Download

1 / 47

470 likes | 626 Views

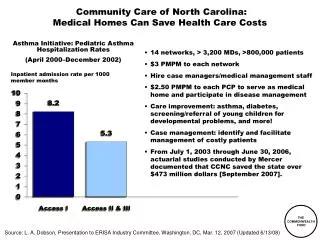

Community Care of North Carolina. Brief O verview of the Patient Protection and Affordable Care Act. Affordable Care Act Summary. The main provisions of the Affordable Care Act are : Requirements for insurance coverage Expanding Medicaid

E N D

Community Care of North Carolina Brief Overview of the Patient Protection and Affordable Care Act

Affordable Care Act Summary The main provisions of the Affordable Care Act are: • Requirements for insurance coverage • Expanding Medicaid • New coverage options through benefit exchanges, subsidized premiums • New health plan regulations • Cost reduction/quality improvement efforts • Changes in the tax code

Coverage Requirements Individual Mandate - US citizens without qualifying health coverage pay a tax penalty. $695 per year up to a maximum of $2,085 per family or 2.5% of household income. Gradually phased in through 2016, then increased annually by cost-of-living adjustment. Exemptions: financial hardship, religious objections, short-term lack of coverage, income under certain thresholds.

Coverage Requirements Employer Mandate • Businesses with 50 or more employees pay $2,000-3,000 fee for each employee uncovered or receiving a premium tax credit; first 30 employees exempt (2014). • Businesses with less than 50 employees exempt. • Business more with than 200 employees must automatically enroll employees in health insurance; employees can opt out.

Coverage Requirements SCOTUS Decision Penalties/mandates are constitutional. The penalties are taxes that fall under Congress’ general authority to levy taxes.

Medicaid Expansion • Expand Medicaid to all individuals under age 65 with incomes up to 133% FPL. • Feds fund decreasing portion of costs • 100% federal funding for 2014 through 2016 • 95% federal financing in 2017 • 94% federal financing in 2018 • 93% federal financing in 2019 • 90% federal financing for 2020 and thereafter

Medicaid Expansion States already covering adults with incomes up to 100% FPL will receive a phased-in increase in the federal medical assistance percentage (FMAP) States must maintain current income eligibility levels for children in Medicaid and the Children’s Health Insurance Program (CHIP) until 2019 and extend funding for CHIP through 2015. CHIP match rate increases in 2015.

Medicaid Expansion SCOTUS decision High court determined that federal government cannot make state match for all Medicaid programs contingent on participation in new expansion. Decision to expand will be on a state-by-state basis. NC’s approach has not yet been determined

New Coverages • American Health Benefit Exchanges / Small Business Health Options Program (SHOP) • State-based insurance exchanges for individuals and businesses with 100 or fewer employees • Restricted to US Citizens and legal immigrants • Exchanges administered by a governmental agency or non-profit • Office of Personnel Management to contract with insurers to offer at least two multi-state plans in each Exchange. • At least one plan must non-profit and at least one plan must not provide coverage for abortions

New Coverages • American Health Benefit Exchanges / Small Business Health Options Program (SHOP) • State-based insurance exchanges for individuals and businesses with 100 or fewer employees • Only US Citizens and legal immigrants; constraints on age-rating • Exchanges administered by a governmental agency or non-profit • Office of Personnel Management to contract with insurers to offer at least two multi-state plans in each Exchange. • At least one plan must non-profit and at least one plan must not provide coverage for abortions

New Coverages • Consumer Operated and Oriented Plan (CO-OP) • Non-profit, member-run health insurance companies in all 50 states and District of Columbia to offer qualified health plans • Feds to provide $4.8 billion to establish CO-OPs by July 1, 2013 • Can’t be an existing health insurer • Profits must be used to lower premiums, improve benefits, or improve the quality of health care delivered to its members.

