Download

1 / 54

540 likes | 683 Views

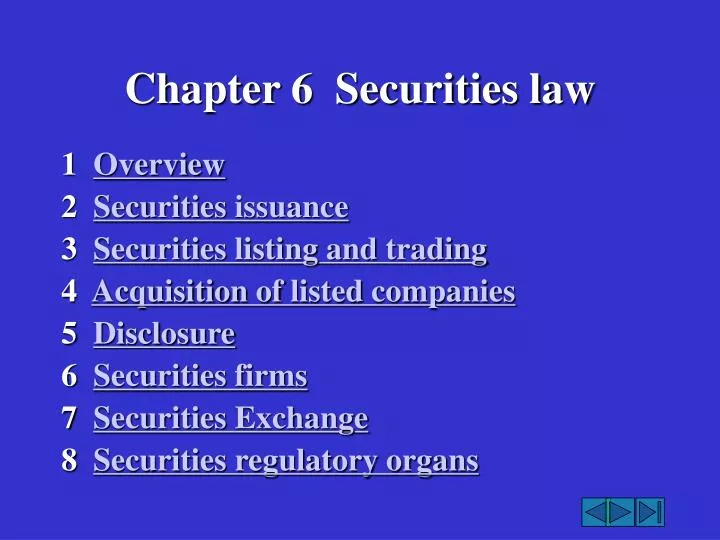

Chapter 6 Securities law . 1 Overview 2 Securities issuance 3 Securities listing and trading 4 Acquisition of listed companies 5 Disclosure 6 Securities firms 7 Securities Exchange 8 Securities regulatory organs . 1 Overview . 1.1 Concept of securities .

E N D

Chapter 6 Securities law 1 Overview 2 Securities issuance 3 Securities listing and trading 4 Acquisition of listed companies 5 Disclosure 6 Securities firms 7 Securities Exchange 8 Securities regulatory organs

1 Overview 1.1 Concept of securities • Negotiable instrument: means of payment • Securities: means of investment • represent property rights contained in them • directly indicate the magnitude of the rights • Stocks and corporate bonds are the primary means of • investment

1.2 Sources of securities law • Stock Regs., 1993 • Company Law, 1993 • Securities Law, 1999 • 250 pieces of securities-related laws, administrative regulations and ministerial rules

2.1 Classification 2.1.1 Stocks 2.1.1.1 State, legal person and individual shares 2.1.1.2 Registered and bearer shares 2.1.1.3 Common and preferred shares 2.1.2 Corporate bonds 2.1.2.1 Registered and bearer bonds 2.1.2.2 Guaranteed and non-guaranteed bonds 2.1.2.3 short, mid and long term bonds 2.1.2.4 Convertible and non-convertible bonds

2.2 Conditions for stock issuance Conditions and procedures of securities issuance

2.2.1 IPO • 6 conditions: (1) production and operation conformity with State industrial policies (2) only one type of common stock is issued with equal rights for equal shares (3) promoters: no less than 35% of the total shares (4) promoter’s shares: no less than RMB 30 million in terms of absolute number (5) general public shares: no less than 25%, proportion for workers and staff no more than 10% of the amount to be issued to the public. If total issuance more that RMB 400 million, the CSRC may reduce such proportion, but not below 10% bottom line (6) promoters: not major violation of the law within previous 3 years • Additional requirements for converting into CLS: • net assets: at least 30% of total assets, intangible assets not more than • 20% • (2) having made profits for 3 consecutive years prior to stock issuance

2.2.2 Re-issuance (1) former issuance has been fully subscribed for (2) interval since the former issue at least 12 months (3) profitable consecutively for the recent three years, able to pay dividends to its shareholders (4) financial and accounting documents: no misrepresentation for the recent three years (5) projected profit rate reaches the interest rate of bank deposits for the like period. Corporate resolutions on re-issuance: (1) classes and number of the new shares (2) issuing price (3) commencing and ending dates of issuance (4) classes and number of new shares issued to the existing shareholders

