Download

1 / 17

170 likes | 568 Views

Adjustments and the Ten-Column Work Sheet. Chapter 18. Identifying Accounts to be Adjusted and Adjusting Merchandise Inventory. Worksheet – to determine net income or net loss and to determine stockholders’ equity 10 Column Worksheet vs 6 Column Worksheet Trial Balance Adjustments

E N D

Adjustments and the Ten-Column Work Sheet Chapter 18

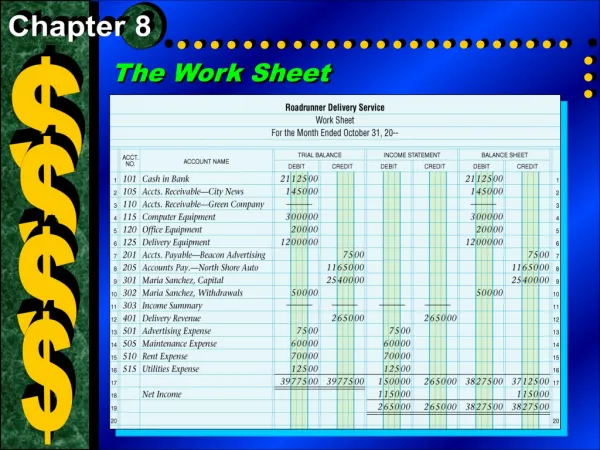

Identifying Accounts to be Adjusted and Adjusting Merchandise Inventory • Worksheet – to determine net income or net loss and to determine stockholders’ equity • 10 Column Worksheet vs 6 Column Worksheet • Trial Balance • Adjustments • Adjusted Trial Balance • Income Statement • Balance Sheet Pg 518

Trial Balance • A trial balance is prepared to prove the equality of debits and credits in the general ledger. Pg 519

Calculating Adjustments • Not all changes in account balances result form daily business transactions. • Some changes result from internal business operations or the passage of time. • Supplies get depleted over time • Insurance is paid up front and used a little at a time • Large assets decrease in value (depreciate) Pgs 519-520

Permanent Accounts vs Temporary Accounts • Adjustment – an amount that is added to or subtracted from an account balance to bring that balance up to date. • Every adjustment affects at least one permanent account and one temporary account • At the end of the period, adjustments are made to transfer the cost of the asset accounts (permanent accounts) to the appropriate expense accounts (temporary accounts) • These assets are “expensed” meaning the expense is recorded in the same period the revenue/value for that asset was recorded. Pg 520

Determining the Adjustments Needed • How do you know which accounts to adjust? • Review each account balance in the work sheet’s Trial Balance section. If the balance for an account is not “up to date” as of the last day of the fiscal period, that account balance must be adjusted. • Merchandise Inventory • Supplies • Prepaid Insurance • Federal Corporate Income Tax Pgs 520-521

Adjusting Merchandise Inventory • The balance in Merchandise Inventory is from the beginning of the period. • The amount of Merchandise on hand changes all the time. These changes are recorded in the Purchases and Sales accounts not Merchandise Inventory. • The ending inventory is determined with a physical inventory count of what is on hand and an adjustment is made to correct the amount • The amount of the ending Merchandise Inventory becomes the beginning Merchandise Inventory for the next period.

Calculating the Adjustment for Merchandise Inventory • When calculating the adjustment for Merchandise Inventory, you need to know 1) the Merchandise Inventory account balance and 2) the physical inventory amount: • Account balance $84,921 • Physical Inventory $81,385 • The amount at the end of the period is less than beginning inventory so you know the account needs to be decreased. • Merchandise Inventory is an asset account so is decreased with a credit. • Merchandise Inventory adjustments are offset to the Income Summary account. Pg 521-522

Adjustments are marked with (a), (b), (c), and (d) so that anyone looking at the worksheet can see which debits and credits go together. Pg 522

Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax • These expenses represent a large cost to businesses and must be expensed so that businesses can use the information to make good decisions. • Supplies (pencils, pens, computer paper, shopping bags, sales slips, price tags, cash register tape) can amount to a lot when all added together. As we purchase supplies we add to the asset account but we do not take away every time we use a pen or replace the copy paper. • Prepaid Insurance must be adjusted for the portion that has been used up between its purchase and the end of the period. • Federal Income Tax is the tax the business is required to pay on its profits (net income) • Each year, the accountant predicts (estimates) what they think the income of the business will be for the year and makes quarterly payments of the taxes that will be due. • At the end of the year, the actual amount is calculated. If the business has over paid, they will get a refund, if they have under paid they will have to pay the difference. Pg 524-527

Completing the Worksheet • After the adjustments have been entered in the adjustments section of the work sheet, you must prove that debits and credits are still equal by proving and ruling the adjustment columns • Then all totals and adjusted totals should be extended to the Adjusted Trial Balance • The Adjusted Trial Balance should be proved and ruled Pgs 529-531

Journalizing and Posting the Adjusting Entries • Adjusting Entries – the journal entries that update the general ledger accounts at the end of the period. • The source for the adjusting entries is the worksheet • Begin the adjustment section of the journal by writing the words Adjusting Entries in the Description Line • Journalize the entries in the order they are listed alphabetically on the worksheet Pg 531-534

Posting Adjusted Entries Pg 535