Download

1 / 19

250 likes | 540 Views

Chapter 3 Job Costing, Process Costing, & Operations Costing. ©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. Job Costing.

E N D

Chapter 3Job Costing, Process Costing, & Operations Costing ©2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

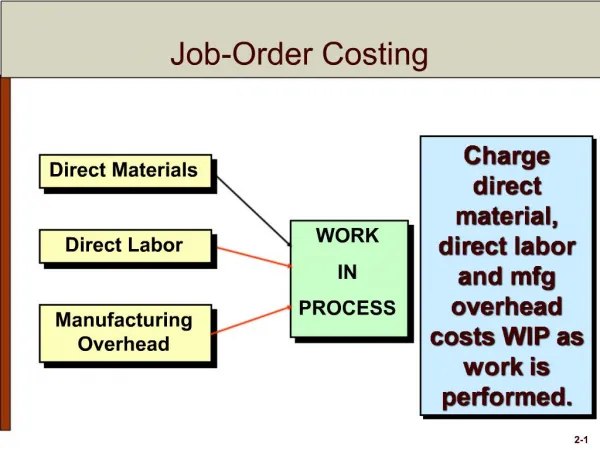

Job Costing Companies that manufacture customized products or provide customized services to clients use a costing system called job costing, which accumulates, tracks, and assigns costs for each job. EXAMPLES Builder of custom homes A CPA firm A Hospital

Process Costing Companies that produce a homogeneous product on a continuous basis use process costing to accumulate, track, and assign costs to products. EXAMPLES Oil Refineries Paint Manufacturers Beverage Manufacturers

Operations Costing Operations costing is a hybrid of job and process costing, for companies that make large numbers of products that are standardized within a batch. EXAMPLES Clothing Manufacturers Automobile Manufacturers Footwear Manufacturers

Measuring and Tracking Direct Labor Wage Rate Number of Hours = X Direct Labor Wage Rates must include the cost of FringeBenefits,such as employer’s cost for health, dental and other insurance, retirement plans, employer portion of social security tax and state and federal unemployment taxes (often 30-35%of the base wage).

Manufacturing Overhead • The most difficult cost to track and assign to products • Indirect in nature • Made up of many unrelated costs

Cost Drivers and the Overhead Rate The choice of cost driver depends on the specific company and the processes it uses to manufacture products and provide services to customers. Manufacturing Overhead Cost Driver Overhead Rate =

The Use of Estimates Since the actual amount of many overhead items will not be known until the end of a period (when an invoice is received), companies often estimate the amount of overhead that will be incurred in the coming period. What are the benefits of estimates? Normalizes fluctuations Helps with production decisions. Allows firms to set prices

Predetermined Overhead Rate Estimated Overhead for the Cost Pool Estimated Units of the Cost Driver Predetermined Overhead Rate (for a Cost Pool) = Predetermined overhead rates are typically calculated using annual estimates of overhead and cost drivers.

Over- and Underapplied Overhead • Because overhead is applied to products using predetermined overhead rates based on estimates, it is likely that actual overhead costs (when they become known) will differ from those applied.

Basic Process Costing • Tracked by department & assigned evenly as products pass through • Tracked by department & assigned evenly as products pass through To ignore product safety??

Equivalent Units • Equivalent units are: • The number of finished units that can be made from the material, labor, and overhead included in partially completed units • For example: • 2,000 units that are 50% complete are equivalent to 1,000 finished units (or 2,000 x 50%)

Four Steps in Process Costing When a company has both beginning and ending inventories of WIP, process costing becomes more complicated and must be addressed in four steps. As such, equivalent units of production can be calculated in two different ways—the first-in, first-out (FIFO) method or the weighted average method.

Equivalent Units – FIFO Method In the FIFO method: The equivalent units and unit costs for the current period relate only to the work done and the costs incurred in the current period.

Equivalent Units - Weighted Average Method In the Weighted Average method: The units and costs from the current period are combined with the units and costs from last period in the calculation of equivalent units and unit costs.

Service Department Cost Allocation Large organizations have both production and service departments. Production departments are involved in the direct manufacture of a product/service to external customers. Service departments provide services to internal departments within the company. Allocating service department costs to production is a first step in the overall product costing process.