Download

1 / 24

240 likes | 340 Views

Job-Order Costing. Basic Costing Terminology…. Several key points from prior lecture: Cost Objects - including date, departments, customers, products, etc. Direct costs and tracing – materials and labor Indirect costs and allocation - overhead. …logically extended.

E N D

Basic Costing Terminology… • Several key points from prior lecture: • Cost Objects - including date, departments, customers, products, etc. • Direct costs and tracing – materials and labor • Indirect costs and allocation - overhead

…logically extended • Cost Pool – any logical grouping of related cost objects • Cost-allocation base – a cost driver is used as a basis upon which to build a systematic method of distributing indirect costs.

Costing Systems • Job-Costing: system accounting for distinct cost objects called Jobs. Each job may be different from the next, and consumes different resources • Wedding announcements, aircraft, televisions • Process-Costing: system accounting for mass production of identical or similar products • Oil refining, orange juice, soda pop

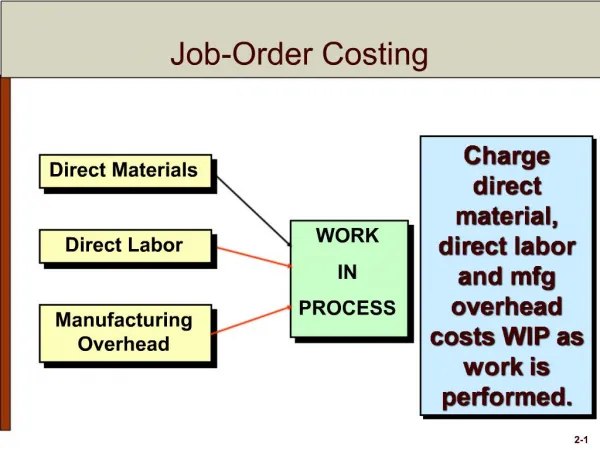

Job-Order Costing – An Overview Charge direct material and direct labor costs to each job as work is performed. Direct Materials Job No. 1 Direct Labor Job No. 2 Manufacturing Overhead Job No. 3

Direct Manufacturing Costs Manufacturing Overhead, including indirect materials and indirect labor, are allocated to all jobs rather than directly traced to each job. Direct Materials Job No. 1 Direct Labor Job No. 2 Manufacturing Overhead Job No. 3

PearCo Job Cost Sheet Job Number A - 143 Date Initiated 3-4-05 Date Completed Department B3 Units Completed Item Wooden cargo crate Direct Materials Direct Labor Manufacturing Overhead Req. No. Amount Ticket Hours Amount Hours Rate Amount Cost Summary Units Shipped Direct Materials Date Number Balance Direct Labor Manufacturing Overhead Total Cost Unit Product Cost The Job Cost Sheet

Will E. Delite Measuring Direct Materials Cost

Why Use an Allocation Base? Manufacturing overhead is applied to jobs that are in process. An allocation base, such as direct labor hours, direct labor dollars, direct material dollars or machine hours, is used to assign manufacturing overhead to individual jobs. • We use an allocation base because: • It is impossible or difficult to trace overhead costs to particular jobs. • Manufacturing overhead consists of many different items ranging from the grease used in machines to production manager’s salary.

Estimated total manufacturingoverhead cost for the coming period POHR = Estimated total units in theallocation base for the coming period Ideally, the allocation base is a cost driver that causes overhead. Manufacturing Overhead Application The predetermined overhead rate (POHR) used to apply overhead to jobs is determined before the period begins.

The Need for a POHR Using a predetermined rate makes itpossible to estimate total job costs sooner. Actual overhead for the period is notknown until the end of the period. $

Overhead applied = POHR × Actual activity Application of Manufacturing Overhead Based on estimates, and determined before the period begins. Actual amount of the allocation based upon the actual level of activity.

Estimated total manufacturingoverhead cost for the coming period POHR = Estimated total units in theallocation base for the coming period $640,000 POHR = 160,000 direct labor hours (DLH) Overhead Application Rate POHR = $4.00 per DLH For each direct labor hour worked on a particular job, $4.00 of factory overhead will be applied to that job.

Interpreting the Average Unit Cost The average unit cost should not be interpreted as the costs that would actually be incurred if anadditional unit were produced.Fixed overhead would not change if another unitwere produced, so the incremental cost of another unit may be somewhat less than $118.

Problems of Overhead Application The difference between the overhead cost applied to Work in Process and the actual overhead costs of a period is referred to as either underapplied or overapplied overhead. Underapplied overhead exists when the amount of overhead applied to jobs during the period using the predetermined overhead rate is less than the total amount of overhead actually incurred during the period. Overapplied overhead exists when the amount of overhead applied to jobs during the period using the predetermined overhead rate is greater than the total amount of overhead actually incurred during the period.

Practice with Overhead • Actual manufacturing overhead $340,000 • Budgeted machine hours 10,000 • Budgeted direct labor hours 20,000 • Budgeted direct labor rate $14 • Budgeted manufacturing oh $364,000 • Actual machine hours 11,000 • Actual direct labor hours 18,000 • Actual direct labor rate $15 • POHR - Machine hours • POHR - direct labor hours • POHR - direct labor dollars

Job-Order System Cost Flows Word Documents Fisher Company Journal Entries T-Accounts Over/Under-applied Overhead Cost of Goods Manufactured Cost of Goods Sold Income Statement

Overapplied and Underapplied Manufacturing Overhead - Summary

May be more complex but . . . May be more accurate because it reflects differences across departments. Multiple Predetermined Overhead Rates To this point, we have assumed that there is a single predetermined overhead rate called a plantwide overhead rate. Large companies often use multiple predetermined overhead rates.