Download

1 / 35

350 likes | 547 Views

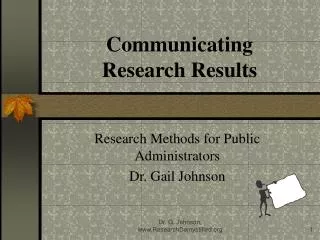

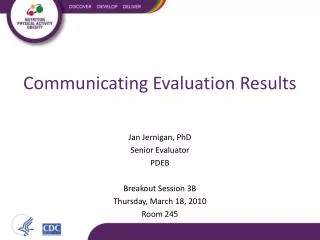

Communicating Results. Lectured by Dr. Siriluck Sutthachai Accounting lecturer Faculty of Management Science Khon Kaen University Khon Kaen, Thailand. WP. Develop Audit Findings. Review. Summary Sheet. No. Prepare Draft Audit Report. OK. Yes. Draft Audit Report. Review.

E N D

Communicating Results Lectured by Dr. Siriluck Sutthachai Accounting lecturer Faculty of Management Science Khon Kaen University Khon Kaen, Thailand

WP Develop Audit Findings Review Summary Sheet No Prepare Draft Audit Report OK Yes Draft Audit Report Review Exit Interview Prepare Final Audit Report No OK Yes Response/Planned Actions Final Audit Report Review Report Distribution/ Final Audit Report Review No OK Yes Final Audit Report No OK Sign Yes Audit Reporting Process

Report Purposes • InformTell what they found • Persuade Convince management on the worth and validity of the audit findings • Get resultsMove management toward change and improvement

Audit Report • Interim Report(รายงานระหว่างโครงการ) • รายงานด้วยวาจาหรือเป็นลายลักษณ์อักษรก็ได้ • รายงานเมื่อเป็นกรณีเร่งด่วนที่ต้องการการแก้ไข • รายงานเมื่อมีการเปลี่ยนแปลงขอบเขตการตรวจสอบ • รายงานแจ้งความคืบหน้าในการตรวจสอบกรณีโครงการนั้นๆใช้เวลานาน หรือแจ้งยืดอายุโครงการตรวจสอบ

Audit Report • Summary Report(รายงานสรุป) • รายงานผลการตรวจสอบที่กลั่นกรองแล้วว่ามีความสำคัญต่อผู้บริหารระดับสูง • Final Audit Report (รายงานการตรวจสอบ) • รายงานการตรวจสอบภายในอย่างละเอียดทั้งวัตถุประสงค์ ขอบเขตการตรวจสอบ ข้อมูลแวดล้อม และผลการตรวจสอบ • รายงานมีการลงนามโดยผู้อำนวยการสำนักตรวจสอบภายในหรือผู้ที่ได้มอบอำนาจ

Audit Report • Report should be • Objective • Clear • Concise • Constructive • Timely

Audit Report • Objective Report • Factual—รายงานข้อเท็จจริง/ สิ่งที่ตรวจพบจริง • Unbiased—ไม่มีอคติ ไม่มีความเห็นหรือทัศนคติส่วนตัวกระทบต่อการแสดงความเห็นในรายงานการตรวจสอบ • Free from distortion—ไม่มีการบิดเบือนข้อเท็จจริง • Without prejudice—ปราศจากความลำเอียง ไม่เลือกที่รักมักที่ชัง

Audit Report • Clear Report • Easily to understood—ง่ายในการทำความเข้าใจ • Logical—สมเหตุสมผล • Avoiding unneccessary technical language—หลีกเลี่ยงการใช้ศัพท์ทางวิชาการ • Providing sufficient supportive information—มีข้อมูลสนับสนุนอย่างเพียงพอ

Audit Report • Concise Report • To the point--ตรงประเด็น • Avoid unnecessary detail--หลีกเลี่ยงการเขียนรายละเอียดที่ไม่จำเป็น • Using fewest possible words to express thoughts--หลีกเลี่ยงการใช้คำที่เป็นลักษณะการออกความคิดเห็นส่วนตัว