2.3 Conditions for bonds issuance • CLS’s net assets no less than RMB 30 million, LLC’s no less than RMB 60 million • (2) cumulative value of company bonds not exceed 40% of corporate net assets • (3) average distributable profit for the recent three years sufficient to pay one year's interest on the company bonds • (4) investment consistent with State industrial policy • (5) interest rate not exceed level of interest rate set by the State Council • (6) other requirements prescribed by the State Council. 2.3.1 Initial issuance 2.3.2 Re-issuance Conditions for initial issuance + 2 additional conditions: (1) bonds previously issued have been fully subscribed for (2) company not in default of any of previously issued bonds or company debt or late in payment of principal and interest has occurred

Illustration:CSRC sued by Hainan Kaili Company In June 1998 Hainan Kaili Company submitted all the materials for listing A-shares to CSRC. No response was made by CSRC in the subsequent period till 1999 when CSRC submitted a report to leaders of the State Council claiming Kaili Company was suspected of 97% fake profits. As a result CSRC decided to cancel Kaili Company’s A-shares listing qualification. Almost two years later in April 2000 the CSRC returned those materials to Kaili Company. In July 2000 Kaili Company took CSRC to the court. The trial court held that CSRC’s administrative acts were severely defective since CSRC is only empowered to decide whether to approve the listing application. The return of the materials after long delay without saying yes or no did not conform to such requirements. On 18 December 2000 the trail court ordered that CSRC should resume the procedure of reviewing Kaili Company’s listing application and give a definite answer regarding the listing matter within 60 days. CSRC appealed the decision and the appellate court upheld the trial court’s decision on 5 July 2001. That means even powerful government departments have to abide by correct administrative procedures.

2.4 Procedures for issuing securities • 3 months waiting period • If rejected, CSRC and department authorized by the State Council must explain the reasons 2.4.1 Verification or approval

2.4.2 Issuance disclosure • Public offer documents prior to public issuing • Make prospectus available to public and prepare share subscription form Prospectus: (1) number of shares subscribed for by promoters; (2) par value and issuing price of each share; (3) total number of bearer share issued; (4) rights and obligations of subscribers; (5) commencement and expiration time of the share offer, and statement that in the event the shares have not be subscribed in full upon the expiration time, the subscribers may revoke their share subscriptions

Prospectus of bond issuance: (1) issuer’s name (2) total value of bonds and par value of each bond (3) rate of interest on the bonds (4) time limit and method for payment of the principal of and interest on the bonds (5) commencement and ending date of bonds issue (6) corporate net assets value (7) total value of issued and outstanding company bonds (8) underwriter Issuers, promoters or directors must ensure that information so disclosed is authentic, accurate and complete, and does not contain any false, misleading statements or major omissions

2.4.3 Issuing price • Same conditions, same price • At par value, or above par value, but may not • below par value

2.4.4 Securities underwriting • Issuer choose their own securities firms as underwriter • Proxy or exclusive underwriting • Public offer amounting to RMB 50 million: underwriting • syndicate Underwriting agreement: (1) names and domiciles of parties and names of their legal representatives (2) type, quantity, amount and issuing price of securities to be underwritten (3) period, maximum 90 days (4) means and date of payment of proceeds from sale (5) the fees for sale on proxy or exclusive underwriting basis and the means of settlement (6) liability for breach of contract (7) other matters prescribed by the CSRC.

2.4.5 Issuance • Upon full subscription, share capital must be verified by capital verification institution • Issuer shall formally deliver stocks to shareholders • Stocks issued to promoters, State-authorized investors and legal persons must be registered in the name of holder. • Bond issuance: immediate delivery of the bonds • Counterfoil:

3 Securities listing and trading 3.1 Overview 3.2 Listing, and suspension and termination of listing

3.2.1 Listing conditions (1) shares have been issued to the public (2) minimal total share capital RMB 50 million (3) minimum operation period: 3 years, and profitable consecutively (4) minimum 1000 shareholders each holding shares no less than RMB 1000, and shares issued to public amount to at least 25%; if total share capital exceeds RMB 400 million, then at least 15% (5) no material illegal act for the recent three consecutive years, and no misrepresentation in financial and accounting reports (6) other requirements prescribed by the State Council 3.2.1.1 Stock listing conditions