Exchange Plans Bronze plan Minimum creditable coverage -“essential health benefits” -- Cover 60% of the benefit costs of the plan-- Out-of-pocket equal to HSA limits ($5,950 individuals / $11,900 families in 2010) Silver plan-- Cover 70% of the benefit costs of Gold plan-- Covers 80% of the benefit costs of the plan Platinum plan -- Covers 90% of the benefit costs of the plan

Exchange Catastrophic Plan • Available to individuals up age 30 and those exempt from the mandate • Coverage at the current HSA levels except that preventive exempt from deductible.

Requirements for Exchanges Consumer protections • Guaranteed issue/renewability • Limits variation allowable in rates for age, geographical location, family composition and tobacco use • Limits on out-of-pocket maximums based on income.

Requirements for Exchanges Maintain a customer service call center Establish procedures for enrollment and determining eligibility for tax credits. State must develop a single form for applying for state health subsidies online, in person, by mail or by phone. Submit financial reports to the Secretary and comply with oversight investigations

Requirements for Participating Health Plans Rules on marketing, adequacy of provider networks, contracts with “essential community providers,” uniformity of enrollment form, plan info. Require “navigators” for outreach and enrollment assistance Must be accredited Must report information on claims payment policies, enrollment, claims denials, cost-sharing requirements, out-of-network policies, and enrollee rights.

Basic Health Plan – Outside the Exchange States can create a Basic Health Plan for uninsured individuals with incomes between 133-200% FPL Offer an “essential health benefits” that covers at least 60% of the actuarial value of the benefits, limits annual cost-sharing to the current law HSA limits Limits on cost of plan to participants relative to HSA limits and what’s available in the Exchange.

Health plans: risk, rating and premiums • Establish a temporary national high-risk pool to provide health coverage to individuals with pre-existing medical conditions. • Require health plans to report Medical Loss Ratios (2010) and provide rebates to consumers (2011) if less than 85% for plans in the large group market and 80% for plans in the individual and small group • Establish a process for reviewing premium rates; require plans to justify increases. Allow states to merge individual and small group markets. (2014)

Health plans: coverage requirements • Provide dependent coverage for children up to age 26 for all individual and group policies. (2010) • Prohibit individual and group health plans from: • Placing lifetime limits on the dollar value of coverage • Rescinding coverage except in cases of fraud. • Establishing re-existing condition exclusions for children. • Guarantee issue, premium rating, and prohibitions on pre-existing exclusions in the individual, small group and Exchange markets. (2014)

Health plans: coverage requirements • New policies must meet 4 benefit categories. (2014) • Deductibles limited: $2,000 – individuals, $4,000 – families (2014) • Waiting periods limited to to 90 days. (2014) • Health insurers in individual and group markets fund temporary reinsurance program for high-risk individuals. ($25 billion over three years; 2014 through 2016).

Existing plans grandfathered • Existing plans need not comply with new benefit standards, but must extend dependent coverage for adult children up to age 26 and avoid rescissions of coverage. • Grandfathered plans must eliminate lifetime limits and pre-existing condition exclusions for children on phased-in basis.

Consumer Protection • Establish internet website to help residents identify health coverage options (2010) • Develop standard format for presenting on coverage options (2010) • Develop standards for providing information on benefits and coverage • State must establish an ombudsman program to serve as an advocate for people with private coverage

Other health plan provisions Option for health care choice compacts/national plans (2016). • Permit states to form health care choice compacts and allow insurers to sell policies in any state participating in the compact • Compacts must provide coverage at least as comprehensive and affordable that available through state Exchanges.

