Download

1 / 26

260 likes | 260 Views

This talk focuses on emergent risks in financial markets, particularly the May 6, 2010 flash crash. It examines the risks faced by individual firms and the challenges of evaluating securities in automated trading systems. Through interviews, press, and technical literature, it explores the impact of algorithmic trading on market liquidity and the potential for system failures. The talk also highlights instances of software bugs and feedback loops leading to price spikes and crashes.

E N D

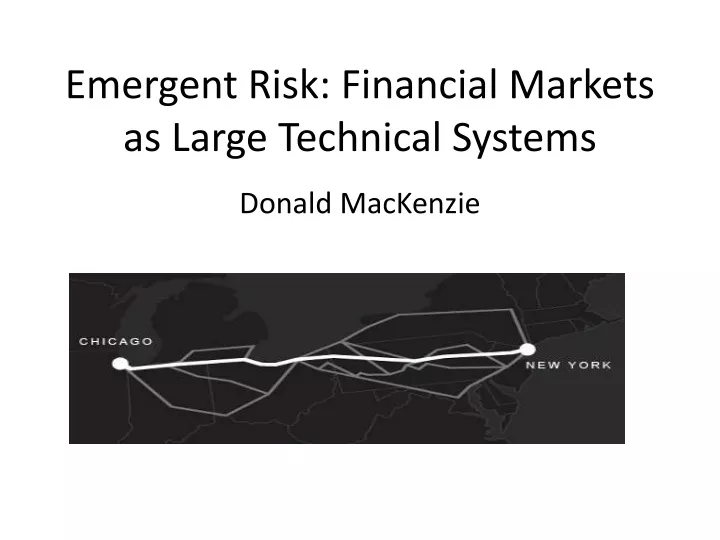

Emergent Risk: Financial Markets as Large Technical Systems Donald MacKenzie

Automated trading: various ways of theorising from an economic sociology/science and technology studies viewpoint. E.g.: Via Carruthers and Stinchcombe, ‘The Social Structure of Liquidity’, Theory and Society 28 (1999). Article with Beunza, Millo and Pardo-Guerra, Journal of Cultural Economy 5 (2012). Via the literature on the sociology of evaluation (e.g. review by Lamont, Annual Review of Sociology 2012): how do automated trading systems evaluate securities? Work in progress.

In this talk, focus directly on risk, esp. emergent • The first full-scale crisis of automated trading, May 6, 2010 (the ‘flash crash’) • Risks to individual firms; emergent risks Sources: 51 interviews with personnel of automated trading firms, trading venues etc; trade press and technical literature; CFTC/SEC report on flash crash (criticism by Nanex).

May 6, 2010: ‘everyone was watching the TV screens, the fires in Greece were raging’ (interviewee)

May 6, 2010, 2:32pm: Kansas City. Sell Algorithm: 75,000 E-Minis (approx $4.1 bn) CFTC/SEC report has linear narrative starting with the Sell Algorithm. No other convincing narrative available. If Nanex criticism of CFTC/SEC correct, the events I’m describing are even more disturbing instance of emergent risk.

Chicago Mercantile Exchange’s data centre, 2:41pm: Sell Algorithm trying to sell 9% of previous minute’s volume (CFTC/SEC); automated High-Frequency Traders (net long 3,300 E-Minis) and other trading systems begin to sell

Proprietary High-Frequency Trading ‘Electronic market-making’: automatic submission and (nearly always) cancellation of limit orders. Earn ‘spread’ by selling at offer and buying at bid. ‘Structural arbitrage’: e.g. E-Mini (now, western suburbs of Chicago), SPY, shares (NJ). Statistical arbitrage (e.g. pairs trading, order book dynamics). Deliberate order anticipation (‘algo sniffing’). Deliberate ‘momentum ignition’.

2:45:13 – 2:45:27 ‘hot potato’ trading among High-Frequency Traders. E-Mini price down 5%; buy-side depth down to $58 million (Sell Algorithm trying to sell $4.1 bn.) Crisis ramifying via fibre-optic links into share-trading data centres (e.g. SPY falls 6%, buy-side depth collapses).

