Download

1 / 38

440 likes | 850 Views

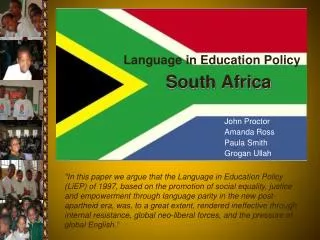

BDO SOUTH AFRICA. Roxanna Nyiri Tax Director BDO South Africa. Independent 3 rd Parties. JPS Group Case Study. Royalty. ??? – Owns Intellectual Property. JPS South Africa Manufacturer. Investment. Product. JPS Mauritius JPS Botswana JPS Uganda JPS Zambia.

E N D

BDO SOUTH AFRICA Roxanna Nyiri Tax Director BDO South Africa Independent 3rd Parties

JPS Group Case Study Royalty ??? – Owns Intellectual Property JPS South Africa Manufacturer Investment Product JPS Mauritius JPS Botswana JPS Uganda JPS Zambia ??? - Headquarter Company location Export Raw Materials Distribution Independent 3rd Parties Facing the Challenges of Doing Business in Africa

International Tax Planning Objectives • To divert, extract and distribute profits out of high tax paying jurisdictions • Ensure that connecting factors i.e. residence/presence do not arise in high tax paying jurisdictions • Avoid double tax • Minimise global tax liability Facing the Challenges of Doing Business in Africa

JPS Example • High Tax • South Africa 28%Contract Manufacturer / Agent • Returns Zambia 35% Uganda 30% Risk Low Tax Mauritius 15% Fully Fledged manufacturer Centralised Services Returns Tax incentive co 3% Distributor Intangibles Risk Botswana 15% - 22% Facing the Challenges of Doing Business in Africa

International Tax issues in SA • Substance over form • Source/deemed source • Section 9D • Residence • Section 31 • DTA effects • General anti avoidance Facing the Challenges of Doing Business in Africa

SUBSTANCE OVER FORM • Is there substance to the offshore entities or are they merely post box companies? • Are there premises, resources, employees and capital infrastructure in the offshore entities? Facing the Challenges of Doing Business in Africa

Source/deemed source • Prior to 2001 SA has applied a source basis of taxation • Originating cause of the income • Location of the originating cause • Residence basis of taxation after 2001 Facing the Challenges of Doing Business in Africa

RESIDENCE • Are any of the offshore entities SA resident? • Is the juristic person incorporated, established or formed in the Republic? • Does the juristic person have its place of effective management in South Africa? • Tie breaker rule in the Double Tax Agreement (‘DTA’) Facing the Challenges of Doing Business in Africa

Section 9D-Controlled Foreign Company legislation • Determine whether the taxpayer is a resident/non resident Is the entity incorporated, established or formed in the Republic? No Yes POEM in SA? Yes No Resident Non resident Facing the Challenges of Doing Business in Africa

Section 9D-Controlled Foreign Company legislation Does the resident (s) individually or jointly, directly or indirectly, hold more than 50% of the participation rights or are more than 50% of the voting rights in that company directly or indirectly exercisable by one or more persons that are resident other than persons that are headquarter companies? Yes No Not a CFC Is a CFC, subject to certain exclusions Include proportional amount of net income in residents income No income included Facing the Challenges of Doing Business in Africa

Section 9D-Controlled Foreign Company legislation • Exemptions: • The business establishment exemption • Net income of CFC included in SA taxable income • Foreign dividend income • Interest, royalties, rental and similar income Facing the Challenges of Doing Business in Africa

Headquarter Companies • A definition of ‘headquarter company’ is added into S1 of the Act, with effect from 1 January 2011 • The aim is to make South Africa attractive as the jurisdiction to hold investments in African countries • The definition is fairly complex but the main features are as follows: Facing the Challenges of Doing Business in Africa

Headquarter Companies • The company must be a resident • Minimum participation by shareholders • Each shareholder must hold at least 20% of the equity shares in the holding company throughout current year of assessment and all previous years Facing the Challenges of Doing Business in Africa

Headquarter Companies • 80-20 Tax Value • Eighty percent of the tax value of the holding company must represent investment in foreign subs in which the holding company holds at least 20% of the equity shares throughout the current year of assessment and all previous years Facing the Challenges of Doing Business in Africa

Headquarter Companies • The company must be a resident (cont…) • 80-20 Receipts and Accruals • Eighty percent of total receipts and accruals of the holding company must be derived from foreign subsidiaries Facing the Challenges of Doing Business in Africa

Headquarter Companies • Qualifying Headquarter Companies become eligible for tax relief • Foreign subsidiaries not treated as CFC’s • Dividends declared by Holding Companies exempt from STC and not subject to new dividends tax • Holding Companies not in violation of thin capitalization rules because of back-to-back cross-border loans Facing the Challenges of Doing Business in Africa

Transfer PricingWhy Transfer Pricing legislation? • Reduction in customs duty rates • Relaxation of exchange controls • The OECD • Section 31 and Practice Note 7 Facing the Challenges of Doing Business in Africa

Transfer Pricing Legislation – Requirements • Goods and/or services • Supplied or acquired • International agreement • Connected person • Price of goods and/or services not at arm’s length Facing the Challenges of Doing Business in Africa

Transfer Pricing Legislation Amendments • The South African transfer pricing rules have been modernised in line with international practice. • The focus on goods and services has been revised. The revised trigger is based on transactions, operations and schemesthat have been effected or undertaken for the benefit of connected persons with a cross-border nexus. Facing the Challenges of Doing Business in Africa