Audit Report • Constructive Report • Content and tone—หลีกเลี่ยงการระบุชื่อบุคคลที่มีส่วนเกี่ยวข้องในความผิดพลาดในหน่วยรับการตรวจสอบ • Help the auditees and organization—เป็นประโยชน์ต่อผู้รับการตรวจและองค์กร • Lead to improvement—นำไปสู่การปรับปรุงงานให้มีประสิทธิภาพ • Timely Report • Issue without undue delay—รายงานตามกำหนดเวลาที่วางแผนไว้ • Enable prompt action—พนักงานมีเวลาที่จะนำไปปฏิบัติตามคำแนะนำ

Audit Report • Content • Purpose • Scope • Background Information • Summaries • Results of the audit

Audit Report • Purpose • วัตถุประสงค์ในการตรวจสอบ (Audit Objectives) • เหตุผลในการตรวจสอบ (Why the audit was conducted) • ความสำเร็จที่คาดหวังไว้ (What it was expected to achieve) • Scope • กิจกรรมที่ตรวจสอบ (Audited activities) • ระยะเวลาที่ตรวจสอบ (Time period audited) • กิจกรรมที่ไม่ได้ตรวจสอบ (Activities not audited) • เทคนิคการตรวจสอบ (Nature and extent of auditing perform

Audit Report • Conclusion (opinions) • การประเมินผลกระทบที่จะเกิดขึ้นจากผลการตรวจสอบที่มีต่อหน่วยรับการตรวจสอบซึ่งประเมินโดยผู้ตรวจสอบภายใน • การสรุปอาจเป็นการพิจารณาว่า วัตถุประสงค์ในระดับกิจกรรมและเป้ามายที่ตั้งไว้สอดคล้องกับวัตถุประสงค์องค์กรหรือไม่ และสนับสนุนวัตถุประสงค์องค์กรจนสามารถทำให้วัตถุประสงค์องค์กรบรรลุผลได้ และอาจพิจารณาว่า กิจกรรมที่รับการตรวจสอบมีการปฏิบัติงานอย่างที่วางระบบไว้หรือไม่

Audit Report • Background Information includes: • Organization unit and function • Relevant information • Status of prior audit report • Scheduled audit or requested audit • Summaries • Balance presentation of audit report content

Audit Report • Results of the audit • Findings • Conclusion • Recommendation • Corrective action/Auditee Accomplishment

Audit Findings • Pertinent statement of FACT • Emerged by a process of comparing “what should be” with “what is” • Based on the following attributes: • Criteria (หลักเกณฑ์) • Condition (สิ่งที่เป็นอยู่) • Cause (สาเหตุ) • Effect (ผลกระทบ)

Audit Findings • ข้อเท็จจริงหรืออนุมาน ?

Audit Findings • Criteria(what should be) • Standards—กฎ ระเบียบ กฎหมาย ข้อบังคับเกี่ยวกับเรื่องนั้น มาตรฐานวิชาชีพ มาตรฐานสำหรับเรื่องนั้นๆ • Measure—หน่วยวัดที่มีการกำหนดขึ้น • Expectation used in making evaluation/ verification—หลักวิชาการที่ดี หลักสามัญสำนึกที่ยอมรับกันทั่วไป • Condition (what does exist) • Factual evidence found in the course of the examination--สิ่งที่ปฏิบัติอยู่จริงในกิจกรรมที่ตรวจสอบและไม่เหมือนกับหลักเกณฑ์

Audit Findings • Cause(why the differences exist) • สาเหตุ/เหตุผลที่ทำให้เกิดความแตกต่างระหว่างภาวะที่คาดหวังกับสิ่งที่ปฏิบัติอยู่จริง • Effect (the impact of the difference) • The risk or exposure the auditee organization encounter because the condition is not the same as the criteria—ความเสี่ยงหรือความเสียหายที่อาจจะเกิดขึ้น • Degree of risk is based on the effect that may have on the organization’s financial statement—ความมีสาระสำคัญของความเสี่ยง

Audit Findings กรณีศึกษา

Recommendation • Types of Audit Recommendation • No change in the current system • Modification of the current internal control system • Transfer risk e.g. purchasing insurance against risk, outsourcing, hedge, share risk • Adjust the required rate of return on certain activities to reflect the associated risk • Terminate the risk e.g. pulling out of the market, divest, etc.)