At around 2:45pm, market participants face an interpretive puzzle: ‘Maybe a nuclear bomb went off’ (interviewee). Perhaps the data feeds were corrupted. Perhaps it was a panic.

‘This isn’t right’ (interviewee) ‘HF STOP’ (e.g. Red Bank, NJ)

Evaporation of liquidity: order cancellations empty the order books. Market orders executed at ‘stub quotes’: $0.01 (e.g. Accenture), $99,999.99 (Sotheby’s)

2. Risks ‘[T]he only way I had to test my system was to turn it on and trade with real money … the boss said ‘turn it on’, I said no, the boss said ‘turn it on’, I said no, and we went back and forth … and then I said okay … I said ‘I want you to know I’m telling you not to do this’, and he said ‘don’t worry about it, turn it on’. The thing went haywire and we couldn’t turn it off and the boss in his Armani suit or whatever, jumping underneath the desks pulling out plugs from the wall’ (interviewee)

Risks to individual firms. E.g.: February 3, 2010, 1:26:28pm Infinium algorithm enters orders for 6,767 oil futures in 3 seconds. $1.03 million loss; $850,000 fines. ‘[I]t happens all the time … I would say at least once a month you hear of a large trading firm whose system went haywire, “oh, did you hear about firm XYZ, their system sent in 31,000 orders yesterday in five milliseconds” … a lot of this stuff doesn’t make the press … fines [are] a perverse incentive not to self-report’ (interviewee)

Risks to individual firms: August 1, 2012, first 45 minutes of trading on NYSE. Knight Capital loses $440 million: ‘It was a software bug, it just happened to be a large software bug’ (Thomas Joyce, Knight CEO)

‘[E]mergent risk is the threat to the individual parts produced by their participation in and interaction with the system itself’ (Centeno and Tham) ‘Bug-free’ algorithms can interact in unexpected ways, e.g. feedback loops.

Price spikes and crashes, Amazon sellers: August 23, 2012, 8:41pm c. £1,700 (observed by Alex Preda) August 23, 2012, 8:42pm £1,965 (observed by Alex Preda) August 30, 2012, 12:19pm £103 (observed by Donald MacKenzie)

profnath’s algorithm: set price at 0.99830 times lowest price bordeebook’s algorithm: set price at 1.270589 times lowest price Research by Michael Eisen, evolutionary biologist at UC Berkeley

Flash crash has some elements of emergent risk (especially if Nanex critique of CFTC/SEC is correct). US stock markets and related derivatives markets have become a large technical system of giant data centres connected by ultra-fast fibre-optic cables.

In stocks, futures and currencies, large technical systems are becoming global:

Large technical system dynamics: At timescales below human reaction times, ‘mixed human-machine’ ecology gives way to ‘all-machine’ ecology with different dynamics (Neil Johnson et al, arXiv:1202.1448v1 [physics.soc-ph]) Different dynamics: e.g. ‘efficient market hypothesis’ seems to break down at timescales of ‘all-machine’ ecology. Viability of HFT as a business suggests very short-horizon price prediction possible (using order-book dynamics and e.g. ‘futures lag’).

Delegitimation? Lay investors believe themselves to face ‘a treacherous market ruled by machines’? (Lex, Financial Times, Aug 9-10, 2010, p.24) TABB Group annual surveys of institutional investors in US equities. Market structure ‘very weak’: May 2010: 3% May 2012: 26% (BATS and Facebook IPOs?)

x nuclear plant x rail tightly coupled loosely coupled x assembly-line x university linear complex The large technical system of finance is in Charles Perrow’s dangerous quadrant of tight coupling and high complexity. The ‘flash crash’ as normal accident?

Keeping perspective: • Delegitimation means that the ‘normalization of deviance’ (Vaughan) is not taking place. • Via SEC, US stock something of a ‘learning’ system (see ‘Berkeley high-reliability school’). • Disruption to ‘fixed-income’ (credit) markets more dangerous than disruption of stock markets. The three people who died on May 6, 2010 were in Greece. • Large technical systems not yet ubiquitous. As yet, little automated trading of fixed-income instruments (no equivalent of SEC to undercut dealers’ opposition).

Limit order book for Astoria Financial, c. noon, October 21, 2011