Cost and Quality Initiatives Administrative simplification • Simplify health insurance administration by adopting a single set of operating rules for eligibility verification and claims status; penalties for failing to comply. Quality improvement • Establish non-profit Patient-Centered Outcomes Research Institute to access clinical effectiveness of medical treatments(not mandates, guidelines, or recommendations for payment)

Cost and Quality Initiatives Fraud and Waste – Medicare and Medicaid • Conduct provider screening, enhanced oversight of new providers and suppliers, and enrollment moratoria in high-risk areas for fraud • Capture and share data across federal and state programs, increase penalties for submitting false claims, strengthen standards for community mental health centers and increase funding for anti-fraud activities

Cost and Quality Initiatives Prescription drugs - Medicare • Increase the Medicaid drug rebate percentage for brand name drugs • Authorize FDA to approve generic versions of biologic drugs after 12 years of exclusive use Tort reform • Five-year demonstration grants to states to develop alternatives to current tort litigation

Medicare Changes • Restructure payments to Medicare Advantage (MA) plans • Require Medicare Advantage plans to achieve medical loss ratio of at least 85% or remit payments • Freeze payments for some services and reduce part D subsidy for recipients above certain income levels. • Reduce the Medicare Part D premium subsidy for incomes above $85,000/individual and $170,000/couple.

Medicare Changes • Independent Payment Advisory Board to recommend strategies for reducing growth in Medicare spending. • Prohibit payments for services related to health care acquired conditions. (2011) • Reduce Medicare Disproportionate Share Hospital (DSH) payments (2014) • Allow ACOs that meet quality thresholds to share in cost savings.

Medicare Changes • Create CMS Innovation Center to test, evaluate, and expand methodologies that reduce program expenditures (2011) • Reduce Medicare payments to hospitals for preventable hospital readmissions. (2012) • Reduce Medicare payments to hospitals for hospital-acquired conditions (2015)

New Medicare Programs • National Medicare pilot – bundled payments for acute, inpatient hospital services, physician services, outpatient hospital services, and post-acute care services. (2013) Expand if effective (2016) • “Episode of care” begins three days prior to a hospitalization and spans 30 days following discharge. • Create Independence at Home demonstration program to provide high-need Medicare beneficiaries with primary care services in their homes (2012)

New Medicare Programs • Establish a hospital value-based purchasing program • Pay hospitals based on performance on quality measures • Extend the Medicare physician quality reporting initiative. (October 1, 2012) • Develop value-based purchasing programs for skilled nursing facilities, home health agencies, and ambulatory surgical centers. (Report 2011) • Provide 10% bonus payment to primary care physicians in Medicare (2011 through 2015)

Medicaid Changes • Create health homes for Medicaid enrollees with at chronic conditions or serious and persistent mental health condition. • Provide 90% match for two years for home health-related services, including care management, care coordination, and health promotion (2011) • Pilot bundled payments for hospitalizations (2012) • Allow pediatric ACOs to share in cost-savings (2012)

Medicaid Changes • Medicaid and CHIP Payment and Access Commission to include assessments of adult services • Increase Medicaid payments for primary care (family, general internal or pediatric) to 100% of Medicare payment rates for 2013 and 2014(100% fed match) • Duals - Create Federal Coordinated Health Care Office to integrate benefits and improve coordination between the feds and states (2010)

Strategy and Disclosure • Develop a national quality improvement strategy for health care services, outcomes, and population health. • Develop quality measures with input from multiple stakeholders (2011) • Require disclosure of financial relationships between physicians, hospitals, pharmacists, and manufacturers of drugs, devices and medical supplies. (2013) • Enhanced collection of data on race, ethnicity, sex, language, disability status, and for underserved rural and frontier populations.

Prevention Initiatives • Establish the National Prevention, Health Promotion and Public Health Council. • Create a Prevention and Public Health Fund • Create task forces on Preventive Services and Community Preventive Services to develop evidenced-based recommendations on prevention services. • Establish grant program to support the delivery of evidence-based and community-based prevention and wellness services in rural and frontier areas.

Prevention Coverage • Eliminate cost-sharing for Medicare covered preventive services; waive Medicare deductible for colorectal cancer screening tests. • Remove cost-sharing and increase federal match for preventive services and immunizations. (2013) • Authorize annual comprehensive health risk assessment. Reimburse 100% of the physician fee schedule amount with no deductible for services provided in outpatient setting. (2011)

Prevention Coverage • Require Medicaid coverage for tobacco cessation services for pregnant women. (2010) • Require qualified health plans to cover (without cost-sharing) specified preventive services for infants, children, and adolescents.

