Download

1 / 38

380 likes | 412 Views

A State Contingent Claim Approach To Asset Valuation. Kate Barraclough. Overview. Aim is to empirically test the application of Arrow-Debreu state preference theory State preference approach is applied to pricing both to stocks and options

E N D

A State Contingent Claim Approach To Asset Valuation Kate Barraclough

Overview • Aim is to empirically test the application of Arrow-Debreu state preference theory • State preference approach is applied to pricing both to stocks and options • Model values under state pricing are compared to other asset pricing models • State preference approach is found to provide an overall improvement on the other models for both stocks and options

Background • Basic form of any asset pricing equation: where Pt is the price at time t, Et is a conditional expectations operator, Xt+1 is the asset’s payoff and Mt+1 is the stochastic discount factor • The stochastic discount factor represents investors’ marginal rates of substitution between consumption in the current period, and consumption in time t, state s.

State Contingent Claims • Stochastic discount factor may be characterised by the set of state contingent claim prices • A state contingent claim will have a positive payoff in state s and zero elsewhere • Ross (1976) - state contingent claims will be implicit in the price of traded securities and in a complete market investors may form a portfolio with a positive payoff in state s and zero elsewhere

State Preference Approach • State price is the price today of one unit of consumption at time t, state s • The price of a risky asset may be determined as the payoff in time t state s multiplied by the state price and summed over all possible S states:

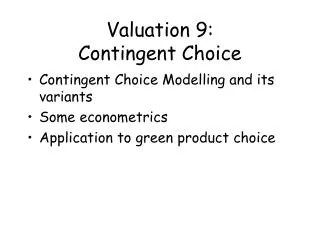

Breeden and Litzenberger (1978) – state contingent claim may be modelled as the second derivative of a call option price Construct a butterfly spread with a unit payoff – buy one call with strike M-ΔM, one call with strike M+ΔM, and sell two calls with strike M State Price Computation ΔM M-ΔM M M+ΔM

State Price Computation • If the value of the underlying asset is M next period, then the payoff on the option portfolio will be ΔM and zero otherwise. • Normalising for a unit payoff: • Taking the limit as ΔM tends to zero then the price of a portfolio paying one unit will be given by: • Evaluating the portfolio at X=M provides

State Price Computation • Black-Scholes option pricing formula provides a closed form solution: where • But cannot compute in continuous increments for each strike

Delta Securities • Delta security – unit payoff if the price of the underlying asset is greater than or equal to some level Y: • State price - cost of a security with a unit payoff if the level of the underlying asset is between some levels is between some levels Y1and Y2:

Advantages • Incorporate market microstructure features • Minimum tick size in the underlying instrument • Price limits, circuit breakers etc • Limit range of distribution with empirical maximum and minimum returns • Not price extreme observations • Reduce computational burden

S&P 500 Index Options • First test of the paper is to apply the state preference approach to pricing S&P 500 index options • Compare model values to the Black-Scholes option pricing formula and Stutzer’s canonical valuation approach

State Preference Approach • Historical maximum and minimum T-day returns are determined from the empirical distribution of returns on the S&P 500 index • Possible future index levels are calculated in increments of 5c • The state price corresponding to each index level are determined by the delta security method

State Preference Approach • The option price is calculated as the sum of the expected payoff at each index level multiplied by the respective state price • Call option prices will be given by: • And put options:

Canonical Valuation • Stutzer (1996) – determine risk-neutral probabilities from the empirical distribution of returns on the underlying instrument • Solving the unconstrained minimisation problem: provides the probability distribution:

Canonical Valuation • Option prices are determined with reference to historical index returns • Calculated as the sum of the expected payoff at each index level multiplied by the respective risk-neutral probability:

Options Data • S&P 500 index options • Weekly observations January 1990 through December 1993 • Two proxies for expected stock market volatility: • CBOE Market Volatility Index (VIX) • 40 day historical volatility • Daily observations on the S&P 500 index used to determine historical distribution of index returns

Stock Valuation • The second test is to apply the state preference approach to stock valuation • Comparison is made between the state preference approach and Ohlson’s (1995) residual income model • Stutzer’s canonical valuation approach is also applied

State Preference Approach • Linear projection to determine stock movements in reference to the market: • Payoffs are given by: • Providing the valuation expression:

Canonical Valuation • Determine risk-neutral probabilities from the historical distribution of index returns as described previously • Apply to the payoff function from the previous slide to provide the valuation expression:

Residual Income Model • The residual income model specifies a relationship between market value, book value, and contemporaneous and future earnings • Based on the dividend discount model: • And a clean surplus relation:

Residual Income Model • Combining the dividend discount model and the clean surplus relation: • Test empirically using cross sectional regression estimates:

Stock Data • Sample covers all companies in the COMPUSTAT database from 1993 through 2004 • Linear projection – based on monthly observations over the previous 5 years • Stock and index returns are from the CRSP database • Consensus earnings from I/B/E/S proxy for the market’s expectation of future earnings

Summary • S&P 500 index options: • state preference approach provides an overall improvement compared to Black-Scholes and canonical valuation • Stocks • state preference approach provides a significant improvement on the residual income model for stock valuation

Future Directions • Extend canonical valuation approach • Additional constraint of previous day’s call option price – similarity to using previous day’s implied volatilities for Black-Scholes • Include market microstructure considerations - 5c/10c price increments rather than empirical movement • Implications for investor risk preferences • VIX index vs realised volatility

Future Directions • Compare results for stock valuation over different maturities • 1 week • 1 month • Quarterly • May be improvements available for residual income model