3.2.1.2 Bonds listing requirements (1) term: no less than 1 year (2) actual amount no less than RMB 50 million (3) still meets issuance conditions at the time of listing 3.2.2 Suspension of listing 3.2.2.1 Suspension of stock listing • total share capital or the composition of equity ownership • has changed so that it no longer meets requirements for listing • (2) fails to make public its financial condition, or has made misrepresentations • (3) has engaged in material illegal act • (4) has been suffering losses for the recent three consecutive years

3.2.2.2 Suspension of bond listing (1) major illegal act (2) no longer meets bond listing conditions due to major change in it (3) proceeds are not used for purposes approved by the approval authority (4) fails to perform its obligations stipulated in the measures for offer of corporate bonds (5) operate at a loss over the past two years 3.2.3 Termination of listing

3.3 Prohibited conducts Liability for guilty of prohibited conducts

3.3.1 Insider trading Insider trading activities: • insiders use inside information in trading securities or • provide advice to other persons to trade • (2) insiders selectively reveal inside information to others who use it to trade • (3) non-insiders obtain inside information by illegal means to trade securities or provide advice to others who trade securities

3.3.1.1 Scope of insiders (1) issuer’s directors, supervisors, manager, deputy managers and other officers (2) shareholders holding more than 5% of the shares (3) senior officers in the holding company of issuer (4) persons capable of obtaining company information concerning trading its securities by virtue of the positions holding in the company (5) staff members of CSRC, and other persons administering securities trading (6) relevant staff members of public intermediary organizations participating in securities trading and relevant staff members of securities registration and clearing institutions and securities trading service organizations (7) other persons specified by the CSRC

3.3.1.2 Scope of inside Information (1) major change in corporate business guidelines or scope of business (2) decision made by company concerning major investment or major asset purchase (3) conclusion by company of major contract which may have important effect on the corporate assets, liabilities, rights, interests or business results (4) incurrence by company of major debt or default on overdue major debt (5) incurrence by company of major deficit or incurrence of major loss exceeding 10% of corporate net assets (6) major change in external conditions of corporate production or business (7) change in BOD chairman , more than 1/3 directors or manager of company (8) considerable change in holdings of shareholders holding more than 5% of the corporate shares

(9) decision made by company to reduce capital, merge, divide, dissolve, or apply for bankruptcy (10) major litigation involving company, or cancellation of resolution adopted by AGM or BOD by the court (11) corporate plans on distribution of dividends or increase of capital (12) major changes in corporate equity structure (13) major changes in security for corporate debts (14) any single mortgage, sale or write-off of major asset used in the business of the company exceeding 30 percent of such asset (15) potential liability for major losses to be assumed in accordance with law as a result of the act committed by directors, supervisors, manager, deputy managers or other officers (16) plans on the takeover of listed companies (17) other important information determined by CSRC to have marked effect on trading prices of securities

3.3.2 Manipulation (1) independently or in collusion with others carrying out combined or successive purchases or sales by building up an advantage in terms of funds or shareholdings or using one's advantage in terms of information, thereby manipulating the trading prices of securities (2) collaborating with another person to mutually trade securities or to mutually buy or sell securities not held by them at the prearranged time and price and by prearranged means, thereby affecting the price or volume of the securities traded (3) buying or selling securities from or to oneself without transfer of ownership of the securities by means of making oneself the other party to the transaction, thereby affecting the price or volume of the securities traded (4) manipulating trading prices of securities by other means

