Download

1 / 38

400 likes | 558 Views

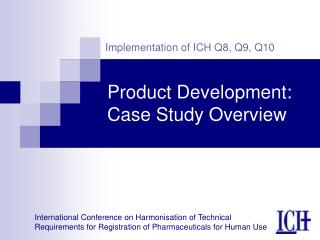

PPP case study: Anyang & Buchon plants, South Korea. Raymond Bourdeaux The World Bank St. Petersburg – May 22, 2008. The Assets: a very complex set up. Electricity. Hot Tap Water Heating. Heat. Combined Heat & Power Plant. Heat Accumulator. Heat. Heat Exchanger. Heat Only Boiler.

E N D

PPP case study: Anyang & Buchon plants, South Korea Raymond Bourdeaux The World Bank St. Petersburg – May 22, 2008

The Assets: a very complex set up Electricity Hot Tap Water Heating Heat Combined Heat & Power Plant Heat Accumulator Heat Heat Exchanger Heat Only Boiler Heat Pipe Consumer Heat Exchanger Heat Incinerator

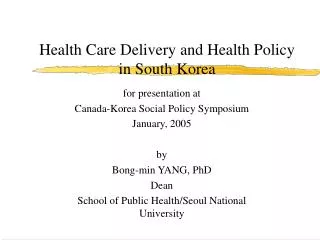

% of DH customer in Korea Capacity generation in Korea Anyang and 98% Anyang and 80% Buchon Buchon Other Other DH generating customers capacity 20% 2% The Assets (cont’d) Huge market potential for privatisation

Mandate and Rationale • December ‘98: Government launches transaction advisors search • Appointed in February ‘99 by Kepco & KDHC to: • undertake 100% sale (assets sales) of : • 2 gas fired power stations (2 * 450MW) producing electricity and heat (combined heat & power “CHP”) in 2 different locations, Anyang & Buchon • 2 district heating (“DH”) networks (about 130 000 households services each) adjacent to CHPs • Rationale • IMF pressure for privatisation and raising cash • KDHC privatisation plan • “logical” fit of CHP & DH systems • “teaser” for Kepco privatisation • get rid of “difficult assets” prior to privatisation • Internal agreed strategy with Client : let’s do it , price is not the top consideration, as this will be a difficult sale

First the good news.. • Not a mammoth transaction: early price range between 400m and 1bn USD • Relatively well managed (no need to significantly reduce work force) • Relatively (new) existing assets, no requirement for significant extension and/or refurbishment • Requirement to raise acquisition finance, not project finance

Specific business characteristics of Anyang and Buchon • “Captive customer basis and long lead time gives good visibility for Heat demand projections. • The obligation to produce heat implies an obligation to produce electricity regardless of the economic rationale to produce electricity (must run status). • As a result the plants are likely to require minimum electricity offtake at certain time equivalent to minimum 40-50% plant load factor .

Strategic Considerations: Commercial District Heating Issues • District heating business is regulated • current price facilitate expansion but is based on “cheap” heat • local monopoly for existing network, but market risk for expansion • limited ability to push fuel price risk to end user • price regulation to be changed but unclear how Electricity Issues • Kepco is quasi monopoly: no market now • move toward pool market at a later (unknown) date means Long Term Power Purchase Agreement not acceptable • “Total fuel pass through to Kepco” would not be fair • merit order position is not straight forward for a “must run” generator • liberalisation of Liquefied Natural Gas market is unclear

Electricty vs heat demand 400 30000 350 25000 300 20000 250 Gcal/hr MWh 200 15000 150 December Heat 10000 100 August Heat 5000 50 December Electricity 0 0 1 3 7 5 9 11 13 15 17 19 21 23 hours The Challenges • Contractual structure: • must run? • fuel pass through? • PPA vs pool?

