Download

1 / 10

120 likes | 345 Views

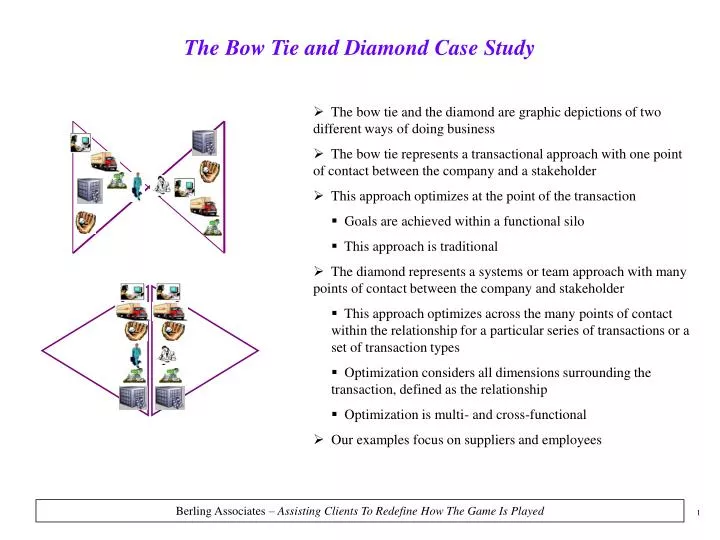

The Bow Tie and Diamond Case Study. The bow tie and the diamond are graphic depictions of two different ways of doing business The bow tie represents a transactional approach with one point of contact between the company and a stakeholder

E N D

The Bow Tie and Diamond Case Study • The bow tie and the diamond are graphic depictions of two different ways of doing business • The bow tie represents a transactional approach with one point of contact between the company and a stakeholder • This approach optimizes at the point of the transaction • Goals are achieved within a functional silo • This approach is traditional • The diamond represents a systems or team approach with many points of contact between the company and stakeholder • This approach optimizes across the many points of contact within the relationship for a particular series of transactions or a set of transaction types • Optimization considers all dimensions surrounding the transaction, defined as the relationship • Optimization is multi- and cross-functional • Our examples focus on suppliers and employees

Company Team Supplier Team Buyer Sales Rep Traditional Supplier Interface The traditional relationship between company and supplier looks like a bow tie, with the company’s buyer and the supplier’s salesperson at the midpoint of the tie – only communicating directly with each other across the companies. Each of the “opponents” are attempting to reach the best “deal” they can, despite the transaction’s impact on the rest of the organization. For example, the supplier might have a 12-pack on special and the company’s customers’ only order 3-packs. The buyer gets a great price per unit, but the warehouse is left the task of repacking the goods into 3-packs. Looking at another dimension of the same transaction, the company’s accounts payable department spends a significant amount of time reconciling receiving reports to purchase orders and to invoices because of incomplete information. Because of the lack of the “right” information, the accounts payable detail does not reconcile to the total amounts due as claimed by the supplier. This results in the payments, sent by the company to the supplier, having incomplete cash remittance information. This in turn results in the supplier’s accounts receivable department expending additional time reconciling the company’s account.

Company Team Supplier Team --- IT --- - Transportation - -- Product Development -- - Sales/Purchasing - -- Accounting -- -- Warehouse -- Enhanced Supplier Interface A different approach is to turn the bow tie inside out so the interaction with the supplier looks more like a diamond, with a number of points of contact between the companies. There are two benefits with this approach. First, the buying and selling processes become multi-functional. This affords visibility to the impact of buying decisions across the company. In our previous example of the 12-pack special, the receiving department would be able to provide input on the disruption and additional cost required to repackage the goods. This would give purchasing a more holistic context for the buy decision on the special. The second benefit with this approach is the opening of direct communication lines across the points of contact between the supplier and company. In our previous example, additional man-hours are being incurred in the account reconciliation process because the accounts payable department of the company does not have the “right” information. This lack of the right information is driving behavior in the company, which in turn causes additional man-hours to be incurred in the supplier’s accounts receivable department. Opening the communications lines across the companies could eliminate this additional work for both parties.