Illustration: Yi’an Technology’s stock price manipulation punished Yi'an Technology was formerly known as Shenzhen Jinxing, which was listed on the Shenzhen Stock Exchange in May 1992. Its former housing developer was acquired by the Guangdong Yi'an Technology Holding Company in April 1999 and changed to its current name four months later. In late 1999 and early 2000 the stock attracted wide attention from investors. Its price soared 486 percent from RMB 26.01 on 25 October 1999 to RMB 126.31 on 17 February 2000. The stock became the first stock in the market that broke the psychological threshold of RMB 100, and set a record of increasing nearly five times its value in 70 trading days. There was obvious speculation on the shares. After full investigation into the case, the CSRC confirmed that it was a typical stock manipulation case. The four companies through illegal activities, such as setting up 627 bogus individual accounts and using them to buy shares, accumulating 85 percent of the circulating shares in the company in a little over a year. Shares were sold back and forth among the various accounts, steadily ratcheting up the price and generating buzz. They brought the prices of Yi'an Technology up to the peak of RMB 126.3 from around RMB 20 at initial public offering. In February 2000, Yi’an Technology became the first stock China to sell for over RMB 100 per share, notwithstanding the fact that it was actually a poultry feed producer with a grab bag of half-baked “new economy” high-tech schemes. The stock then nose-dived after CSRC announced to investigate them. In April 2001 the CSRC punished four institutional investors for stock price manipulation, and imposed a fine and confiscation of illegal incomes totaling RMB 898 million, the highest punishment in China’s securities market history.

Illustration: Zhongke Chuangye’s stock price manipulation Zhongke Chuangye is the only one in which the manipulator confessed an inside story. It triggered big shocks in the stock market when the market witnessed its stock price fall to the flooring limit (10%) five days straight It is also the first stock price manipulation case in the Chinese stock market under criminal proceedings. The present trial in Beijing court is aimed at the five operating persons including Ding Fugen under Lu Liang. The issue was about the manipulation of 53 percent of the outstanding stocks by Ding Fugen only. So far the whereabouts of chief commander, Lu Liang was unknown. In February 2001 Caijing reporter revealed that Lu Liang went down to Shenzhen to start playing the securities market. After a few market turns, he built a reputation among market insiders. By 1996 Lu Liang had created a career writing about markets, doing consulting work, and advising investment funds. He also fell in with a Shenzhen speculator named Zhu Huanliang who was scheming to gain control of a company called Kangda’er.

Lu Liang went back to Beijing, raised over RMB 700 million from various Beijing companies and organizations, bought a large portion of the non-circulating government shares of Kangda’er, and took control of the company. In the spring of 1999, Lu Liang published the first of four articles in Securities Market Weekly under the pseudonym Mr. K. He writes that in biotech and high-tech agriculture, Chinese can take on any foreigner and go global, so the opportunity for investors is now. In the fourth of his series he let drop that an overlooked little company called Kangda’er was well positioned to take advantage of this new wave. In August 1999, he placed an unsigned article in China Securities Daily describing how Kangda’er was reorganizing and would become a holding company with investments in biotech, high-tech agriculture, and Internet services and equipment. He then changed the name of the company to Zhongke Chuangye and bought stakes in Chinese medicine companies, but the company still had almost no assets. With the favorable self-generated publicity, and after orchestrating a series of phony stock deals at steadily increasing prices, and utilizing about 1500 shares accounts in about 120 branches of the securities companies throughout China, he was able to generate a sense of momentum that led to 26 straight months of appreciation, making a profit up to RMB 1000 million. Eventually the scheme collapsed due to Zhu Huanliang’s betrayal, who sold out early. He was left holding the bag.

3.3.3 Securities firms cheating their clients (1) purchasing or selling securities on behalf of the client contrary to its instructions (2) failing to provide the client with written confirmation of the transaction within the prescribed period of time (3) misappropriating the securities entrusted by the client for purchase or sale or the funds in the client's account (4) purchasing or selling securities in the client's account without the client's authorization, or purchasing or selling securities under the name of the client (5) inveigling the client into making unnecessary purchase or sale of securities in order to obtain the commission (6) any other act contrary to the client's authentic demonstration of intention and detrimental to the client's interests

3.3.4 False representation (1) issuers, securities firms making false statements in the prospectus, listing announcement, company reports and other relevant documents (2) professional securities service organizations such as law firms, accounting firms, asset appraisal firms making false statements in the opinions, reports and other relevant documents (3) Securities Exchanges, securities trade association or other self-disciplinary securities trade organizations making false statement having a major impact on the securities markets (4) issuers, securities firms, professional securities service organizations and self-disciplinary securities trade organizations making false statements in various documents, reports and instructions submitted to the CSRC (5) other false statements regarding the securities issuance, trading and relevant activities