Recommendation • Recommendation should be: • เป็นแนวทางในการแก้ปัญหาและลดความเสี่ยงได้ • สามารถปฏิบัติได้จริง • แก้ไขสาเหตุของปัญหาที่เกิดขึ้น • เหมาะกับขีดความสามารถ ความรู้ ความเชี่ยวชาญของผู้รับการตรวจที่จะนำไปปฏิบัติ • เทคโนโลยีที่มีสามารถรองรับการปฏิบัติของผู้รับการตรวจสอบ • ใช้ต้นทุน/ค่าใช้จ่ายที่เหมาะสม เป็นไปได้ และสอดคล้องกับความเสี่ยง • เป็นการแก้ไขปัญหาในระยะสั้นหรือในระยะยาว • ให้ประโยชน์มากกว่าต้นทุน/ค่าใช้จ่ายที่เสียไป

Corrective Action Taken • กิจกรรมที่ผู้เข้ารับการตรวจสอบได้ปฏิบัติตามคำแนะนำในรายงานการตรวจสอบภายใน โดยการปฏิบัติจะเกิดขึ้น: • ในระหว่างการตรวจสอบ—ในรายงานการตรวจสอบต้องแจ้งให้ผู้อ่านทราบว่าผู้ได้รับการตรวจสอบ ได้ทำกิจกรรมตามข้อเสนอแนะอะไรไปแล้ว • หลังจากเสร็จสิ้นการตรวจสอบ—จะเป็นรายงานหลังจากที่ผู้ตรวจสอบได้ทำการ Follow up

Audit Findings Summary Sheet • เป็นการรวบรวมข้อมูลจากหลายๆกระดาษทำการเพื่อพิจารณาว่าข้อมูลที่ได้จากการตรวจสอบมีความสมบูรณ์ ถูกต้องหรือไม่ • ข้อมูลสรุปจะเป็นประโยชน์ • ง่ายต่อการหารือกับผู้รับการตรวจในตอนทำ Field Work • ง่ายต่อการสอบทานของผู้บริหารตรวจสอบภายใน • เขียนรายงานการตรวจสอบได้ง่ายขึ้น

Audit Findings Summary Sheet Prepared by_______Date_____ Reviewed by______Date_____ W/P Ref.__________________ Criteria __________________________________________________________________________________________________________________________ Condition __________________________________________________________________________________________________________________________ Cause __________________________________________________________________________________________________________________________ Effect __________________________________________________________________________________________________________________________ Recommendation __________________________________________________________________________________________________________________________ Management Comments __________________________________________________________________________________________________________________________

ตัวอย่าง • กระบวนการรับคืนวัตถุดิบจากฝ่ายผลิตกำหนดไว้ว่า ฝ่ายคลังสินค้าจะต้องทำการบันทึกรับคืนในบัญชีรับคืนวัตถุดิบและในการ์ดคุมยอดวัตถุดิบคงเหลือแต่ละชนิดเพื่อให้ทราบปริมาณวัตถุดิบทั้งหมดที่อยู่ในมือและที่สามารถเบิกไปใช้เพื่อการผลิตได้ • จากการตรวจสอบพบว่า ในระยะเวลา 6 เดือนที่ผ่านมา วัตถุดิบที่ได้รับคืนจากฝ่ายผลิตไม่มีการบันทึกอยู่ในบัญชีของฝ่ายคลังสินค้าและไม่มีปรากฎในการ์ดคุมยอดวัตถุดิบแต่ละชนิด Criteria Condition

