Download

1 / 64

640 likes | 848 Views

October 9th 2008. Global Economy, UK Recession and the Outlook for Agriculture. David Tinsley UK Economist nabCapital, London David.tinsley@eu.nabgroup,com. Global outlook. Two years of slower global growth ahead…. Source: IMF WEO.

E N D

October 9th 2008 Global Economy, UK Recession and the Outlook for Agriculture David Tinsley UK Economist nabCapital, London David.tinsley@eu.nabgroup,com

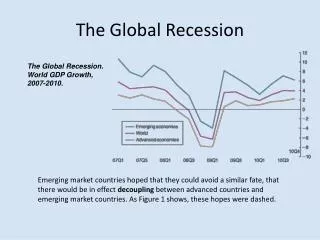

Two years of slower global growth ahead… Source: IMF WEO • From 2004 onwards, global growth picked-up well above its long run average of 3.5% to rates around 5%, its strongest performance since the 1980s. • Although the IMF have revised down the growth prospects for the United States, eurozone and Japan in light of the global credit crunch, global growth is still expected to dip below its long-run average, slowing from 3.9% in 2008 to 3.0% in 2009 before recovering in 2010.

…the slowdown is being felt across the advanced economies and particularly strongly in some of the smaller eurozone economies • Some areas of Europe will struggle. • Note the weakness in Italy and Spain. The Irish economy is also slowing quickly.

Forecasts have been for strong pockets of growth outside the advanced economies… Source: IMF WEO • Not only China and India. • Central and Eastern Europe is expected to grow by over 4% in real terms, more than twice the rate as the United Kingdom. • High oil prices mean that Russia and other CIS member states will grow by over 6%, in line with other Asian economies. • So trade linkages will provide opportunities for growth.

The credit crunch is still ongoing Source: Bloomberg • Recent developments suggest that we are now at the end of the beginning as banks are actively forced to deleverage in order to remain in business • Further consolidation looks inevitable. • Money markets remain stressed and it now seems that quarter-ends are causing more problems despite central bank liquidity injections.

As write-offs exceed capital raising • Gap currently $149.9 billion, which explains why banks refuse to still trust one another. • It also explains the switch by authorities to look at recapitalising banks rather than simply protecting depositors.

Important though to keep the overall size in perspective Source: IMF Global Financial Stability Review (October 2008) • Although the most recent estimates put total financial losses at up to $1.4 trillion, as a percentage of GDP, this is much smaller than the Asian crisis or indeed the Japanese banking crisis of the 1990s. • It is also geographically much more widely spread.

In response, central banks are now easing Source: Bloomberg • Central banks engaged in co-ordinated rate cuts, easing by 50bps. • Attempts to reduce the cost of money are now running alongside attempts to increase its quantity. • Previous history suggests that central banks are happy to create steep yield curves to recapitalise the banking system as well as other methods.

Sharp US slowdown, so global growth now driven by India and China Source: NAB Economics • Strong growth in China and India provides the major offset to US misery. Two years of below trend growth suggest that the US could endure a ‘growth recession’. • We remain more pessimistic than the IMF on global growth. In particular we look for a larger slowdown in the developed world as the credit crunch feeds through. • There are also downside risks in 2009/2010.

The Bad: Lost output can takes years to make good and unemployment rises sharply • In the early 80s recession the loss of output was 4.8%, while in the 1990s recession it was 2.5%. • In the early 1980s and 1990s recessions output was still below its pre-recession level three years later. • In those recessions the unemployment rate almost doubled.

The Bad: Real house prices decline significantly • Real house prices fell by around 20% after the onset of the 1990s recession. But they had already fallen by around 15% before GDP growth had gone negative, so the total fall was around 35%. And in real terms house prices did not get back to their previous high for the rest of the decade. • In the past two recessions, real equity prices have tended to fall most immediately before and in the first quarter of a recession

The Ugly: The UK economy has stalled… • There was no growth in the second quarter, with an annual rate of 1.4%. Growth in Q1 was just 0.3%. • If ‘trend’ growth is 0.7% per quarter then we have already had a year of below trend growth.

…with the credit crunch hitting service sector output Source: ONS • Service sector output growth was 0.2% in Q2, compared to an average of 0.8% in 2007. • The contribution from business and financial services has slowed markedly in recent quarters. In 2007 Q2 it was as large as 0.6pp. Now it is virtually zero. And distribution, hotels and catering has also slowed markedly.

The financial sector will shrink • Just to keep things in perspective, financial intermediation takes up only 8% of the economy. • A contraction in output of the same order of magnitude as 2002 could see 50,000 jobs lost as the sector returns to just 5% of GDP. • International banking consolidation suggests that even more jobs will be lost than in the ‘tech wreck.’

…and real spending is also being hit by rising prices Source: Reuters / Ecowin • Higher food and energy prices are eating into household’s spending power. • Real spending power fell by 1.0% in Q1 – the first fall since 2006 Q4 and the biggest since 1999. • Real disposable income grew in the second quarter as small tax cuts were made, but peaking inflation is likely to restrain it in the second half of the year.