Transfer Pricing LegislationAmendments • Under these conditions, the SARS may impose transfer pricing adjustments if: • Terms and conditions are made or imposed in the transactions, operations or schemes that differ from the terms and conditions that would have existed between independent persons acting at arms length, and • The difference confers a South African tax benefit for one of the parties Facing the Challenges of Doing Business in Africa

Transfer Pricing Legislation Amendments • SARS has the power to adjust the terms and conditions of the transaction, operation, or scheme to reflect the terms and conditions that would have existed at arm’s length. • These adjustments can accordingly be taken into account in the determination of taxable income of the parties to the transaction, operation or scheme. Facing the Challenges of Doing Business in Africa

Transfer Pricing LegislationAmendments • Insertions in section 31 effective1 October 2011 • Any transaction, operation, scheme agreement or understanding directly or indirectly entered into or effected between a resident and a non resident connected persons for the benefit of either or both Facing the Challenges of Doing Business in Africa

Transfer Pricing LegislationAmendments • Any term or condition of that transaction, scheme, agreement or understanding is different from any term or condition that would have existed had those persons been independent parties transacting at arms length and will result in a tax benefit of either party Facing the Challenges of Doing Business in Africa

Transfer Pricing LegislationAmendments • Insertions in section 31 effective 1 October 2011 (Cont…) • The taxable income must be calculated as if that transaction were entered into on the terms and conditions that would have existed had the transaction been entered into between independent parties at arm’s length Facing the Challenges of Doing Business in Africa

Transfer Pricing LegislationAmendments • Inbound and outbound financial assistance pertaining to headquarter companies is specifically excluded from transfer pricing provisions • Thin capitalisation has been incorporated into the transfer pricing provisions Facing the Challenges of Doing Business in Africa

Transfer of goods and /or services • Examples of ‘affected transactions’ • Low interest/Interest free loans/guarantees • Services: management fees, admin fees, technical fees • Royalties/license fees • Transfer of goods in/out Facing the Challenges of Doing Business in Africa

Will the investment into offshore entities be in the form of debt financing? • Rate of interest is required to be a market rate of interest • The rate of interest the borrower would have incurred had borrowed from an independent third party • Must look at all the terms of an intra-group loan • OECD ‘independent lender test’ • Whether debt is to be regarded as a loan or equity Facing the Challenges of Doing Business in Africa

Will the investment into offshore entities be in the form of equity? • Foreign dividends are taxable in SA subject to certain exemptions: • Profits taxed in SA • Listed companies • The CFC exemption • The 20% shareholding exemption Facing the Challenges of Doing Business in Africa

Intangibles INTANGIBLES • What are intangibles? • Manufacturing: • Patents • Processes • Designs • Formulae • Quality control systems Facing the Challenges of Doing Business in Africa

Intangibles INTANGIBLES • Marketing: • Trade names • Trademarks • Advertising formats Facing the Challenges of Doing Business in Africa

Intangibles INTANGIBLES • Calculation of an arm’s length price • CUP method • Residual profit split method • Determine routine profit of performing functions, assuming risks and using assets • Allocate residual profit based on share of R&D costs • Withholding tax on royalties Facing the Challenges of Doing Business in Africa

DOUBLE TAX AGREEMENTS (‘DTA’) DOUBLE TAX AGREEMENTS (‘DTA’) • Article 7 Business Profits • Article 10 Dividends • Article 11 Interest • Article 12 Royalties • Article 15 Income from Employment • Article 25 Mutual Agreement Procedure • Article 26 Exchange of information Facing the Challenges of Doing Business in Africa

Transfer pricing of branch operations Transfer pricing of branch operations • Branches are not a separate legal entity • Transfer pricing provisions of s 31 not applicable • Treaty provisions – attribution of profits to a permanent establishment • Practice Note 7 Facing the Challenges of Doing Business in Africa

Interaction with tax treaties Interaction with tax treaties • Treaty must be in place • Article 5 par 2 of Treaty – PE • Article 7 par 1 and 2 of Treaty – Business Profits • Article 7 par 3 - Expenditure Facing the Challenges of Doing Business in Africa

Foreign Investments by SA Corporate APPLICATIONS RELATING TO CAPITAL TRANSACTIONS OF SA COMPANIES • Investments exceeding R500 million per applicant per calendar year require prior approval from the Financial Surveillance Department • In terms of current policy at least 10 per cent of the foreign target entity’s voting rights must be obtained and the proposed investment must be in the same line of business as that of the applicant company • South African owned Intellectual Property may not be transferred by way of a sale, assignment or cession and/or the waiver of rights in favour of non-residents in whatever form, directly or indirectly without the prior approval of the Financial Surveillance Department Facing the Challenges of Doing Business in Africa

APPLICATIONS RELATING TO CAPITAL TRANSACTIONS OF SA COMPANIES Foreign Investments by SA Corporate • Critical information to be submitted: • Business plan of the applicant • Full details of longer term monetary benefits (cashflow forecast) to be derived by the Republic • Pro-form Balance Sheet of offshore entity (before & after financial position) • Percentage equity to be acquired in the foreign target company as well as the percentage voting rights to be acquired Facing the Challenges of Doing Business in Africa Page 36

Foreign Investments by SA Corporate • Names and domicile of the shareholders • Proposed financial structure of entity to be acquired or to established • (issued share capital) • (loan funds) • (Guarantees to be issued from Republic) • (credit facilities abroad) • (amounts involved) • Manner in which the funds required will be employed; and • Estimate of annual running expenses of offshore entity Facing the Challenges of Doing Business in Africa

THANK YOU Facing the Challenges of Doing Business in Africa