Download

1 / 25

250 likes | 333 Views

An Overview of CPA Firm Mobility. Gary McIntosh AICPA Co-Chair, Uniform Accountancy Act Committee. September 9, 2014. Mobility: A Short History. Prior to the Profession’s Individual CPA Campaign , CPAs often had to hold multiple reciprocal state licenses

E N D

An Overview of CPA Firm Mobility Gary McIntosh AICPA Co-Chair, Uniform Accountancy Act Committee September 9, 2014

Mobility: A Short History • Prior to the Profession’s Individual CPA Campaign, CPAs often had to hold multiple reciprocal state licenses • Bureaucratic Compliance Nightmare • Inconsistent Standards Across the States

Mobility: A Short History • Approximately a decade ago, profession leaders joined together to try to resolve the problem • Idea launched to treat a CPA license like a driver’s license – portable across state lines

Mobility • Basic concept • No notice • No fee • No escape (strong protections)

Mobility • Additionally, a CPA license, like a driver’s license, must be predicated on substantial equivalency • A CPA = a CPA = a CPA • 150 hours of education, CPA Exam passed, 1 year of experience

Uniform Accountancy Act • Individual CPA Mobility Language was inserted into the Uniform Accountancy Act (UAA) in 2006 • UAA is the profession’s model state act • Written jointly by AICPA and NASBA • States then model their accountancy statutes off of the UAA

Mobility • The original plan allowed full individual and CPA firm mobility • Concerns arose, however, about how the new concept would work in practice • Untested • Particular interest in being cautious about the attest function • Final proposal changed to allow individual CPA mobility and CPA firm mobility for non-attest services • Attest services would still require the registration of a CPA firm in any state where attest services are offered, however the firms’ CPAs could operate without reciprocal licenses • Additional concerns at the time about peer review, use of firm names, and CPA ownership standards – mostly now resolved

The Campaign Begins • A True Partnership of the Entire Profession • State CPA Societies • State Boards of Accountancy • AICPA • NASBA • CPA Firms and individual CPAs

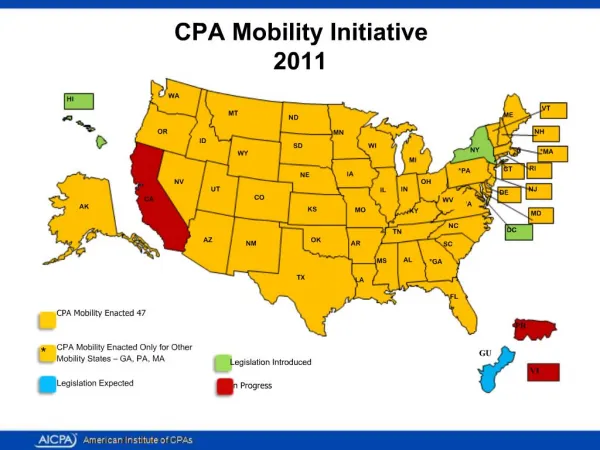

Mobility • Only 3 Jurisdictions Remain • Hawaii (Discussions occurring regarding a 2015 push) • Guam (legislation expected in Summer/Fall 2014) • Commonwealth of the Northern Mariana Islands (legislation expected in Summer/Fall 2014)

Mobility • Additionally, AICPA and NASBA have established resources for CPA Firms and Individual CPAs • CPAMobility.org

An Incredible Success Story • Statutes modernized to reflect actual way CPAs practice around the country • No complaints about enforcement by state BOAs • Bureaucratic red tape and fees that don’t serve public interest eliminated • Envy of other professions

Mobility • Nonetheless, some minor implementation issues remain • Some states still have a few state-specific provisions (ex. casinos, ag audits) • Massachusetts and Georgia have “quid pro quo” provisions

Firm Mobility • Profession now revisiting CPA Firm Mobility for attest • Completion of a promise made in 2006 • Timely after successful history with individual mobility

Uniform Accountancy Act Initiative on CPA Firm Mobility for Attest • Multi-year project • Exposure draft with 90 day comment period • Approximately 3 dozen comment letters received • Language approved Spring 2014 by AICPA and NASBA • States being asked to look at the new language

Firm Mobility Model for Attest Services • Same as individual mobility • “no notice, no fee, no escape” • Already in place for non-attest services • States will gain additional explicit authority to go after unregistered firms

Firm Mobility: Public Protections • To be eligible, must comply with peer review and CPA ownership requirements of mobility state • If not in compliance, then must seek to register as an ‘out-of-state’ firm

Firm Mobility • 14 states already have CPA firm mobility and it appears to be working well • States like OH and VA have had firm mobility for over a decade

Firm Mobility • This new language will not be a concerted campaign. • Commitment not to push like with individual CPA mobility • Reasons: • Individual CPA mobility is too new in some states • Other pressing state issues needing to take precedent • Boards and societies need to review the concept, discuss with stakeholders and members, consider if appropriate

Firm Mobility • What are the biggest obstacles and concerns in regard to CPA Firm Mobility? • Same common concerns we heard in regard to individual mobility in the past • Need to educate, discuss, and develop a comfort level among our partners

Firm Mobility • Lessons from the UAA Comment Period on the CPA Firm Mobility Language • State Societies and CPA Firms all broadly supportive • State BOAs mixed, some strongly supportive, others opposed or had questions or concerns • States BOAs with CPA firm mobility already in place often proved to be the most supportive of other states joining them

Firm Mobility • Common Concerns That Needed to be Examined • Understanding the peer review protections • Potential Insufficient Information without registration/notification • Questions about enforcement • Inconsistency between states (e.g. compilations) • Concerns about insufficient information or study of the issue. • Potential Loss of Revenue from Out-of-state Registration Fees