ตัวอย่าง Cause • เราพบว่า พนักงานที่รับผิดชอบในเรื่องการรับคืนวัตถุดิบจากฝ่ายผลิตไม่ได้รับการแจ้งให้ทราบว่า หน้าที่ความรับผิดชอบในตำแหน่งนี้มีอะไรบ้าง จึงไม่ได้ทำการบันทึกการรับคืน รวมทั้งหัวหน้าที่ดูแลในเรื่องนี้ไม่ได้ทำการตรวจสอบการทำงานของพนักงานฝ่ายคลังสินค้าเป็นระยะๆ • ผลจากการไม่บันทึกวัตถุดิบรับคืนทำให้บริษัทต้องเสียค่าใช้จ่ายในการซื้อวัตถุดิบเกืนความต้องการไปเป็นจำนวนเงิน 75,000 ดอลล่าร์สหรัฐ Effect

ตัวอย่าง Recommendation • เราได้ทำการพิจารณาเรื่องนี้ร่วมกับผู้จัดการฝ่ายคลังสินค้าและผู้จัดการเห็นชอบที่ควรจะมีการปรับปรุงข้อมูลการรับคืนวัตถุดิบทุกครั้งเพื่อให้ยอดจำนวนวัตถุดิบมีข้อมูลที่เป็นปัจจุบัน และเห็นด้วยว่าฝ่ายคลังสินค้าควรมีการจัดทำรายละเอียดลักษณะงานสำหรับแต่ละตำแหน่งงานให้ชัดเจน รวมทั้งหัวหน้าของหน่วยต่างๆ ในฝ่ายคลังสินค้าควรที่จะทำการทำงานของพนักงานอย่างสม่ำเสมอและส่งรายงานการทำงานนั้นมาเป็นระยะๆ • ก่อนที่เราจะทำการสรุปการตรวจสอบครั้งนี้ ผู้จัดการฝ่ายคลังสินค้าก็ได้แก้ไขการทำงานที่ฝ่ายคลังสินค้าตามที่เราได้แนะนำเป็นที่เรียบร้ยแล้ว และเมื่อเราได้ติดตามประเมินผลการปรับเปลี่ยนครั้งนี้ เราพบว่า การปฏิบัติเป็นไปอย่างมีประสิทธิผลแล้ว เราจึงเห็นว่า ฝ่ายคลังสินค้ามีการทำงานที่ดีในเรื่องนี้แล้ว Corrective action taken

Report Writing Techniques • Keep most sentences short and simple • Consistency/Flow in logical succession • Avoid technical jargon • Use action words • Use short paragraph

Audit Report Exit conference/Post-auditing meeting • To ensure no misunderstanding of facts • Give opportunity to auditees to clarify specific items and express views of the findings, conclusions, and recommendations • Participants • Individuals who are knowledgeable of detailed operation • Those who can authorized the implementation of corrective actions

Audit Report Exit conference/matter to be considered • Need for face to face discussion • Auditor should be in charge of the review • Prepared for conflicts and questions • Flexible on matters not affecting the substances of the report • Never negotiate the audit opinion • Disagreement should be explained in the report

Executing the exit conference Be on time Begin with introduction Set the clients at ease Give positive feedback first Discuss area needing improvement Obtain suggestions for improvement Sell recommendation where necessary Obtain agreement and move on Summarize the meeting Thank you Audit Report

Audit Report Final Audit Report • Reviewed and approved by the director of internal auditing or designees • Distributed to • Who are in position to take corrective action • Head of each audited unit • Senior management • Audit Committee • External Auditor

Follow up Follow up เป็นการติดตามผล หลังจากที่ได้มีการนำเสนอรายงานต่อผู้ที่มีส่วนเกี่ยวข้อง • เพื่อให้แน่ใจว่า มีการแก้ไข ปรับปรุงตามข้อเสนอแนะ หรือ • ยอมรับความเสี่ยงโดยผู้บริหารในระดับที่เหมาะสม • การติดตามผล • ขึ้นอยู่กับความเสี่ยง • ภายในระยะเวลาที่กำหนด • ให้ผู้รับการตรวจสอบรายงาน หรือผู้ตรวจสอบทำการสัมภาษณ์ หรือทดสอบรายการ • ออกรายงานติดตามผลใช้รูปแบบรายงานเหมือนกับ Audit Report โดยเพิ่มผลของการติดตามและความเห็นของผู้ตรวจสอบ

ตัวอย่างรายงานการตรวจสอบภายในตัวอย่างรายงานการตรวจสอบภายใน