Strategic considerations; objectives? • Allow operational flexibility and controlling must run states • Managing unions and employee position and achieving transfer to private sector at good price • Maximise value and minimise scope for change in contracts • Foreign investment vs. no foreign exchange rate protection • Minimise future KEPCO liabilities and maximise value

Strategic Considerations: Process • 1 or 2 Sales? • Separate sales of DH and CHP would not maximise speed of transaction • negotiate steam purchase agreement (conflict) • investors with DH experience have electricity experience • Separate sales of DH & CHP in 2 separate geographical entities would not maximise value: • 900 MW is acceptable to investors • 2 sales means 2 parallel bidding processes

The Challenges (cont’d) • Estimate future cash flows? • Presenting reasonable picture of future operating regime • Price evolution for district heating in a new regulatory framework • Future district heating expansion in a “non integrated environment” • PPA for set period vs. indefinite obligation to supply heat • Financial modelling refines price between 400 and 600m USD (allowing foreign exchange protection estimated to be worth between 50-70m USD)

ANYANG/BUCHON LIKELY CASH FLOWS Liberalisation fuel imports bln Won 400 Pool start SALE ? 300 Cash flow 200 Fuel Costs 100 O&M costs 0 - 2000 2010 2005 2015 2020 year FSA PPA -100 -200 2. Requirement for a successful sale: predictable cash flows

Strategic Considerations: Process (con’t) • Contractual strategy has long term impact on players • existing contract for heat sale between Kepco and KDHC sets precedent for transfer price for heat • the higher the PPA tariff the more KDHC will benefit • LT won market not tested : FX protection? • Acquisition vs. project financing vs. on balance sheet

The challenges: issues nobody wanted to talk about • How can it be done without Technical or Legal advisors? • Implicit negotiations between KDHC and KEPCO • Government expectations in relation to impact of risk allocation on prices? • Quality of the Data room? • Realism of the bid process timetable? • Flexibility to negotiate key terms if they are flagged by investors? • Overall Government commitment to transaction success? • Transparency of the prequalification and short-listing process?

Solutions • Short term PPA (1year) • Automatic renewal until • establishment of pool market • Contract for difference • in future • Partial fuel pass through structured to provide incentives to low electricity production at low demand time • Recognition of must run obligations but • under operational model

Solutions (cont’d) • Getting the right price: • Maximising investors interest • Critical mass: • O&M savings • Spare savings • Market share • Competitive tender with no deviation criteria • Allowing free hand on financing • Feedback between first and second rounds Gas play Electricity play District heating play

Commercial Structure: District Heating • 1. Obtain written letter from MOCIE on “fuel pass through” concept on DH price to end users • 2. Obtain assurance of growth possibility by securing licenses • 3. To the extent possible, provide strong rationale for growth story (expansion plan) • limited regulatory protection means that only serious DH players will have tools to properly value the assets

LNG play for investors Future liberalization Solutions for Fuel Supply Agreement (cont’d) Existing FSA with KEPCO • Medium term rather than matching PPA • Draft form for investors fine tuning

Overview of the Deal Timetable: What the Government was prepared to hear Information memorandum/ financial model sent to potential investors Preliminary non binding bids received (6 weeks) Shortlist of bidders announced June July August September October Phase I Phase II Detailed due diligence, meetings and site visits (6 weeks) Binding Bids received Winner announced; agreements signed Closing; funds received by KEPCO/ KDHC (3 weeks - 2 months) depending on sale structure

Marketing the Sale: Initial Steps • 40 investors contacted early on and marketed/updated regularly (once a week) • request for prequalification sent to interested parties and published on net • objectives: - select “large number” of potential candidates (either as leader in consortium or as potential consortium partner) • ensure high visibility to further Government continuing commitment • Pre-selection criteria: know how (district heating, LNG fired power stations, commitment to Korea and financial capabilities) • 23 parties pre-selected

Marketing the Sale: Info Memo • Info Memo sent to shortlisted parties with request for preliminary proposals demonstrating: • key capabilities (financial and technical) • level of commitment (understanding of business plan, treatment of employees due diligence requirement, conditions for closing) • willingness to commit to a price and list of “subject to”

