Download

1 / 42

420 likes | 563 Views

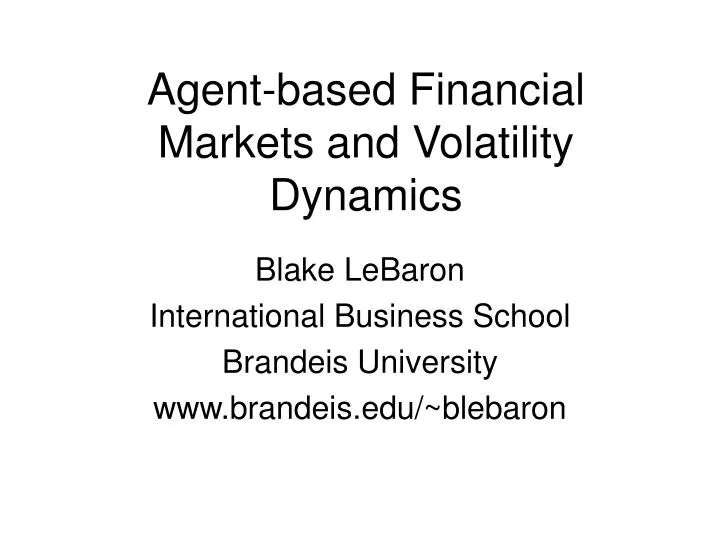

Agent-based Financial Markets and Volatility Dynamics. Blake LeBaron International Business School Brandeis University www.brandeis.edu/~blebaron. Fundamental Input. Market Output. Price Volatility Volume d/p ratios Liquidity. Geometric Random Walk. Agent-based Financial Market.

E N D

Agent-based Financial Markets and Volatility Dynamics Blake LeBaron International Business School Brandeis University www.brandeis.edu/~blebaron

Fundamental Input Market Output Price Volatility Volume d/p ratios Liquidity Geometric Random Walk Agent-based Financial Market

Overview • Agent-based financial markets • Example market • Prices and volatility • Future challenges

Agent-based Financial Markets • Many interacting strategies • Emergent features • Correlations and coordination • Macro dynamics • Bounded rationality

Bounded Rationality andSimple Rules • Why? • Computational limitations • Environmental complexity • Behavioral arguments • Psychological biases • Simple, robust heuristics • Computationally tractable strategies

Agent-based Economic Models • Website:Leigh Tesfatsion at Iowa St.http://www.econ.iastate.edu/tesfatsi/ace.htm • Handbook of Computational Economics (vol 2), Tesfatsion and Judd, forthcoming 2006.

Example Market • Detailed description: • Calibrating an agent-based financial market

Assets • Equity • Risky dividend (Weekly) • Annual growth = 2%, std. = 6% • Growth and variability in U.S. annual data • Fixed supply (1 share) • Risk free • Infinite supply • Constant interest: 0% per year

Agents • 500 Agents • Intertemporal CRRA(log) utility • Consume constant fraction of wealth • Myopic portfolio decisions

Trading Rules • 250 rules (evolving) • Information converted to portfolio weights • Fraction of wealth in risky asset [0,1] • Neural network structure • Portfolio weight = f(info(t))

Information Variables • Past returns • Trend indicators • Dividend/price ratios

Rules as Dynamic Strategies Portfolio weight 1 f(info(t)) 0 Time

Portfolio Decision • Maximize expected log portfolio returns • Estimate over memory length histories • Olsen et al. • Levy, Levy, Solomon(1994,2000) • Restrictions • No borrowing • No short sales

Heterogeneous Memories(Long versus Short Memory) Present Return History Future Past 2 years 5 years 6 months

Short Memory: Psychology and Econometrics • Gambler’s fallacy/Law of small numbers • Is this really irrational? • Regime changes • Parameter changes • Model misspecification

Agent Wealth Dynamics Short Long Memory

New Rules: Genetic Algorithm • Parent set = rules in use • Modify neural network weights • Operators: • Mutation • Crossover • Initialize

GA Replaces Unused Rules In Use Unused

Trading • Rules chosen • Demand = f(p) • Numerically clear market • Temporary equilibrium

Homogeneous Equilibrium • Agents hold 100 percent equity • Price is proportional to dividend • Price/dividend constant • Useful benchmark

Two Experiments • All Memory • Memory uniform 1/2-60 years • Long Memory • Memory uniform 55-60 years • Time series sample • Run for 50,000 weeks (~1000 years) • Sample last 10,000 weeks (~200 years)

Financial Data • Weekly S&P (Schwert and Datastream) • Period = 1947 - 2000 (Wednesday) • Simple nominal returns (w/o dividends) • Weekly IBM returns and volume (Datastream) • Annual S&P (Shiller) • Real S&P and dividends • Short term interest

Price/return Features • Mean • Variance • Excess kurtosis (Fat tails) • Predictability (little) • Long horizons (1 year) • Near Gaussian • Slow convergence to fundamentals

Volatility Features • Persistence/long memory • Volatility/volume • Volatility asymmetry

Crashes and Volume • Large price decreases and • Trading volume • Rule dispersion

Summary • Replicating many volatility features • Persistence • Volume connections • Asymmetry • Crashes, homogeneity, and liquidity (price impact) • Simple behavioral foundations • Not completely rational • Well defined

Future Challenges • Model implementation • Validation • Applications

Model Implementation • Complicated • Compute bound • Nonlinear features • Estimation • Ergodicity

Future Validation Tools • Data inputs • Price and dividend series training • Wealth distributions • Agent calibration • Micro data • Experimental data • Live market information/interaction

Applications • Volatility/volume models • Estimation and identification • Risk prediction (crash probabilities) • Market and trader design • Policy • Interventions • Systemic risk • Forecasting