The Diamond and Suppliers The Problem A consumer products company owed a large amount to a key supplier, and it was significantly past due. The reason the large balance was in arrears was the numerous unreconciled errors in the account transactions detail, which were attributed to perceived invoicing problems at the supplier. The situation had escalated to the point the supplier slowed its shipments to the company and was threatening to stop all shipments until full payment was received. The Cause Both the VP of Sales and the VP of Purchasing were feeling the product squeeze from the supplier and decided to visit the Accounts Payable Manager and Controller. What they heard from the Accounts Payable Manager was that the supplier was not providing the “right” information to support the invoiced amounts. And, no payments would be made of balances not fully supported. The Solution Internal and External Events - The Controller took the lead. He arranged a meeting, with the assistance of the VPs of Purchasing and Distribution, with the buyer assigned to the product line provided by the supplier and with the manager of the Receiving Department. They found that part of the missing “right” information was in the Receiving Department, but the rest of it was with the supplier. (Changes were made in the internal business processes to ensure the right information in house would start flowing to Accounts Payable.) Next, the Controller called the Controller at the supplier. A conference was set for the appropriate Credit and Accounts Receivable personnel at the supplier and the Controller and Accounts Payable personnel at the company. At the conference all the details of who had what information were understood.

The Diamond and Suppliers Cross-Company Problem Solving and Process Simplification - A week after the conference, a second meeting was held. This meeting included representatives from the Sales Department, Shipping Department and Customer Service Department, in addition to the accounting personnel at the supplier. From the company, in addition to the accounting personnel, the Receiving Department manager and Buyer were in attendance. For this meeting, all brought the business process maps from their departments and close attention was focused on the interfaces of information between the departments and the two companies, i.e. between shipping and receiving, between accounts receivable and accounts payable, etc. Glitches were found in the information hand-offs both within and across both companies. Actions were taken to remedy the causes of the errors. The account transaction errors were reconciled, and new business process activities were put in place to ensure the errors do not arise again. While this example is from what may be considered a mundane dimension of the relationship between supplier and company, a lack of attention to these details can cause major headaches. Attention to them can result in a stronger more efficient and effective relationship between company and supplier.

Business Forecast Sales Plan Production Schedule Inventory Plan Order Release Plan Warehouse Plan Demand Information (POS Data) The Diamond and Suppliers The Search For Advantage A distributor of health care products was operating in an industry segment undergoing rapid and massive consolidation. Competition was cutthroat, cost pressures were monumental. The distributor was looking for ways to create barriers to competitors by leveraging its relationship with one of its primary suppliers. The distributor had access to POS data from a number of its customers, but had not really ever used this information. The Opportunity The distributor and supplier held a series of meetings to identify ways in which they might work together to reduce the total cost of the distributors’ product to his customer. They both understood that the supplier’s lowering of the product acquisition cost (one component of total cost) was not a practical solution for the supplier. The distributor and supplier decided to form a team of IT personnel from both companies. This team took the demand data (POS information) over time and performed a series of sophisticated data mining and analytical exercises. Through this work the team identified consumer purchase behavior patterns within various SKUs, demonstrated during certain days of the week and months. From this work the team created a tool for crafting a sales forecast for over one-half of the SKUs the distributor purchased from the supplier for the distributor’s customers.

Business Forecast Sales Plan Production Schedule Inventory Plan Order Release Plan Warehouse Plan Demand Information (POS Data) The Diamond and Suppliers Cross-Company Problem Solving and Process Simplification Next, a team of personnel from the Sales Department of the supplier and the Purchasing Department of the distributor began to review the historic demand data and the results of the IT team’s work. This team compared how the distributor had purchased from the supplier historically, against the amounts the distributor’s customers were actually selling to their customers. They noted how the purchasing patterns were historically out of synch, gaining visibility into both long and short stock positions of the distributor’s customers. They also could see how scheduling their business using the forecasting model (which is based on the weekly demand data) could potentially smooth out the flow of product through the supply chain, reducing inventories for the supplier and distributor. Interestingly, they developed a six-month sales forecast, inventory level and turnover goals for each of them, and a schedule of planned order releases against the sales forecast. They shared each other’s goals and held each other accountable for the attainment of each others goals. The distributor then took this data and analysis to the Distribution Center manager. They began to discuss how the change in product flow patterns would impact the work in the DC. The DC manager began to consider smaller unit, more frequent deliveries from the supplier and began to think of ways the supplier could package the inventory at shipment to make it easier on the DC manager’s receiving and put-away processes. It was decided another team should be created. This team would be made up of the DC managers of the supplier and distributor. The DC manager of the distributor invited representatives of the receiving and put-away work groups to join this team. The DC manager of the supplier invited representatives of the pulling and shipping work groups to join the team. From a series of meetings with this team it was concluded that new product packs could be designed for the distributor. It was also determined that with better information they could eliminate the backorder method of purchasing/receiving and change to a fill or kill method. This not only speeded up the receiving process, but also eliminated major tracking and reconciliation issues in both inventory control and accounting.

