Download

1 / 53

530 likes | 692 Views

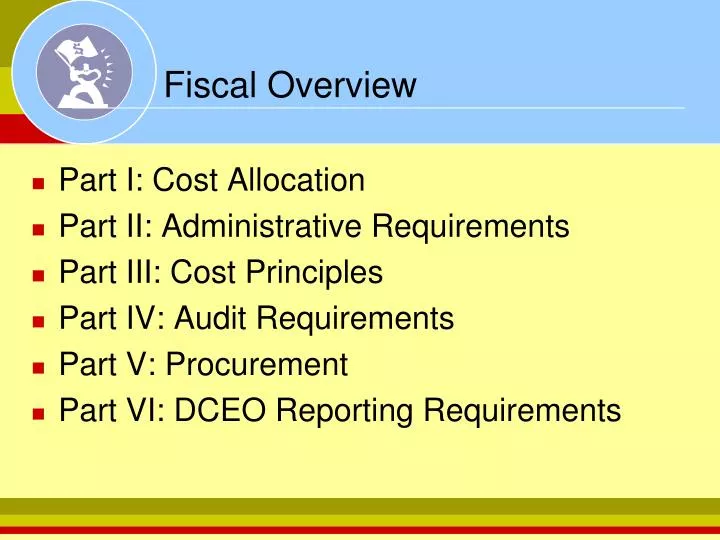

Fiscal Overview. Part I: Cost Allocation Part II: Administrative Requirements Part III: Cost Principles Part IV: Audit Requirements Part V: Procurement Part VI: DCEO Reporting Requirements. Federal Regulations. Part I: Cost Allocation & Time Distribution. . Cost Allocation.

E N D

Fiscal Overview • Part I: Cost Allocation • Part II: Administrative Requirements • Part III: Cost Principles • Part IV: Audit Requirements • Part V: Procurement • Part VI: DCEO Reporting Requirements

.Cost Allocation • The process used to distribute costs to a final cost objective based on benefits received Costs Direct Shared Indirect

Federal Guidance • OMB Circular A-87 • OMB Circular A-122 • OMB Circular A-21 • 48 CFR Part 31 • 45 CFR Part 74, Appendix E • Guidance on direct and indirect costs

Treatment of Costs • Direct charge whenever possible • Consistent treatment • In accounting system • Over time • Measuring benefit • Benefit determines allocation

Types of Costs • Direct • Single cost objective • Shared • Multiple cost objectives, or • Multiple fund sources • Indirect • Overhead

What are Direct Costs? • Those costs that can be readily identified with a particular cost objective. Examples (program specific): • Salaries • Space • Supplies • Communications

What are Indirect Costs? • Those costs that are not readily identifiable with a particular cost objective Examples: • Salaries • Space • Supplies • Telecommunications • Management & overhead

Cost Objectives • Intermediate • Cost pools or cost centers • Final • Funding source • Cost category

Allocation Bases • Keep in mind • Fair basis & equitable to all fund sources • Minimal distortion • Actual costs only (Can’t Charge $80k for Program Director’s Salary if he is paid $50k) • General acceptability • Timely management control • Materiality, cost, and practicality of use • Controllable • Direct relationship to costs

What is a Cost Allocation Plan?(CAP) • A document that identifies, accumulates, and distributes allowable direct and indirect costs and declares the allocation methods used for distribution. Federally approved Cost Allocation Plan

Cost Allocation Plans • Must be: • In writing • Include a process for reconciliation and adjustment • Periodically validated and updated

Benefits of a CAP • Management tool • Equitable sharing of costs • Establishes financial management standards • Meets cost principles and standards • Eliminates arbitrary methods of charging costs • Standardizes financial practices

Types of CAPs • Indirect cost plan • Addressed in OMB Cost Circulars • Federal agency approval required • Need Letter from federal cognizant agency • Rate should not be applied against direct costs that require little administrative involvement (e.g., ITAs, large subcontract amounts). Refer to letter. • Includes an indirect cost rate • CAP of the organization • Shared indirect costs • Awarding agency approval

Indirect Costs • Allowable to the extent • Contained in a Cost Allocation Plan • Identify as a separate cost pool & allocated to programs based on equitable benefit • Approved by cognizant Federal Agency, if required • Must be within Administrative Cost limitations • Generally overhead costs of organization • Can not include unallowable costs such as fundraising