Marketing the Sale: Info Memo • overview of Korea & Economy • DH and electricity sector description • description of facilities • description of main contractual terms • projections going forward and assumptions • personnel and organization • financial model • In the meantime, preparation of a data room

Shortlisting Serious Bids • Out of 23 pre-selected, 12 companies grouped forces into 6 consortiums ® 6 bids: • AES (US) • Singapore Power (Singapore) • Dalkia (France) / Sithe (US) Kukdong city gas / Kukdong oil (K) • British Gas (UK) / Daesung Industrial co (K) • Enron (US) / SK corp (K) • Tractebel (Belgium) Samchully (K)

Please wait while we are experiencing some technical difficulties…

Some problems with the process… • Wide price range in views of uncertainty (price with conditions) • Price is below expectation of Government, but fully expectable in view of the short due diligence process and uncertainties • Complaints in relation to the short time table for due diligence • common elements for additional requirements in contractual / sale process: the contractual risk structure was not fully acceptable • No way the full price will be paid within the time frame the Government wants

Next Step in selection process • Full due diligence (2-3 weeks) for shortlisted parties • Unconditional bid and fully marked up contractual documents (PPA, FSA, Asset Purchase Agreement) • Preferred bidder selection and final negotiation • close expected of year-end /beginning 2000

Actual timetable • Appointment of financial advisors: February 99 • Appointment of technical advisors April 99 • Appointment of legal advisors April 99 • Project launch : June 99 (request for prequalification) • Prequalification dues (without forming consortium) June 25 99 • Prequalification received: July 10 99 • Info memo scheduled to be sent to selected parties: 25th August 99, sent end September 99 • Indicative bids (non binding) scheduled for Nov 15 99, delayed until 1 week October 99 • Shortlisting down to 4 to do full due diligence • Bid submitted 15th December 99

Actual timetable • Process collapses ended December 99 • Government announced new Re tendering 12th January 00 • RFP documentation sent to bidders on 8 March 00 • Due diligence from bidders March to May 26 • Bid submission and announcement of preferred bidder 31st May 00 • Negotiations 1st to 28th June • Down payment of 10% of purchase price: 28th June 00 • Financial closed September 00

Relaunch of bidding process • Revised documentation and more Government support • Different mix of investors with much more local flavor • Many bidders on first round drop out entirely and some new players: • AES (US) • LG Caltex (LG and Texaco), Texaco (US) and Kukdong city Gas (K) • SK Corp (K) / El Paso (US) • Daesang (K) / Osaka Gas (Japan)

What is less well known • Most conditions that came as market feedback on first round are accepted • No significant difference in sale price achieved in view of the loosening of contractual conditions • Sales is a conditional one with 10% down payment while negotiations are ongoing for closure scheduled later • Financing plan based on Korean won with decreasing maturities (12 year maximum) • A large portion of the bonds are placed with Korean Development Bank (state owned) who is being asked to “ be helpful” by Government

Life goes on in a privatized company • February 2008: refinancing of company with a 1.77bn Won: 5 year grace period and 7 year tenor

Some Lessons Learnt • Thanks god there was no big competing transaction at the same time! • The timetable cannot be completely imposed by the Government • This is not just about the assets, but very much about the contracts around the assets • Unrealistic expectation to risk allocation lead to frustration and (at best) re-tendering • Investors appetite varies significantly with time. They can be frightened away even if the market potential is there • Uncertainty is okay but within a manageable framework • More upfront preparation upfront rarely hurt • Listening to market under competitive pressure makes sense • If the Government had followed the advisors advice, the process would have been shortened by one year.

Outcome • Large cross section of investors interested • Innovative financing solutions • Extensive transfer of risk • Sale price achieved matching expectation • Longer than anticipated timetable • Show that KEPCO/KDHC/NOCCF are willing to execute ?? transaction

THANK YOU !!! Raymond Bourdeaux The World Bank Rbourdeaux@worldbank.org PPP case study: Anyang & Buchon plants, South Korea