Business Forecast Sales Plan Production Schedule Inventory Plan Order Release Plan Warehouse Plan Demand Information (POS Data) The Diamond and Suppliers Cross-Company Problem Solving and Process Simplification (continued) Seeing how these teams worked to impact inventory levels, receiving and shipping activities, and the activities in the inventory control and accounting areas, it was decided that cross-company multifunctional communication was good. Accordingly, a weekly telephonic Sales and Operations Planning meeting is now held with representatives of all the departments in both companies to review the weekly sales forecast for the distributor’s customers. Decisions are made from the information shared at that meeting on what product to move through the supply chain and what work to schedule in both DCs. The result is that inventory levels and over-time are both down. Extending the Opportunity Now that the distributor is comfortable managing the flow of product from the supplier to himself, he is getting ready to turn toward his customers. He wants to extend his command over the flow of product and the management of transaction related costs from the supplier to his customer. He wants to anchor his management of product flow in demand planning and be the driver of the supply chain, managing and controlling the information necessary to do this effectively.

Company Team Supplier Team --- IT --- - Transportation - -- Product Development -- - Sales/Purchasing - -- Accounting -- -- Warehouse -- The Diamond and Employees The gains that can be obtained by effectively and efficiently linking business processes between the company and the supplier are very tangible. The gains typically improve productivity, i.e. reduced man-hours of effort per unit of work, lower manning levels, and elimination of unnecessary activities and related work. In addition to the business process efficiencies to be gained, there are less easily measurable gains to be obtained from the employees of both the company and supplier. Employees are given an opportunity to contribute to the improved efficiency of their jobs by changing the causes of inefficiency at the source. They are working outside the bounds of their traditional jobs making change to improve the methods used to perform their work. They become ambassadors of the company working for improvements across company boundaries. Relationships are formed; open communications are fostered; and employee satisfaction improves. This environment should have two tangible results. First, the employee turnover levels should decrease. Second, the cross-company relationships should create barriers to entry for other suppliers. This is because the relationship is built around the interaction of a many multi-functional personnel versus one sales person and one buyer.

The Diamond and Employees The Situation An industrial products company collected warranty returned units from its customers and returned them to the supplier for credit. Returns were picked-up from customers, held at the branch until certain minimum quantities were accumulated, then sent to the regional DC for consolidation with units from other branches, then periodically sent to the main DC for further consolidation and return to the supplier. Transfer transactions were recorded at each step of the physical movement of the units to be returned. These transactions were processed by the company’s accounting department moving the inventory from one location to another, and eventually claiming the return to the supplier. The supplier was receiving the returns and issuing the appropriate paperwork to the company. This business process had been in place for twenty years. Cross-Company Problem Solving and Process Simplification For the first time, at its annual key supplier meeting, the company invited its accounting personnel and the supplier brought its accounting personnel. As the two groups of accountants met, the topic of warranty returns and the laborious process associated with processing the activity at the company became the focus of the discussion. As the accountants commiserated, a larger issue emerged, that being, the cost to the company to move the returns from the customer through the main DC and on to the supplier. The company’s accountants took ownership of the effort to review and change the way returns were processed. After a series of meetings with product, distribution, and transportation personnel at the company and product, distribution, and transportation personnel at the supplier, the accountants modeled a new process to transfer returns from the branches directly to the supplier’s DC. In addition to the change in the physical flow of the returns, the accountants also clarified a number of the return “rules” that were complicating the processing activity between the supplier and company.