Time Distribution • System that distributes staff salaries & benefits • Based on staff time spent on certain activities, projects, and grants • Needed if staff work on multiple projects/fund sources • Ensure sufficient activity/project codes to cover all funding sources

Time Distribution • System must: • Account for 100% of staff time • Allocate only time that is being paid • Should be completed by staff at least on a monthly basis and approved by a supervisor • Actual allocation of costs should be traceable to staff time activity report • Time & Attendance Records (Personnel Activity Reports) • Use also for allocating non-personnel costs

Common Compliance Findings • No written cost allocation plan or approved indirect cost rate in place • Direct charging of all staff time to one program when individuals were working on multiple programs • Costs related to an approved indirect cost rate exceeded the allowable administrative cost limitation for a program

Common Compliance Findings • Costs were allocated based on funding projections • Allocation bases used by staff were not consistent with the bases and cost pools described in the agency’s cost allocation plan • Costs were allocated every six months rather than on a monthly or quarterly basis

Part II: Uniform Administrative Requirements & Financial Management Standards

Applicable Federal Administrative Requirements • Non-Profits and Institutions of Higher Education must comply with the administrative requirements at 29 CFR Part 95.

All Financial SystemsMust Adhere to 7 separate standards • 1. Financial reporting • System must permit preparation of Federal financial reports • Must report accruals • 2. Accounting records • Adequately identify grant funds • Awards, obligations, assets, liabilities, income, and expenditures (Fund Accounting) • Supported by source documentation • Must be maintained in accordance with GAAP

More Financial Standards • 5. Allowable costs • Only allowable costs charged • 6. Source documentation • Costs must trace to authorizing document • Proof that costs are allowable & allocable • 7. Cash management • System to control cash assets

Internal Control System (ICS)What is it? • The process used by an agency to safeguard its assets, check the accuracy and reliability of its accounting data, promote operational efficiency, and encourage adherence to management’s policies.

Internal Control System (ICS)How to monitor the ICS? • Interview, review, and test: • Segregation of duties • Authorization, execution and payment • Competent personnel • Integrity, training, and supervision • Access to assets is limited • Records are periodically compared to existing assets • Authorized transactions are recorded in a timely manner

Financial & Administrative Procedures • Formalize procedures in writing • Distribute to all appropriate staff • Include at a minimum the following policies: • Payroll • References to Applicable Federal Regulations • Financial Reporting • Purchasing/Procurement • Cash Management • Cost Allocation Plan or Policies • Property Management • Audit • Travel • Bonding • Petty Cash • Payment Approval/Cash Disbursements • Cost Classification • Bank Reconciliations • Posting to Books of Account

Property Management • Equipment records shall be maintained accurately and shall include the following information: • (i) A description of the equipment. • (ii) Manufacturer's serial number, model number, Federal stock number, national stock number, or other identification number. • (iii) Source of the equipment, including the award number. • (iv) Whether title vests in the recipient or the Federal Government. • (v) Acquisition date (or date received, if the equipment was furnished by the Federal Government) and cost. • (vi) Information from which one can calculate the percentage of Federal participation in the cost of the equipment (not applicable to equipment furnished by the Federal Government). • (vii) Location and condition of the equipment and the date the information was reported. • (viii) Unit acquisition cost. (ix) Ultimate disposition data, including date of disposal and sales price. A physical inventory of equipment shall be taken and the results reconciled with the equipment records at least once every two years.

Federal Cost Principles • Purpose – provides that the Federal government bears its fair share of costs except where restricted or prohibited by law • Reasonable & Necessary • “Prudent Person Rule” • Arm’s Length Transaction • Allocable • Clearly benefit program • Both direct & indirect costs

Factors Affecting Allowability of Costs • Authorized or not prohibited • Consistent with the Federal Rules & Circulars • Consistent treatment • Across time & program lines • Not used as match • Unless specifically authorized

Allowability • Documented • Traceable to source documentation • Consistent with GAAP • Accounting standards & treatment • Conform to limitations/exclusions contained in the cost principles • Net of applicable credits

Allowable Costs Examples • Payroll • Salary & bonus limitations • ETA funded programs per TEGL5-06 per Public Law 109-234 • Requires documentation supporting time distribution • Travel • Training • Audit

