Download

1 / 55

550 likes | 623 Views

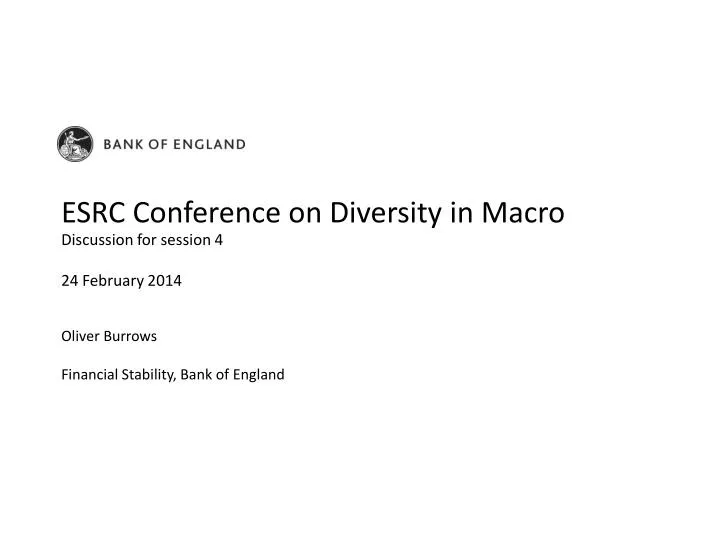

ESRC Conference on Diversity in Macro. Discussion for session 4 24 February 2014. Oliver Burrows Financial Stability, Bank of England. UK-resident banks’ sterling lending to UK residents, % of GDP. Credit by type: purchasing existing assets vs financing activity.

E N D

ESRC Conference on Diversity in Macro Discussion for session 4 24 February 2014 Oliver Burrows Financial Stability, Bank of England

UK-resident banks’ sterling lending to UK residents, % of GDP Credit by type: purchasing existing assets vs financing activity

UK-resident banks’ sterling lending to UK residents, % of GDP Credit by type: purchasing existing assets vs financing activity

The UK financial system, with cross-border inter-bank connections

The UK financial system, with cross-border inter-bank connections and derivatives

Growth of savings vs asset price inflation:insurance companies and pension funds

System-wide network effects / liquidity riskMonetary circuits MPC/FPC awayday on credit

System-wide network effects / liquidity riskMonetary circuits MPC/FPC awayday on credit

System-wide network effects / liquidity riskMonetary circuits MPC/FPC awayday on credit

System-wide network effects / liquidity riskMonetary circuits MPC/FPC awayday on credit

System-wide network effects / liquidity riskMonetary circuits • If demand for household and PNFC deposits grows in line with income, then lending can be accommodated out of deposit growth… MPC/FPC awayday on credit

System-wide network effects / liquidity risk • If demand for household and PNFC deposits grows in line with income, then lending can be accommodated out of deposit growth… • ...but if it grows faster, the financial network can become larger and more fragile MPC/FPC awayday on credit

The balance sheets (maroon is cash, blue is debt, orange is loans, green is equity, purple is contingent claims and red is other)

Side issue 1: the size of the UK banking system Banking sectors by residency UK-resident bank assets are large by international comparison... ...in part because of the UK’s role as a financial sector.... ...which means there are lots of foreign-owned banks in the UK... ...and that UK-owned banks’ global balance sheets are large. Sources: BIS, national central banks

Side issue 1: the size of the UK banking system London’s share of selected global markets UK-resident bank assets are large by international comparison... ...in part because of the UK’s role as a financial sector.... ...which means there are lots of foreign-owned banks in the UK... ...and that UK-owned banks’ global balance sheets are large. Sources: BIS, national central banks

Side issue 1: the size of the UK banking system Resident banks by ownership UK-resident bank assets are large by international comparison... ...in part because of the UK’s role as a financial sector.... ...which means there are lots of foreign-owned banks in the UK... ...and that UK-owned banks’ global balance sheets are large. Sources: BIS, national central banks

Side issue 1: the size of the UK banking system Global balance sheets by country of ownership UK-resident bank assets are large by international comparison... ...in part because of the UK’s role as a financial sector.... ...which means there are lots of foreign-owned banks in the UK... ...and that UK-owned banks’ global balance sheets are large. Sources: BIS, national central banks

The UK financial system, with cross-border inter-bank connections

Hedging example Tailored IR + FX hedge Corporate Bank A

Hedging example Tailored IR + FX hedge Corporate Bank A IR risk FX risk Bank B

Hedging example Tailored IR + FX hedge Corporate Bank A +10 +10 IR risk FX risk Bank B

Hedging example Tailored IR + FX hedge IR risk Corporate Bank A Bank C +10 FX risk +10 IR risk FX risk Bank B

Hedging example Tailored IR + FX hedge IR risk Corporate Bank A +5 Bank C +20 FX risk +15 IR risk FX risk Bank B

Hedging example Tailored IR + FX hedge IR risk Corporate Bank A +5 Bank C +20 FX risk +15 IR risk FX risk Bank B

Hedging example Tailored IR + FX hedge IR risk Corporate Bank A +5 Bank C +20 FX risk +15 IR risk FX risk Bank B =

Hedging example Tailored IR + FX hedge IR risk Corporate Bank A +5 Bank C +20 FX risk +15 IR risk FX risk Bank B = = 20 60 Gross MV

The balance sheets (maroon is cash, blue is debt, orange is loans, green is equity, purple is contingent claims and red is other)

Network risks: interconnections ? Chart 1: Stylised map of UK-resident banks’ £3.1 trillion repo market activity as of end-2011 Chart 8: Contagious links (orange arrows) and exposed banks (red dots) From Paul Baverstock’s note on Mapping UK-resident banks’ repo activity From Tomo Ota’s note on Mapping the UK interbank system – some insights from a new dataset

Example of further work on repo • Breakdown balance sheets further by underlying collateral-type • Use this to assess the impact of - increased hair-cuts - falls in asset prices (e.g. due to a snap-back in yields) on the value of sectors’ repo books and resultant collateral shortfalls (to maintain current levels of funding via repo).