Download

1 / 14

140 likes | 207 Views

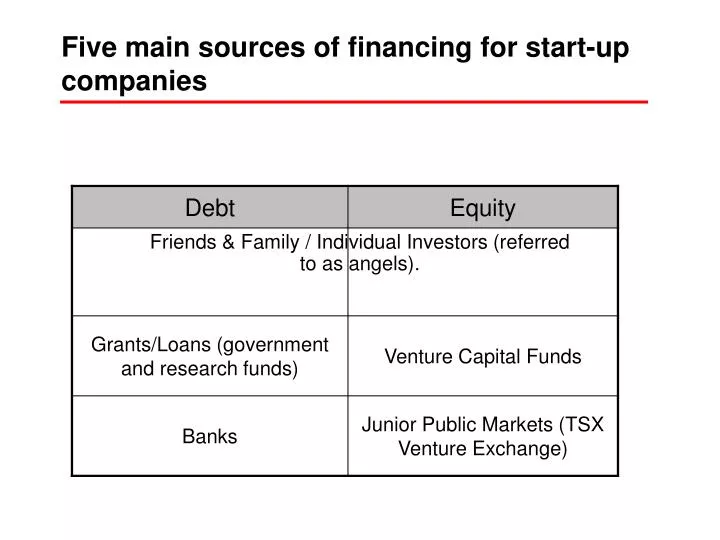

Five main sources of financing for start-up companies. Friends & Family / Individual Investors (referred to as angels). At what stage of the business do VCs invest?. Who can attract VC investment ?. Revenue Potential ($M). Can Raise VC $. Cannot Raise VC $.

E N D

Five main sources of financing for start-up companies • Friends & Family / Individual Investors (referred to as angels).

Who can attract VC investment? Revenue Potential ($M) Can Raise VC $ Cannot Raise VC $

Finding the right deal is the challenge! • Venture Capital is: Equity investment in high risk, but high potential and high growth businesses: • Looking for 100% per year or higher growth • Business has potential to dominate a market • VC has ability to exit in the future • VCs invest in < 2% of the business plans they review

IC Review Formal Due Diligence Complete Legal documents Formal recommendation Basic Screen Initial analysis Initial meetings Submission Decision 2 to 6 weeks 2 to 6 months Communication with LPs Cash Call Communication with LPs Due Diligence: From submission to decision • Complete process could take anywhere from 2 to 6 months • Initial screening and analysis can quickly disqualify up to 90% of submissions • Deep due diligence is an iterative process that is done on 10% to 15% of the submissions • Final investment is made on 1% to 2% of deals

Basic screening cuts out > 50% of deals • Was this company referred to me by someone I know? • Does the deal fit with the stage of my fund? • Does the deal fit with my fund’s focus • Technology • Geography • Size of investment • Other mandate • Are there any potential conflicts with existing portfolio companies? • Is the executive summary or business plan well written?

Initial analysis and dialogue with entrepreneur help narrow the funnel to 10% to 15% of deals • Management • Are the founders serial entrepreneurs? • Ethical or moral issues at play? (zero tolerance) • Market • Is the target market large enough (total available market >$100M)? • Can the Company become a dominant force in its market? • Is the business an “enabler” of future industry developments, and does it fit within the long-term structure of the industry (roadmap)? • Product, Technology and Intellectual Property (IP) • Does the company create or own anything truly unique and novel? • Does the company/entrepreneur own the Intellectual property or are partnerships required • Financial and other considerations • Can it achieve objectives within available funding, and can we easily foresee where the syndicate can be formed? • Can it attain $250M value (importance or market cap) in a reasonable time frame (5 to 7 years)? • Is there an exit for VC down the road • Is the business one of the half-dozen best deals we expect to see all year?

Due Diligence: Trust, but Verify • Due Diligence is: Rigorous research to verify the company’s claims and to understand the risks • Due Diligence consists of: • Checking the accuracy of the business plan • Collecting data by calling (perspective) customers channel partners, ex-bosses and employees. • Validating feasibility of projections (financial, business, product) • Conducting patent searches, technical studies, market studies. • Reviewing audited financial statements

Technology and product Technological achievement is not a sufficient basis for market acceptance…

Is the entrepreneur realistic about …. • …. the opportunity • Open, honest and “spin-free” • …. the competitive advantage • Willing to learn and change • …. managements capabilities • Customer focus NOT technology focus • …. deal structure & terms • The ‘pie’ will grow

My contact: jennyinc@gmail.com Local angel groups: http://www.angelforum.org/ http://www.wutif.ca/ Local technology associations and news: momentum.vef.org www.techvibes.com www.bctia.org Recommended Readings Crossing the Chasm by Geoffrey A. Moore (must read for engineers – go to market strategies for new technologies) Founders at Work: Stories of Startups' Early Days by Jessica Livingston http://blog.guykawasaki.com/ http://www.avc.com/