Download

1 / 23

230 likes | 385 Views

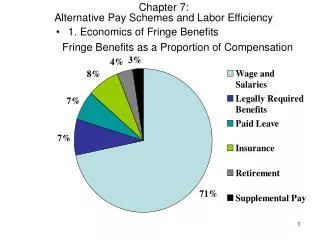

FRINGE BENEFITS. AUTOMOBILES AWARDS,PRIZES CELLULAR PHONES EDUCATIONAL REIMUBURSEMENTS SAVINGS BONDS ALLOWANCES MEAL MONEY (BASED ON HOURS WORKED). GROUP TERM LIFE MOVING EXPENSES PARKING ER PROVIDED LIVING QUARTERS CLOTHING OTHER THAN CERTAIN UNIFORMS SPOUSAL TRAVEL

E N D

AUTOMOBILES AWARDS,PRIZES CELLULAR PHONES EDUCATIONAL REIMUBURSEMENTS SAVINGS BONDS ALLOWANCES MEAL MONEY (BASED ON HOURS WORKED) GROUP TERM LIFE MOVING EXPENSES PARKING ER PROVIDED LIVING QUARTERS CLOTHING OTHER THAN CERTAIN UNIFORMS SPOUSAL TRAVEL SEASON TICKETS Examples of Fringes CASH NON-CASH

Accident and health plans achievement awards athletic facilities de minims fringes dependent care asst. programs educational assist employee discounts Group-term life lodging on employer’s premises moving expenses reimbursements no-additional cost services tuition reduction working condition fringes EXAMPLES OF EXCLUDED FRINGES

TAXATION OF BENEFITS • ALL REMUNERATION, CASH OR NON- CASH, ARE CONSIDERED GROSS INCOME UNLESS SPECIFICALLY EXEMPT BY LAW. (IRC 61) • BUSINESS PORTION MAY BE EXCLUDED AS A “WORKING CONDITION” FRINGE BENEFIT...(IRC 132) • PROVIDED THE RECORDKEEPING REQUIREMENTS OF IRC 274ARE MET.

Automobiles • PERSONAL USE CONSTITUTESWAGES • VALUATION METHODS: Cents per mile ($.565/Mile 2013) Commuter rule ($1.50 each way/day) Annual Lease Valuation

CENTS-PER-MILE • FMV of auto must be less than $16,000 for automobile; $17,000 for truck - 2013 • At Least 50 Percent Of Annual Mileage Must Be For Business Use • Must Be Actually Driven At Least 10,000 Miles Per Year (May Be All Personal Miles) • Used During The Year Primarily By Employees.

COMMUTER RULE • Must own or lease vehicle and provide vehicle to one or more employees • Auto must be provided for bona fide non-compensatory reasons – i.e., on-call • Must have written policy that prohibits personal use other than commuting or de minims personal use. • Cannot be used for Control employee • Government Control employee is any elected official or employee whose salary exceeds $145,700 for 2011.

ANNUAL LEASE VALUATION • Annual Lease Value Table provides annual lease amount based on the fair market value of the automobile. • Prorate annual lease amount based on percentage of personal use. • Additional $.055 mile charged for each personal mile if employer provides fuel. • Records must be maintained to show total miles and personal or business use. • Employer may elect to tax 100% personal.

Exempt Vehicles • Clearly Marked Police or Fire Vehicles • Unmarked Police Cars * • Ambulances or Hearses • Large Trucks • School Buses

EMPLOYEE EXPENSE REIMBURSEMENTPLANS: Must have an “Accountable Plan”

MUST MEET ALL THREE RULES TO BE ACCOUNTABLE: • Have a Business Connection • Be Substantiated by the Employee • Return of Excess Reimbursements

REIMBURSEMENTS THAT MAY BE WAGES: • AUTOMOBILE EXPENSE REIMBURSEMENTS • MEALS • LODGING • CLOTHING • MATERIALS AND TOOLS • MOVING EXPENSES

NON-ACCOUNTABLE PLANS • EXPENSES ARE NOT SUBSTANTIATED TO YOU WITH DOCUMENTS, SUCH AS RECEIPTS. • ADVANCES ARE NOT ACCOUNTED FOR AND/OR AMOUNTS IN EXCESS ARE NOT RETURNED TO YOU WITHIN A REASONABLE PERIOD OF TIME. • REASONABLE PERIOD OF TIME IS WITHIN 120 DAYS.

Types of Allowances • Car Allowance • Uniform Allowance • Moving Allowance • Travel Advance • Tool Allowance

Cell Phones and Computers • Computers are considered “listed property” • Must account for personal use • Personal use taxable wages • Wages subject to all employment tax • NOTE: Cell phones are no longer considered “listed property” – must be noncompensatory reasons

Supper Money • Must be paid to enable employee to work overtime • Based on hours worked - Taxable wages • Subject to all employment taxes

Longevity Pay • Report on Form W-2 • Do NOT report on Form 1099-Misc • Subject to all employment taxes

Reimbursement Personal Expenses • Payment for meals, not away overnight - Personal • Uniforms must be qualified • Plain clothes detectives - reimbursed for torn suit - Personal

Resources • Publications 15, 15A, 15B • IRC Section 3121 • Payroll Management Guides • NC 218 Coordinator • Internal Revenue Service

Idaho FSLG Specialist • Chris Casteel • Phone: 208-363-8818 • Fax: 208-387-2849 • E-mail: • chris.k.casteel@irs.gov • Address: • 550 West Fort • Boise, ID 83724