So the consumer is very unhappy… Sources: GfK. • The July GfK measure of consumer confidence fell to lowest level since 1990. • The recovery since then has been marginal and probably reflects some boost from falling oil prices.

The slowing housing market will be a drag on consumption… Sources: National Statistics, Nationwide. • Falling perceptions of wealth will hit spending. And consumption linked to house-moves will slump. Central estimates suggest that a 1% fall in house prices reduce consumption by 0.1% over time. • The current rate of house price inflation is consistent with annual volumes growth close to zero - suggesting that the retail slowdown is only just beginning.

And slowing growth means a deterioration in the labour market Source: Reuters Ecowin Source: Reuters Ecowin • The numbers claiming unemployment benefit rose by 32,500 in August. The numbers claiming unemployment benefit has increased by 110,000 in the last seven months. • 15,000 jobs lost in financial services alone in the six months to June. However, these do not show up in claimant count data but do in the wider ILO measure.

Which will get worse Source: Reuters Ecowin • Four quarters of below trend growth have seen the inflow into the pool of unemployed pick up sharply in recent months, while the outflow rate has fallen. • In other words, those in the pool of unemployed stay there for longer, which will drain aggregate income in the economy and so weigh on spending.

Banks are unwilling to lend Lending intentions: next three months Source: Bank of England • The BoE credit conditions survey shows that banks are restricting credit to UK households. • Unsecured lending and lending to commercial real estate have been the hardest hit.

And rising arrears • The increased cost and reduced availability of credit has seen arrears start to rise. • With house prices falling, lenders are much quicker to seize properties, especially those who have exited the UK mortgage market. • At 18,900 repossessions rose above their long-run average in the first half of this year and we expect to see further increases over the next year or so.

By historical measures the housing market is extremely overvalued Source: Nationwide • In real terms, house prices fell by 37% from peak to trough in the last downturn and took 12 years to regain their previous peak. • So far house prices have fallen by just over 5%. • Given that prices in real terms are just as relatively overvalued now as in 1989, it is clear where 40% housing falls come from. With inflation lower this time around, nominal falls have to be higher.

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 And prices have fallen at an extremely fast pace 102 100 98 1989-98 (Bottom scale) 96 94 92 90 88 2007- date (top scale) 86 84 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 Source: Datastream • House prices has so far fallen around 11% from their peak • Note that after the last housing market slump which began in 1989, it took 116 months to regain previous peak levels.

Meaning that houses are no longer ATM machines • After a decade of withdrawals, home owners injected £2.7 billion of equity into the housing market in the three months to June. • That represents a 1.2% fall in disposable income, reducing the ability to consume further.

The risks are heavily skewed to the downside • We expect growth of just 1.0% in 2008 and 0.6% in 2009. • The risks to our growth forecast are not symmetric. Much greater chance of a more negative outturn.

The Good: The current slowdown will be the most severe this century… • And the scale of this slowdown will be a lot longer and deeper (especially compared with 2004).

…and we expect a technical recession • But it will remain modest compared with the output losses seen in the early 1980s and 1990s. • After a brief fall, growth should start to resume back towards trend. • Note though, that lower losses mean that growth will not bounce back as strongly.

But inflation should ease rapidly in the coming months… • We look for CPI to peak at 5.1% in September, remaining at 3.0% or higher until June 2009. • But weakening activity should see underlying inflation ease and allow rate cuts.

…and any reversal in libor spreads would add to the stimulus Source: Bloomberg • Looking at the spread between inter-bank rates and the Bank of England base rate, we see the long-term average has been below 20 basis points • But since last summer the spread has ballooned, and remains elevated. • Should market tensions ease, credit costs will fall extremely sharply.

…and any reversal in libor rates would add to the stimulus • Comparing forecasts of Bank Rate against three-month libor futures contracts, it seems that markets do not expect the spread to return to ‘normal’ levels anytime soon.

Previous episodes of financial stress suggest that spreads can fall back very quickly • The current stresses and strains are not unprecedented. • Back in September 1981, the spread widened to 288bps before easing by to 38 by end of March 1982. • A similar retracement would be the equivalent of a 75bps rate cut on top of any additional cuts in Bank Rate by the MPC.

So the economy should be growing just below trend in 2010 • Even by 2010, consumption will still be close to levels seen this year. • Government spending and investment will support growth in the meanwhile. • But how plausible is this?

UK labour market fundamentals are different Source: Office for National Statistics • Most of the 3 million+ jobs created since 1997 have gone to non-UK sources. • Most are economic migrants who would be expected to return to their countries of origin in the event of job losses. • So the rise in the UK claimant count will be much less than in the 1990s.

Eastern European workers have become the fastest growing sector Source: Office for National Statistics • Accession 8 countries now account for 508,000 jobs, back in 2004 there were just 76,000 employees. • Most tend to be concentrated in construction, leisure and tourist sectors all of which are more likely to be adversely affected by the consumer downturn. • So we could see half a million jobs lost in the UK with little increase in the UK claimant count rate as migrant workers are not eligible to claim it.