Wellness Programs • Grants for small employers to establish wellness programs. • Evaluate employer-based wellness programs through national survey of worksite programs • Permit employers to offer employees rewards (premium discounts, cost-sharing waivers, additional benefits) for participating in a wellness program • Require chain restaurants and vending machines to disclose nutritional content of products.

Long-term Care Changes • Establish CLASS program (insurance for community living assistance services and supports) with cash benefit averaging $50/day. • Extend the “Medicaid Money Follows the Person” Rebalancing Demonstration • Create new state options for home and community-based services through a Medicaid state plan • Establish the Community First Choice Option for community-based attendant supports for individuals with disabilities(enhanced federal match)

Long-term Care Changes • Require skilled nursing facilities under Medicare and nursing facilities under Medicaid to disclose information regarding • Ownership • Accountability requirements • Expenditures. • Publish standardized information on nursing facilities on web so Medicare enrollees can compare the facilities.

Other Investments • Reduce costs for Medicare beneficiaries : • $250 rebate to those in “doughnut hole” • Reduce coinsurance in doughnut hole from 100% to 25% (2020) • Require 50% discounts, federal subsidies on brand-name drugs for individuals in the doughnut hole (2013) • Provide 75% federal subsidy of generic drugs for individuals in the doughnut hole beginning (2011) • Reduce out-of-pocket requirements for qualifying for catastrophic coverage (2014 through 2019)

Other Investments • 10% bonus payment to primary care physicians, general surgeons practicing in health professional shortage areas (2011-2015) • Additional payments to qualifying hospitals in counties with the lowest quartile Medicare spending (2011 and 2012) • Require non-profit hospitals to conduct a community needs assessment every three years and: • Adopt an implementation strategy to meet the identified needs • Adopt and publicize availability of free or discounted care • Limit charges to patients who qualify for financial assistance and make reasonable attempts to determine eligibility for assistance before undertaking collection.

Workforce Improvements • Support for training programs for primary care models such as medical homes, team management of chronic disease, and integrated physical /mental health services. (2010) • Multi-stakeholder Workforce Advisory Committee to develop a national workforce strategy. • Increase the number of Graduate Medical Education (GME) training positions • Support training of health professionals through scholarships and loans for training of primary care professionals in medically underserved areas

Workforce Improvements • Support interdisciplinary behavioral health training programs and training for oral health professionals (2010) • Increased support for nursing training programs and loan repayment and retention grants for nurses

Tax Changes – Credits • Help individuals and families purchase coverage through the Exchanges through premium credits • Support on sliding scale for individuals earning100-400% FPL • Adjust subsidies over time based on premium cost and CPI • Provide cost sharing subsidies to reduce out-of-pocket costs for eligible individuals and families. • Provide eligible small employers with tax credits of 35 to 50% of cost of employees coverage (2010.) • Temporary reinsurance program for employers providing health insurance coverage to retirees over age 55 not eligible for Medicare. (2010)

Tax Changes – New Taxes • New tax on individuals lacking coverage: $695 per year up to a maximum of three times that amount or 2.5% of household income (2014) • Exclude OTC drugs from reimbursement under HSA or Archer Medical Savings Account. • Increase HSA/Archer tax penalty for non-medical disbursements • Limit contributions to flexible spending account to $2,500 (increased annual by COLA) • Increase the threshold for the itemized deduction for medical expenses from 7.5% to 10% of adjusted gross income

Tax Changes – New Taxes • Increase the Medicare Part A (hospital insurance) tax rate on wages for high-income taxpayers. • Impose an excise tax on health plans with aggregate values that exceed $10,200 for individual coverage and $27,500 for family coverage (indexed to CPI) • Eliminate the tax deduction for employers who receive Medicare Part D retiree drug subsidy payments. (2013) • Impose new fees on pharmaceutical manufacturers, health insurers, indoor tanning services and medical device manufacturers.