Download

1 / 28

280 likes | 350 Views

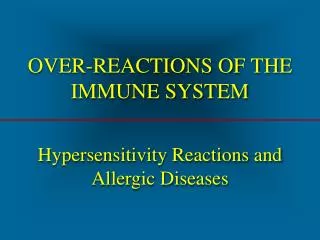

Reactions to the Sub-Prime Turmoil Carlos Hamilton V. Araújo IADB, May 2008. I. Asset Prices II. Banking System III. Macroeconomic Developments IV. Conclusion. Outline. Asset Prices. US Dollar Spike. 108. 98. Jun 14 2007=100. 88. 78. Jun. Jul. Aug. Sep. Oct. Nov. Dec. Jan.

E N D

Reactions to the Sub-Prime Turmoil Carlos Hamilton V. Araújo IADB, May 2008

I. Asset Prices II. Banking System III. Macroeconomic Developments IV. Conclusion Outline

US Dollar Spike 108 98 Jun 14 2007=100 88 78 Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar 07 07 07 07 07 07 07 08 08 08 USD/BRL USD/CNY USD/JPY USD/EUR Source: Bloomberg

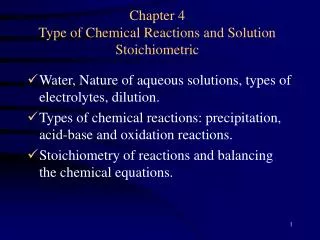

1.5 310 1.0 280 0.5 250 0.0 220 -0.5 190 -1.0 160 -1.5 -2.0 130 Jun 07 Jul 07 Ago 07 Sep 07 Oct 07 Nov 07 Dec 07 Jan 08 Feb 08 Mar 08 Apr 08 May 08 Sovereign Spread and Risk Aversion Index Embi+Br basis points Risk Aversion Index Sources: JP Morgan Chase and Merrill Lynch

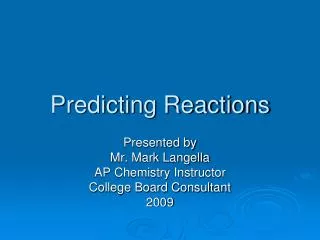

125 115 105 95 85 75 Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar 07 07 07 07 07 07 07 08 08 08 Ibovespa x Latin American Stock Exchanges Jun 14 2007=100 Ibovespa Mexbol Merval IPSA IBVC Source: Bloomberg

Other Comments • Almost all IPOs, even those that had already been announced, were postponed • The cost of the international financing became prohibitive, even in case of well ranked corporations • There are reasons to believe that “this time is different”

Some Previous Developments • Mainly in the second half of the 90s, the Brazilian banking system passed through a huge clean-up process • In the last couple of years, the Congress approved some laws enhancing the protection of the creditors • The above improvements contributed decisively to strengthen the prospect for the system

Expansion of the Credit * Registered at the Central Bank Credit Information System

Trade Balance 12-month accumulated 175 165.6 165 155 145 12-month surplus: US$36.4 bi 135 125 129.2 115 US$ billion exports 105 95 85 75 65 imports 55 45 Jan Jan Jan Jan Jan Jan Jan Jan Jan Feb 99 00 01 02 03 04 05 06 07 08

Net FDI 45 FDI 35 25 15 US$ billion 5 -5 -15 Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Jan Jul Feb 99 99 00 00 01 01 02 02 03 03 04 04 05 05 06 06 07 07 08

International Reserves Mar 25: US$194.3 bi 200 180 160 140 120 Apr 03: 15.9 US$ billion 100 80 60 40 20 end-of-2004: 27.5 0 Jan Jan Jan Jan Jan Jan Jan Jan Jan Mar 99 00 01 02 03 04 05 06 07 08

Net External Debt 175 150 1Q03: 165.2 125 4Q04: 135.7 100 75 US$ billion 50 25 0 4Q07: -10.8 -25 1Q 3Q 1Q 3Q 1Q 3Q 1Q 3Q 1Q 3Q 1Q 4Q 02 02 03 03 04 04 05 05 06 06 07 07

External Sustainability Indicators net external debt/exports net external debt/GDP de 3.1 para -0.1* de 32.7 para –1.4%* 3.5 35 3.0 30 2.5 25 2.0 20 1.5 15 % 1.0 10 0.5 5 0.0 0 -5 -0.5 00 01 02 03 04 05 06 07 08 00 01 02 03 04 05 06 07 08 (Feb) (Feb) * Record low since the start of the series in 1970; 2008 – estimates.

Interest Payments/Exports Ratio from 35.6% to 9.5%* 38 34 30 26 % 22 18 14 10 6 1999 2000 2001 2002 2003 2004 2005 2006 2007 * Record low since the start of the series in 1970.

IPCA Expectations and Target 15 12-month IPCA expectations 12 9 % p.a. upper limit 6 central target 3 lower limit 0 Jan Jan Jan Jan Jan Jan Jan Jan Dec 02 03 04 05 06 07 08 09 09

Inflation Convergence to Targets IPCA (12-month trailing basis ) 18 market consensus 15 12 Feb 08: 4.61% 2008: 4.44%* 9 % % 6 3 0 Jan Jan Jan Jan Jan Jan Jan 03 04 05 06 07 08 09 *March 20

Consolidated Public Sector Primary Surplus 7 6 avg. 1994-Jun/95 4.77% Jan 08 4.15% avg. 2003-2007 4.13% 5 4 3 % of GDP avg. 1999-2002 2.91% 2 avg. Jul/95-1998 -0.08% 1 0 -1 -2 Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan Jan 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Debt/GDP 57 56.0 55 1Q 02 – 2Q 07 (quarterly data) market expectations (annual data) 53 51 49 4Q 07 42.8 47 % of GDP 45 43 41 39 37 35.1 35 1Q 02 1Q 03 1Q 04 1Q 05 1Q 06 1Q 07 2008 2012 Source: BCB

Accumulated Reduction in FX-Linked Domestic Debt as of Jan 2003 90 80.9 80 70 60 50 40 US$ billlion 30 20 10 0 -10 Jan Jul Jan Jul Jan Jul Jan Jul Jan Jan Jul 03 03 04 04 05 05 06 06 07 08 07

Asset Prices Similarly to what was seen in the last two decades or so, the Brazilian assets depreciated in response to the break out of the sub-prime financial turmoil However, differently from the old pattern, the depreciation was relatively modest and they fastly recovered and on balance have not been hardly affected so far Banking Sector The Brazilian bank sector was healthy enough to overcome the problems caused by the international liquidity crunch without sacrificing the recent cicle of credit expansion Macroeconomic Developments Afer almost a decade of Inflation Targetting, flotation and generation of primary surplus (privatisation, bank reform), “this time is different” From my perspective, since there has been a strong enhancement in the fundamentals, this is largely the best explanation for the fact that so far Brazil has not suffered a lot as a consequence of the sub-prime crisis Conclusion