Government spending will support growth as the private sector stagnates • Government spending will continue to boost growth this year and next. • Investment grows by 11.5%yoy in 2008-09 before stabilising at around 6%. That suggests that it should contribute to GDP growth this year. • Net investment rates have also been very strong in 2007-08 and 2008-09. The slowdown in later years is another reason to remain suspicious of HMT growth forecasts.

Though public finances are the biggest constraint on extra Government intervention (1) Public sector net borrowing £ billion 2001 2002 2003 2004 2005 2006 2007 2008 45 40 35 30 25 20 15 10 5 0 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 Source: nabCapital • HM Treasury is consistently overoptimistic when forecasting future PSBR • Already, the forecast for 2008/09 has been revised up from £23bn to £24bn, £25bn, £29bn and now £42bn.

Though public finances are the biggest constraint on extra Government intervention (2) Public sector net borrowing £ billion 70 2008 Budget Treasury Forecast 60 nabCapital forecast 50 40 30 20 10 0 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 Source: Datastream • HM Treasury yet again forecasts that the PSBR will be lower in future years. • Our Central Forecast is that borrowing will hit £70bn in 2009/10 and if the recession proves deep and prolonged, the risk is that we could see a deficit as high as £100bn.

Net trade may also provide some support, though limited • Sterling has fallen by around 17% against the euro over the past year. • That should have boosted UK competitiveness substantially. However, it seems that exporters have responded by raising prices aggressively. • Export price inflation is currently around 10%yoy, so volume growth will not be as strong as post-ERM exit.

And further falls in the pound look likely • We have long been bearish on sterling, but even our 15-month targets have now been met. • The downgrading of UK and eurozone growth prospects have helped boost the US dollar and push down on commodities prices. • We look for sterling and the euro to trade within a narrow range given that both are soft.

And corporate balance sheets may be better placed to withstand the downturn than previously Source: Office for National Statistics • The corporate rate of return is high going into the downturn, especially for service sector firms. • And the rate of insolvencies remains fairly low by historical comparisons.

And companies have plenty of cash on hand Source: Office for National Statistics • Business investment is also likely to hold up better than expected as non-financial corporates still have plenty of funds on hand. • The forced deleveraging of the banking system will be focused on the housing system.

Note that not all is doom and gloom in the housing market • The UK has not experienced the building booms seen elsewhere, especially when compared with the United States and Spain. • Indeed construction activity is slowing sharply. Any oversupply of housing could well have disappeared by 2010, especially as housing gets cheaper.

Conclusions: Global • Despite the global credit crunch, the global economy looks to be in reasonable shape with growth this year and next just below historical averages. But that reflects the performance of the emerging markets. The advanced economies will slow sharply. • We are now at the ‘end of the beginning’ of the credit crunch. The financial sector will not return to its pre-2007 shape. There will be fewer banks and less credit product. Indeed, the entire sector is likely to contract. • A battery of policy measures by the Fed alongside deep cuts in interest rates means the US economy seems to have avoided the worst-case scenarios. We expect the Fed to pause for now. A stronger US dollar would have a much more immediate impact on stimulating the economy through lower gasoline and food prices. • Eurozone will grow at roughly the same rate as the UK, but note country level differences. Germany and France will do OK, but Italy looks in recession and risks being joined by Ireland and Spain. • Other global risks come from a slowdown in China in the second half of 2008 after the Beijing Olympics. However, so far, there is little sign that growth is slowing at all. • Main risk now is that emerging markets start to get infected by the credit crunch, removing the main hope of navigating through the turmoil in relative safety.

Conclusions: UK • In the UK the household sector is under considerable stress and a sharp retrenchment looks likely. UK growth will slow to 1.0% this year and 0.6% next. • The economy will enter a technical recession by the end of this year. However, it should prove less deep than previous episodes. • We still see a very large adjustment in property prices as we have seen in every other recession. With inflation lower, the fall in nominal house prices will have to be even larger and a fall in nominal terms of 25% to 30% is possible. • Although consumer spending will fall sharply as household budgets fall and debt is repaid, there is enough strengths in other sectors. • Easing inflation will provide scope for BoE rate cuts. Money market spreads could ease back by the end of March 2009. • Unemployment is not likely to rise as sharply as feared given recent reliance on migrant labour. • Government spending and investment will support some businesses, especially those in infrastructure. • Corporate balance sheets are in very good shape. Most will be able to wait out the recession. Some will benefit from falling asset prices. • Net exports are also likely to provide a lift, especially if sterling falls back against the US dollar and any contagion of the credit crunch to emerging markets is contained. • By 2010, growth will return to trend.

What’s driving the world market? Supply constraints Higher input costs for farmers Poor weather conditions Demand growth Incomes, population and westernisation of diets Low stocks Commercial and government Reduced policy intervention Reform of CAP Higher substitute prices Soy protein and vegetable oils