Download

1 / 4

130 likes | 553 Views

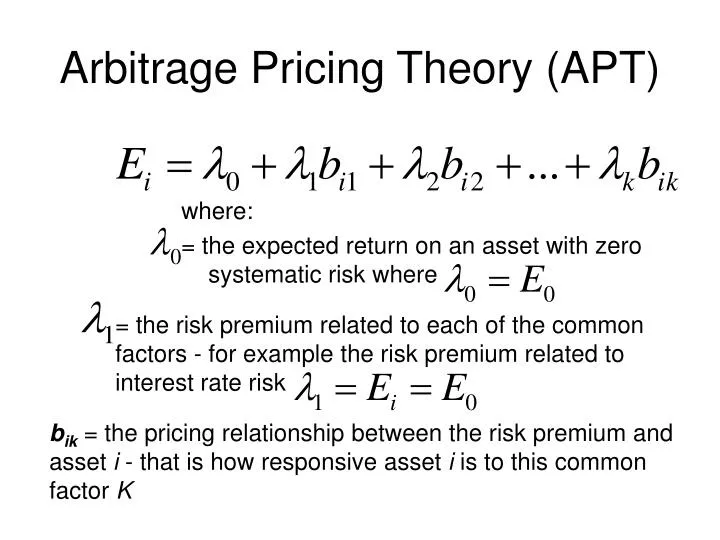

Arbitrage Pricing Theory (APT). where: = the expected return on an asset with zero systematic risk where. = the risk premium related to each of the common factors - for example the risk premium related to interest rate risk.

E N D

Arbitrage Pricing Theory (APT) where: = the expected return on an asset with zero systematic risk where = the risk premium related to each of the common factors - for example the risk premium related to interest rate risk bik = the pricing relationship between the risk premium and asset i - that is how responsive asset i is to this common factor K

Example of Two Stocks and a Two-Factor Model = changes in the rate of inflation. The risk premium related to this factor is 1 percent for every 1 percent change in the rate = percent growth in real GNP. The average risk premium related to this factor is 2 percent for every 1 percent change in the rate = the rate of return on a zero-systematic-risk asset (zero beta: boj=0) is 3 percent

Example of Two Stocks and a Two-Factor Model = the response of asset X to changes in the rate of inflation is 0.50 = the response of asset Y to changes in the rate of inflation is 2.00 (by1 = 2.00) = the response of asset X to changes in the growth rate of real GNP is 1.50 = the response of asset Y to changes in the growth rate of real GNP is 1.75

Example of Two Stocks and a Two-Factor Model = .03 + (.01)bi1 + (.02)bi2 Ex = .03 + (.01)(0.50) + (.02)(1.50) = .065 = 6.5% Ey = .03 + (.01)(2.00) + (.02)(1.75) = .085 = 8.5%