Illustration: Yinguangxia financial fraud The CSRC confirmed that Yinguangxia fabricated a huge sum of RMB 745 million of profit by way of counterfeiting purchasing and selling contracts, exportation declaration statements, value added tax invoices, duty-free documents, financial notes and business revenue fabrication. In 1999, it boasted RMB 178 million of profit and RMB 567 million in 2000. Zhongtianqin, a Shenzhen-based accounting firm, was found to have helped Yinguangxia fabricate profit reports to win a top performer position. Zhongtianqin has since been rebuked by the MOF. More than 60 listed company clients of Zhongtianqin, which was previously the largest and most renowned accounting firm in China have had their reputations damaged because of the fraudulent actions related to Yingguangxia. Yinguangxia appeared to be one of the best stock in recent years. At the date of flotation 12 December 1999, the price was only RMB 13.97. One year later on 29 December 2000, the price rose to RMB 37.99, or 75.98 per share due to the habit of splitting one share in half. It rose over 440% and was the 2nd best performing stock.

The profit per share increased to RMB 0.827 after splitting the shares in half. The reason why so many investors are eager to buy is its well-arranged annual reports and notices. It spent two (2) years making a trap for its minority shareholders. In 2001 the boasts became ridiculous. Its fabrications were unveiled on 2 August by the Business & Finance Review. After its suspension for 1 month, it broke the record of China’s securities market by undergoing a consecutive 15-day drop from RMB 30.79 to 6.35 per share. Its minority shareholders suffered enormous losses as a result. This is not an individual phenomenon. The Zhengbaiwen (600898), ST Zhongke (0048), Yi’an Technology (0008), Lantian (600709) and some others have their own stories. The announcement on the accounting information quality sample survey published by the MOF shows 155 of the 157 enterprises surveyed had the problem of false reporting on their profits. It is clear how serious the case of false figures and information is. These cheating and fabrications greatly hurt shareholder’s confidence and contributed to the historic downward turmoil in China’s stock market dropping from 2245.43 to 1607.08 points from 14 June to 24 December 2001, a decrease of 30%.

Illustration: Securities analyst liable for misrepresentation On March 1997 Zhang Quanjia read an article entitled Xiang Zhongyao with great potential written by securities analyst Xiong Jingsong published on a newspaper. The paper claimed that Mr. Xiong called the company and was advised that its performance would increase 100% that year with a net profit of RMB 35 million. The net earning per share would reach RMB 0.5 and the total corporate assets would amount to RMB 800 million. Its products have obtained the FDA authentication. Zhang Quanjia was profoundly attracted by such analysis and decided to buy such shares. Within just one month Zhang Quanjia spent RMB 343590.37 and bought 27500 shares in sixteen times. Soon after Zhang’s purchase the company announced its annual report, which disappointed Zhang dramatically. There was huge gap between the actual result and Xiong’s forecast. In reality the net profit is merely RMB 15.6 million with an earning of RMB 0.217 per share. The corporate products did not pass FDA authentication either. Zhang suffered a total loss of RMB 79577.66. Dissatisfied with such securities analysis Zhang sued Mr. Xiong and the newspaper in 1999. In June 2001 the trial court awarded Zhang RMB 84836.1 as compensation. On 7 December 2001 such judgment was enforced by court and Zhang obtained the total sum of damages suffered from irresponsible securities analysis.

