Download

1 / 11

110 likes | 125 Views

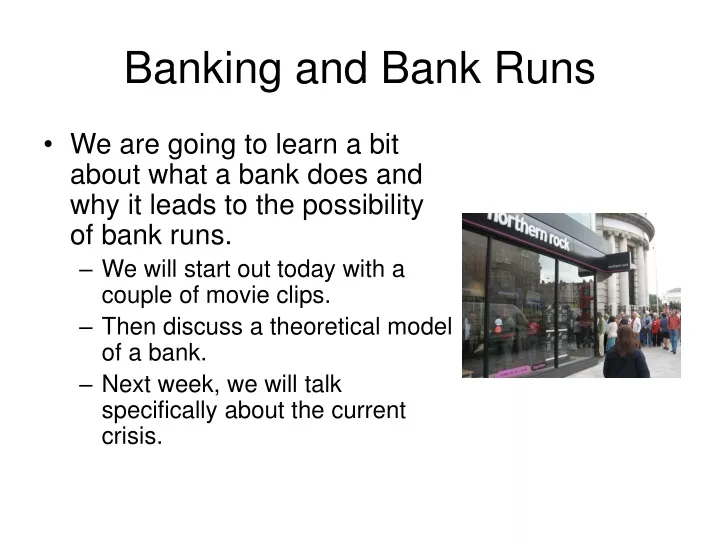

Banking and Bank Runs. We are going to learn a bit about what a bank does and why it leads to the possibility of bank runs. We will start out today with a couple of movie clips. Then discuss a theoretical model of a bank. Next week, we will talk specifically about the current crisis.

E N D

Banking and Bank Runs • We are going to learn a bit about what a bank does and why it leads to the possibility of bank runs. • We will start out today with a couple of movie clips. • Then discuss a theoretical model of a bank. • Next week, we will talk specifically about the current crisis.

Mary Poppins • Two things to notice. • Bank Run was caused by panic w/o financial reasons. The bank was fully solvent. • The bank closed its doors: stopped payment.

It’s a Wonderful Life • It was a systemic panic. • There may have been a justification for the bank run. • A bank takes money and invests it in long-term assets (mortgages). • The bank can’t easily liquidate these assets. • The bank did not fully suspend payments. Doing so would hurt depositors. • There was a degree of negotiation on who gets what.

Diamond Dybvig Model (1983) • Captures elements of what a bank does. • Shows that there is a basic problem of bank runs. • The model consists of two parties. • Depositors • Banks • The model has three time periods: yesterday, today and tomorrow.

Depositors • Depositors placed money (say £1000) in a bank (yesterday) before learning when they need the money. • Depositors either need their money today (impatient) or tomorrow (patient). There is a 50% chance of being either type. • The ones that need their money tomorrow can always take the money today and hold onto it. • The ones that need money today get relatively very little utility for the money tomorrow.

Banks • Banks have both a short term and a long term investment opportunity for the money. • The short term investment (reserves) is locking the money in the vault. This investment returns the exact amount invested. • The long term investment returns an amount R tomorrow. It is illiquid and returns only L<1 today.

Deposit Contract • The depositors invested £1000 yesterday have a contract with the bank. • The depositors can withdraw their money today and receive £1000 or wait until tomorrow and receive R*£1000.

Bank’s decision • How can the bank meet this contract? • The bank can divide into two parts. • Take half and keep it as reserves. • Take the other half and put it in the long term investment. • Say there are 10 depositors: 5 patient and 5 impatient. The bank puts £5000 in the vault and invests £5000. • Demands today are 5*1000, and 5*R*1000. The bank has 5000 and R*5000 tomorrow. • Thus, a bank makes zero profit.

Danger! • The bank can not always remain solvent. • If too many depositors try to withdraw today, it won’t be able to meet the contract tomorrow. • For instance if 7 depositors withdraw today, then the bank can pay 5000 out of reserves. It then must sell its illiquid asset to meet the rest of the needs, £2000. • How much must it sell to meet the needs? How much is left? • How much does those withdrawing tomorrow receive? • On average, how much does those withdrawing today receive? • At what value of L does is the bank unable to meet demands today for those 7 depositors?

Multiple equilibria • This leads to multiple (Nash) equilibria. • It is inherent in banking. • Here is an example with 2 patient depositors (and 2 impatient depositors). • This forms a 2x2 game between the patient depositors. • R=1.5 and L=.5

Game between patient depositors Depositor 1 Tomorrow Today 0 3/4 Today 3/4 1 Depositor 2 1 3/2 Tomorrow 0 3/2 R=1.5, L=.5