Download

1 / 32

320 likes | 453 Views

Federal Income Tax Update. Central Illinois Chapter Meeting April 25, 2019 Bloomington, IL. Thomas F. Wheeland BKD, LLP – St. Louis. Impact of TCJA – A Recap. 1. 2. 3. Our goals for today. What We Have Seen. What We Don’t Know. TCJA Provisions

E N D

Federal Income Tax Update Central Illinois Chapter Meeting April 25, 2019 Bloomington, IL Thomas F. Wheeland BKD, LLP – St. Louis

Impact of TCJA – A Recap 1 2 3 Our goals for today What We Have Seen What We Don’t Know

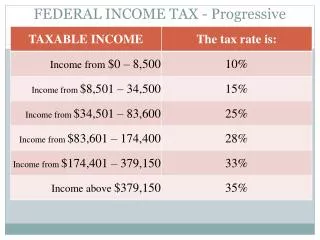

TCJA Provisions • Reduction in Federal Corporate Income Tax Rate to 21% • Repeal of Alternative Minimum Tax (AMT) • AMT Credit Utilization and Refund • Net Operating Losses (NOLs) • Unlimited Carryforward • No Carrybacks • Limited to 80% of Regular Taxable Income • P&C Company NOL Rules Unchanged • Capital Loss Rules Unchanged GENERAL CORPORATE PROVISIONS

Utilization of Existing AMT Credits • Use AMT Credits to Offset Regular Tax • Excess Credits are Refundable (over an established period) • 50% of Excess Refundable in 2018-2020 • 100% of Excess Refundable in 2021 • Classification to Income Taxes Recoverable vs. DTAnow disclosed in Annual Statement Tax Footnote Amt credits

AMT Credit Example $100,000 AMT Credit Carryforward as of 12/31/17 Calculation: $40,000 2018 Regular Tax ( 40,000) AMT Credit Offset Against Regular Tax $ 0 Subtotal ($30,000) 50% of Remaining AMT Credit Allowed as a Refundable Credit - Refund Shown on 2018 Tax Return $30,000 AMT Credit Carryforward as of 12/31/18 Amt credits

AMT Credit Example $100,000 AMT Credit Carryforward as of 12/31/17 Calculation: $ 0 2018 Regular Tax ( 0) AMT Credit Offset Against Regular Tax $ 0 Subtotal ($50,000) 50% of Remaining AMT Credit Allowed as a Refundable Credit - Refund Shown on 2018 Tax Return $0 Regular Tax in 2019 and 2020 would yield refunds of $25,000 & $12,500, respectively, with $12,500 balance refunded in 2021 Amt credits

Net Operating Losses (NOLs) • Conforms Life Operations Loss Deduction (OLD) Rules to NOLs • No Carryback of NOLs • Indefinite Carryforward • Annual Limitation of 80% of Regular Taxable Income for Post-2017 NOLs • P&CNOLs Unchanged • 2 Year Carryback • 20 Year Carryforward • 100% Offset of Regular Taxable Income • Capital Loss Carryback and Carryforward Rules Unchanged Net operating losses

Nol comparison chart Pre and Post TCJA

TCJA Provisions • 100% Bonus Depreciation & Expanded §179 Expensing • Limitation on Deductibility of Business Interest • Income Inclusion Rule • Reduction in Dividends Received Deduction • Meals & Entertainment Limitations • Qualified Transportation Fringe Limitations • Step One Disallowance for Reserved Employee Spots • Step Two Primary Use of Remaining Spots • Step Three Allowance for Reserved Non-Employee Spots • Step Four Remaining Use and Allocable Expenses GENERAL CORPORATE PROVISIONS

Accelerated Tax Depreciation • Bonus Depreciation • Increased to 100% for Assets Placed in Service After September 27, 2017 and Before January 1, 2023 • §179 Expensing • Expanded to $1 million (from $500K) with Phase-Out Beginning at $2.5 million (from $2 million) • Property Placed in Service After December 31, 2017 Fixed asset expensing

Parking Example • Facts: Taxpayer has 500 total parking spots used by visitors and employees, 50 of which are reserved for management. During normal business hours, 400 employees park in the non-reserved spots. Also, there are 10 reserved spots (included in the 500) for visitors. Expenses for the parking lot total $10,000. • Step One – The reserved management spots result in $1,000 [$10,000 * 50/500] of non-deductible expenses (or $1,000 of UBTI) • Step Two – The primary use of the remainder (400/450) is not for use of the general public (>50%) • Step Three – The visitor spots (10/450) result in roughly 2% of the expenses ($200) NOT subject to disallowance • Step Four – Taxpayer reasonably determines that $7,822 of the remaining $8,800 is subject to disallowance (400/450) SEE IRS Notice 2018-99

Non-Deductible Expenses • Meals & Entertainment • No Deduction for Entertainment Expenses • Notice 2018-76 clarifies deductibility of certain business meals • All Meals Subject to 50% Disallowance • Ordinary & necessary • Not lavish or extravagant • Taxpayer or employee present • Provided to current or prospective clients • If during an entertainment activity, food and beverage cost must be separately billed or stated Update on certain non-deductible expenses

Other Items of Note • Year of Inclusion • Income Inclusion - No Later than Inclusion for Financial Reporting Purposes • Some Exceptions • Per Notice 2018-80, market discount is excluded • Questionable Application to Accrued Dividends • §174 Amortization of Research & Experimentation Expenses • 5 Year Amortization Period • For Expenses Incurred After 12/31/21 • No Change to R&E Credit Additional tCJA Provisions

Other Items of Note • Limitation on Business Interest Expense • Limits net business interest expense • 30% of adjusted taxable income • Excess carried forward • Insurance company interest income is included in “business interest income” for purposes of IRC §163(j) per Notice 2018-28 Additional tCJA Provisions