4 Acquisition of listed companies 4.1 Overview 4.2 Acquisition by tender offer

Trigger: holding 30% of issued shares + plans to continue acquiring the target company’s shares • Submission of offer to CSRC: • (1) name and domicile of purchaser • (2) takeover decision of the purchaser • (3) name of listed company to be acquired • (4) purpose of takeover • (5) detailed description of shares to be bought up and number of • shares scheduled to buy up • (6) term and price of takeover • (7) amount and guaranteed availability of the funds required for • such takeover • (8) proportion of shares held by the offeror at the time the takeover • report is submitted • Simultaneous submission to the Securities Exchange

Public announcement: 15 days after submission • Length of takeover: 30 to 60 days • If acquire more than 75%, termination of listing of shares of target company • If acquire more than 90%, remaining holders may sell their shares on the same terms as those in the takeover offer, and offeror must buy up the same 4.3 Acquisition by agreement

5 Disclosure Requirement for different ways of disclosure

5.1 Overview On 27 March 2001, 12 firms were disciplined for failing to register the deals with the watchdog or disclose the opinions of the intermediate organizations on the deals, as required by relevant rules. On 27 July 2001 the CSRC publicized the decision to issue a public criticism to five firms and their functionaries for irregularities in substantial purchases and sales of assets. The five firms are: Yibin Wuliangye Co., Ltd, Shanghai Material Group Import and Export Co.,Ltd, Xiongzhen Group Co., Ltd, ST Xiamen Marine Co., Ltd, and Shanghai Hongsheng Technology Co., Ltd. The chairmen of their BOD and BOD secretaries were also criticized and asked to take responsibility. Illustration: Five listed companies criticized by CSRC

5.2 Mid-term and annual report • corporate financial and accounting reports and business • situation • (2) major litigation involving the company • (3) particulars of any changes in the shares or corporate bonds issued • (4) any important matters submitted to the shareholder’s' meeting for consideration • (5) other matters specified by the CSRC 5.2.1 Mid-term report

5.2.2 Annual report (1) brief account of the corporate general situation (2) corporate financial and accounting reports and business situation (3) brief introduction to the directors, supervisors, managers and the officers and information with respect to their shareholdings (4) details of shares and corporate bonds issued, including the name list of 10 biggest shareholders and number of shares held by them (5) other matters specified by the CSRC

5.3 Material events report (1) major change in the corporate business guidelines or scope of business (2) decision made by the company concerning major investment or major asset purchase (3) conclusion by the company of major contract which may have important effect on the corporate assets, liabilities, rights, interests or business results (4) incurrence by the company of major debt or default on the overdue major debt (5) incurrence by the company of major deficit or incurrence of major loss exceeding 10% of the corporate net assets (6) major change in the external conditions of the corporate production or business (7) change in BOD chairman, more than 1/3 directors or manager of the company (8) considerable change in the holdings of shareholders holding more than 5% of the corporate shares (9) decision made by the company to reduce capital, merge, divide, dissolve, or apply for bankruptcy (10) major litigation involving the company, or cancellation of the resolution adopted by AGM or BOD by the court (11) other events specified in laws or administrative regulations

5.4 Acquisition disclosure Acquisition by tender offer and by agreement is subject to disclosure 5.5 Disclosure of big shareholding changes

6.1 Creation and scope of business • Comprehensive securities companies: • LLC or CLS • Subject to the approval by CSRC (1) minimum registered capital of RMB 500 million (2) chief administrators and business persons are qualified to engage in securities business (3) fixed place of business and up-to-standard trading facilities (4) sound management system and standardized system for the separate administration of business on its own account and brokerage business • Securities brokerage companies: (1) registered capital of RMB 50 million (2) chief administrators and business persons are qualified to engage in securities business (3) fixed place of business and up-to-standard trading facilities (4) sound management system.

6.2 Special qualifications Directors, supervisors and manager: Company Law Additional negative requirements: • responsible persons of Securities Exchanges or securities • registration and clearing institutions and directors, supervisors and managers of securities companies removed from office due to violation of the law or rules of discipline within 5 years after such removal • (2) lawyers, certified public accountants, and professionals of statutory asset appraisal organizations or verification organizations disqualified as such due to violation of the law or rules of discipline within five (5) years after such disqualification

6.3 Regulations on business activities • separate their brokerage business from trades for their own account • separate relevant business personnel and financial accounts from each other Comprehensive securities companies: Handling brokerage business: separate securities account and funds account for its client