Costs Allowable With ConditionsExamples • Advertising/Public Relations • Solely for public relations of organization – unallowed. • RFP & promotion of program/grant – allowable • Capital Assets • Purchase of land or buildings – unallowed • Equipment – allowable (w/ prior approval)

Unallowable CostsEXAMPLES • Entertainment • Allowable for certain WIAYouth recreation activities • Lobbying • Losses, fines & penalties • Alcoholic Beverages • Contingency reserves • Employment Generating/Economic Development Activities • Donations and contributions • Goodwill

Audit Requirements • Grant Agreement: Audited Financial Statements • OMB Circular A-133: A Single Audit is required when an Entity expends more than $500,000 or more in federal funds in a fiscal year.

ApplicabilityWho is required to have a Single Audit? • States, local governments, and non-profit organizations that are direct grant recipients & sub recipients of Federal funds • Commercial organizations that expend $500,000 or more and are a sub recipient under WIA Title I must adhere to OMB Circular A-133 Audit Requirements • WIA Regulations at 20 CFR 667.200

Part V: Procurement & Contracting 29 CFR 97.36 29 CFR 95.40-48 WIA Regulations

Procurement Requirements • Minimum requirements • Written procurement/purchasing procedures • Written code of conduct & conflict of interest policies • Procedures to review procurements • Cost price analysis (determination of needs, costs, estimates, etc.) • Demonstrated ability to perform • Close-out & protest process of contracts (records, settlement, etc.)

Partners? • Identifying partner organizations in your grant proposal and agreement DOES NOT PRECLUDE you from abiding by Federal procurement procedures • All services and goods within your grant agreement ARE SUBJECT to procurement • Grantees need to use FULL & OPEN COMPETITION when contracting with partners • EXCEPTION: In accordance with TEGL 14-08, procurement is not required for ARRA-funded contracts with institutions of higher education, such as community colleges, and other eligible training providers

Procurement Methods 1. Small purchase - INFORMAL 2. Sealed bids – FORMAL (technical specifications & price) 3. Competitive proposals – FORMAL (request for proposals) 4. Non-competitive proposals – sole source or limited competition

Small Purchase • Informal method for easily purchased items • Example: office supplies, equipment, etc. • Price is the factor (ONLY FACTOR) • Easily quoted, standardized product, no performance, etc. • Threshold limit – commonly seen from $500 to $5,000 – establish a limit suitable for your agency • Minimum of three (3) quotes DOCUMENTED

Sealed Bids • Publicly solicited bids • Awarded to lowest price bid (ONLY FACTOR) • Technical specifications spelled out in solicitation • At least two responsive bidders • Procurement based SOLELY ON PRICE • Publicly opened, evaluation, selection, award • Rejected bidders have documented reasons • Maintain procurement file on each solicitation • IF YOU DO NOT HAVE A SMALL PURCHASE LIMIT – ALL PROCUREMENTS UNDER $100,000 MUST BE DONE BY SEALED BIDS!!!!!

Competitive Proposals • Performance & delivery are critical factors; • Public request for services or goods being needed; • Evaluation factors determine best proposal (weighting); • Tell us how services will be delivered; • Requires a Cost & Price Analysis and/or Lease vs. Purchase Analysis • Fixed price or cost reimbursement contract

Non-Competitive Proposals • SOLE SOURCE • No responses from RFPs issued (more than once) • Public emergency or delay • Reason must be fully documented & approved by Directors/Board • Cost/Price analysis is required • Profit is negotiated separately • Last resort for procurement of goods & services • Will be reviewed during monitoring by DOL • USE CAUTION – may need the awarding agency or state approval

Welcome Package Reports Deliverable Schedule • Project Status Report – 30 days after the end of each calendar quarter • Financial Status Report – 30 days after the end of each calendar quarter • Final Financial Status Report – 45 days after grant end date • Audits – 9 months after grantee’s fiscal year-end • ARRA Section 1512 Report – 5 days after end of each calendar quarter

Status Reports • Status Report Templates and Instructions can be found on DCEO website http://www.ildceo.net/dceo/Bureaus/Office+of+Accountability/Reporting/

Financial Status Report • Report Grant Expenditures (including Accruals), Match, Grant Funds Received, and Grant Income • Supporting Documentation (i.e., Trial Balance) must be provided • Must be signed by Authorized Signatory named in Grant Agreement