TCJA Provisions • Loss Reserves • Changes in Interest Rate and Payment Pattern – Generally Reduced Tax Loss Reserves • No Company Election • Repeal of §847 • Proration Percentage Increased from 15% to 25% • Keeps the After-Tax Yield of Tax-Exempt Bonds Constant at 5.25% • Narrows the Spread Between Taxable and Tax-Exempt Bonds • Retention of NOL Rules (2 Back/20 Forward) Non-life company PROVISIONS

TCJA Provisions • §807(f) Changes Subject to §481 Rules • 4 Year Spread for Reserve Decreases • 1 Year Spread for Reserve Increases • DAC Capitalization • 2.09% for Annuities (formerly 1.75%) • 2.45% for Group Life (formerly 2.05%) • 9.2% for Other Contracts (formerly 7.7%) • DAC Amortization • Retains 60 Month Amortization • Increases 120-Month Amortization Period to 180 Months life company PROVISIONS

TCJA Provisions • Life Reserves Capped at Greater of Net Surrender Value or 92.81% of NAIC Prescribed Reserves (8 Year Phase-In) • 70% Company Share/30% Policyholder Share (6.3% ETR on Tax Exempt Interest) • Inclusion of Policyholder Surplus Account Balance in Income over 8 Years • NOL/OLD Conformity • Elimination of Small Life Insurance Company Deduction (SLICD) life company PROVISIONS

DRD Summary • Dividends Received Deduction • <20% Owned – 50% (vs. 70%) • P&CDRD (Net of Proration) • Old Law 14.175% ETR • New Law 13.125% ETR • Life Company (Net of P/H Share) • Old Law Varied • New Law 13.65% ETR • C Corporations • Old Law 10.5% ETR • New Law 10.5% ETR • ≥20% Owned – 65% (vs. 80%) Additional tCJA Provisions

Income Tax Accounting Impact • Impacts to the 2017 & 2018 Tax Provisions • Reduction in DTAs • Increase 2017 GAAP Effective Tax Rate (ETR) in P&L Regardless of Source • Increase 2017 SAP ETR in Surplus • 2018 impact of return-to-provision adjustment (as well as carrybacks to pre-TCJA years) • Increases in Current Taxes (Caused by Reserves and DAC) Increase Deductible Temporary Differences – Reversal Patterns are Key GAAP & SAP Reduction in Current Federal Taxes with Short-Term Impact of DTA Reduction

Income Tax Accounting Impact • Elimination of NOL Carryback for Ordinary DTAs of Life Companies • Removes a Source of Income for GAAP • Makes SSAP 101, ¶11.a., Effectively Moot • Make ¶11.b. difficult to apply • Year 2 and 3 reversals that create NOLs cannot be carried back to years 1 and 2 • Year 1 and 2 reversals that create NOLs are subject to 80% limitation when carried forward to years 2 and 3 • Adds complexity to ¶11.c. GAAP & SAP Complexity Created by Change in NOL Rules

Income Tax Accounting Impact • Assume ABC Insurance Company has $1,000,000 of pre-tax book income and $(100,000) of favorable permanent differences • “Book Taxable Income” [taxable income without regard to temporary differences] is $900,000 • At 21%, that generates $189,000 of tax and an effective tax rate (ETR) of 18.9% • ETR increases to 19.25% if pre-tax income is $1.2 million • ETR decreases to 18.375% if pre-tax income is $0.8 million • P&C companies with historic level tax-exempt investments are reporting ETRs in the 16%-18% rage • Life and health companies are more in the 19%-21% range (IMR skews impact for life companies) GAAP & SAP Effective Tax Rate Observations

The Big Five Reconciliation of Current Taxes Receivable/Payable Components of Deferred Tax Inventory Return-to-Provision Adjustment (RTP) Effective Tax Rate (ETR) Reconciliation Uncertain Tax Position (UTP) and Valuation Allowance (VA) Support Tax function key controls

What We Have Seen… • Items like Meals & Entertainment and Qualified Parking should be tempered by materiality • P&C companies are not running from tax-exempt investments and Life companies do not appear to be running towards them…perhaps it is a light stroll • On P&C side, reserve re-set was close to a push in 2018 provision calculations • Look for opportunities to carryback ordinary and/or capital losses to 2017 and prior years Bkd observations

What We Don’t Know… • Net Operating Losses • Assume C Corporation and P&C Company each have $1,000 of taxable income in carryback period • P&C company has tax loss of $(1,000) • Should result in full utilization • $210 tax refund • P&C company has tax loss of $(1,200) • The “entire amount” language of §172(b)(2) comes into play • Suggests $252 refund BKD OBSERVATIONS Net Operating Losses Unanswered questions in mixed group scenarios

What We Don’t Know… • Net Operating Losses • P&C company has tax loss of $(2,000) • The “entire amount” language of §172(b)(2) comes into play • Coupled with §172(e) for pre-TCJA years • Suggests $420 refund for pre-TCJA years and $378 (80% limitation for C corporation) for post-TCJA years BKD OBSERVATIONS Net Operating Losses Unanswered questions in mixed group scenarios

What We Don’t Know… • Alternative Minimum Tax • How will refundable AMT credit work in a §382 fact pattern? • Will P&C companies with NOLs in 2018 and/or 2019 be required to calculate an AMT NOL? • If a P&C insurer has an NOL in 2018 or 2019, and creates an AMT liability in the carryback period, how is the resulting credit refunded? BKD OBSERVATIONS Alternative Minimum Tax

Any Questions? Thomas F. Wheeland twheeland@bkd.com 314.802.0213 3