Download

1 / 14

150 likes | 158 Views

Learn why the cash flow statement is essential for understanding a company's financial health, including the net change in cash, sources and uses of cash, and the impact on operations, assets, liabilities, and equity.

E N D

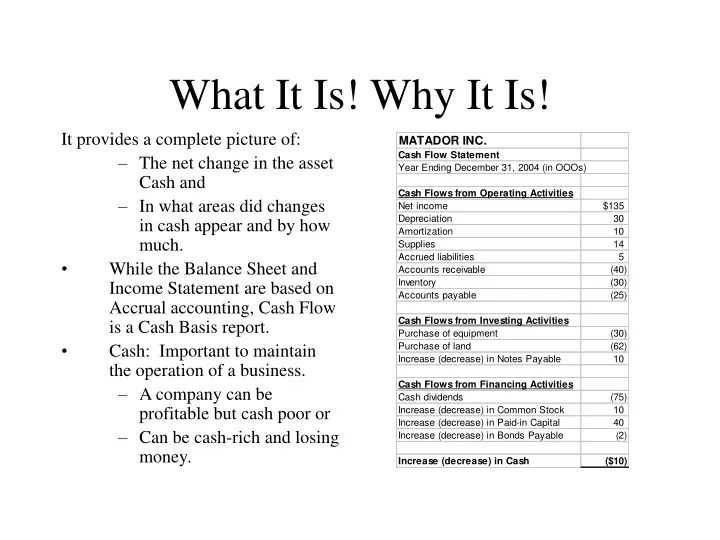

What It Is! Why It Is! It provides a complete picture of: • The net change in the asset Cash and • In what areas did changes in cash appear and by how much. • While the Balance Sheet and Income Statement are based on Accrual accounting, Cash Flow is a Cash Basis report. • Cash: Important to maintain the operation of a business. • A company can be profitable but cash poor or • Can be cash-rich and losing money.

Sources and Uses of Cash • The Cash Flow Statement shows: • Sources of cash (funds) over the accounting period • Uses of cash (funds) over the accounting period • The change in cash due to cash infusions (sources) and expenditures (uses). • There are only four possible Sources and Uses of cash: • Assets • Liabilities • Owners’ Equity • Operations (profit generating activities)

Sources of Cash • Assets • The Sales of an asset resulting in cash • Liabilities • An increase in borrowed money results in new cash. • Owners’ Equity • Investment of cash by owners or • The sale of stock results in new cash. • Operations • Selling goods or services for a Profit resulting in cash • A decrease in Inventory resulting in cash • A decrease in Accounts Receivable provides cash. • Depreciation of assets (a non-cash transaction) must be added back to reverse the reduction of Net Income.

Uses of Cash • Assets • Purchase of equipment, property or other assets. • Liabilities • Payment of loans and Accounts Payable • Owners’ Equity • Repurchase of stock • Payment of dividends • Withdrawal of cash or other assets by owners • Operations • Purchase of inventory, supplies and other operating expenses will decrease cash. • An increase in Accounts Receivable consumes additional cash. • Business losses consume cash.

Direct vs. Indirect Method • Direct Method: • Cash receipts and cash payments are used directly for determining Cash Flows from Operations • Indirect Method: • Changes in Current Assets, Current Liabilities and Net Income converts from Accrual accounting to Cash-basis accounting. • Cash Flows from Investing and Financing Activities are the same for both methods.

Creating a Cash Flow Statement (Indirect Method) • Cash Flows from Operations are transactions affecting: • Net Income • Working Capital (WC = CA – CL) • Cash Flows from Investing Activities are transactions affecting: • Non-Current Assets • Cash Flows from Financing Activities are transactions affecting: • Non-current debt • Owners’ Equity

Cash Flow from Operating Activities Cash flows from Operations Data SourceIncreaseDecrease Net Income Income Statement Source (Use) Depreciation and Amortization Income Statement Source Accounts Receivable Balance Sheet (Use) Source Inventory Balance Sheet (Use) Source Accounts Payable Balance Sheet Source (Use) Accrued Liabilities Balance Sheet Source (Use)

Cash Flows from Investing Activities Cash flows from Investing Data SourceIncreaseDecrease Investment in fixed assets Balance Sheet (Use) Source Purchase of Marketable Securities Balance Sheet (Use) Source

Cash Flows from Financing Activities Cash flows from Financing Data SourceIncreaseDecrease Short-term and Long-term debt Balance Sheet Source (Use) Payment of Dividends Income Statement (Use) Issuance of Stock Balance Sheet Source Stock repurchase Balance Sheet (Use)

Balance Sheet Current Assets + Non-current Assets Total Assets Current Liabilities + Non-current Liabilities Total Liabilities Invested Capital + Retained Earnings Total Owners Equity Income Statement Revenues - Expenses Net Income Statement of Retained Earnings Dividend Payment (Expense) Cash Flow Statement Cash Flows from Operations Cash Flows from Investing Activities Cash Flows from Financing Activities Creating a Cash Flow Statement (Indirect Method)