Pricing • Black Sea price base • Plus logistical costs • Plus import duties • Commission and financing • Plus harbour and stevedore cost • Plus domestic logistical cost • Converted with the exchange rate • The gap with the prevailing price levels is determined • A management decision is then taken with the above information together with the view on international steel price movement

Current Model: Basket/Benchmark Pricing • This model averages out domestic US dollar prices of steel products in two developed (US, Germany) and two developing (China, Russia) nations. • This is translated on a monthly basis via our forecast for the Rand / US $ exchange rate for the months ahead. • New model implemented Q1 2006. • This method produces a realistic basis for supporting development of the steel manufacturing industry in SA. • Central to the development of the infrastructure which underpins the competitiveness of South Africa in the global economy.

ArcelorMittal and the Downstream Manufacturing Industry Value-added export rebate system – funded and administered by SAISI. Where do we want to be as a country – competitive with niche or mass producers? China – difficult to compete on steel prices alone, other input costs are more crucial. But we can add value through quality downstream products. Efficient downstream manufacturing will enable South Africa to become globally competitive. ArcelorMittal SA’s wider economic impact: Employs 9 100 permanent and 2000 temporary staff (at peak production levels). Supports thousands of jobs among sub-contractors and the downstream manufacturing industry. Contribution to GDP: 1.2%. Significant tax payments (2008: R4bn) and forex contribution (R5bn). Trains artisans, technicians and engineers beyond its own requirements to support government’s drive to train scarce skills (Current pipeline of over 3,000 skills) R250m CSI commitment to the construction of public schools over a 7-year period 15

Agenda • Introduction • Competition Commission • Our Cases • Our Pricing • Compliance • Our Vision

ArcelorMittal South Africa operates its business in a manner that is in compliance with applicable competition law.

ArcelorMittal South Africa Today: Legal/Compliance Practices ArcelorMittal has rigorous internal compliance practices in place, driven through documented compliance policies. • Promoting a culture of probity and commitment to the highest standards of ethical and professional conduct which apply to all directors, employees and contractors. • Core values of honesty, integrity and dignity are firmly entrenched in the company’s code of business conduct. • Overarching Compliance Framework provides an overview of the compliance requirements: • Assists with effective implementation of Compliance • Sets out standards developed to highlight key aspects of compliance that must be attended to on an ongoing basis.

ArcelorMittal South Africa Today: Legal/Compliance Practices

Agenda • Introduction • Competition Commission • Our Cases • Our Pricing • Compliance • Our Vision

We firmly believe that a successful business is a responsible business, and long-term growth for shareholders goes hand-in-hand with our wider commitment to our communities, our employees, and the environment. 21

ArcelorMittal of Tomorrow • ArcelorMittal South Africa is firmly committed to ensuring compliance with all relevant laws, regulations and to the highest standards of ethical conduct by constantly striving to improve the company’s governance model. • We do not condone anti-competitive market behaviour • We strive to operate with integrity, reliability and innovation - three core values that drive our business forward. • Responsible behaviour is central to our business and fully supports our strategy for growth. • We promote high ethical standards across the business and provide detailed codes of best practice to all our employees. • ArcelorMittal's success in the steel sector relies on responsible behaviour and good corporate citizenship and maintaining good relationships with all its stakeholders.

Conclusion • ArcelorMittal South Africa does not believe that steel in this country is inappropriately priced. • On the contrary, by benchmarking prices against international norms we fairly reflect global supply and demand conditions. • Our basket pricing model puts paid to the criticism that we are abusing our strong local market position. • Realistic basis to support downstream steel industry with specific focus on export facing fabricators and manufacturers. • We need to move beyond legacy-based perceptions.