Download

1 / 11

110 likes | 244 Views

Long-Run Exchange Rates. PPP. Purchasing Power Parity. The Law of One Price (LOOP) Gold, silver, oil, and securities with identical risk & return each have the same price everywhere That’s common sense

E N D

Purchasing Power Parity • The Law of One Price (LOOP) • Gold, silver, oil, and securities with identical risk & return each have the same price everywhere • That’s common sense • Actual applications may require considerable disentangling of tariffs & local taxes, transportation costs

Weaker Relationship • For real estate it clearly does not work in any absolute sense • But, if humans were perfectly mobile, would real estate prices become uniform everywhere? • People are already very mobile; comparable units in major cities have become comparably expensive. How about comparable rural locations?

Back to PPP • PPP is also common sense, but isn’t that simple • What is a “representative market basket of goods?” • Absolute PPP: ER = relative prices • Very strong assumption • ER(¥/$) = P¥/P$

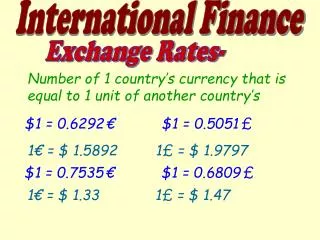

ER(¥/$) = P¥/P$ • If ER = 110, as it does now, almost • A New York salary of $100 a day is as livable as a Tokyo salary of ¥11,000 a day • An Alaska salary of $500.00 per week is equivalent a Hokkaido salary of ¥55,000 • A one week $3000 ecotourism package in Maui should be similar to a ¥330,000 package in Okinawa

Relative PPP • Using the above equation and a little mathematics, • Ln(¥/$) = ln(P¥) – ln(P$), • Taking derivatives with respect to time, • %Δ(¥/$) = %ΔP¥ - %ΔP$ • This equation says that the per cent appreciation of the dollar should equal the Japanese inflation rate minus the US inflation rate

Long-Run Exchange Rate Changes • Remember, MV = Py? • M$V$ = P$y$, & M$V$/y$, = P$, • M¥V¥ = P¥y¥ & M¥V¥/y¥ = P¥ • OK, rearrange terms to get: • R(¥/$) = P¥/P$ = (M¥/M$)(V¥/V$)(y$/y¥)

Reality Check R(¥/$) = P¥/P$ = (M¥/M$)(V¥/V$)(y$/y¥) Is this equation valid? LHS: R(¥/$), has fallen recently, 120 to 110 (yen appreciation) P¥/P$ has also fallen due to minor deflation in Japan & minor inflation in USA So R(¥/$) = P¥/P$ is OK

What About the RHS? • Is (M¥/M$)(V¥/V$)(y$/y¥) falling? • We know that (M¥/M$) is rising due to Japanese use of monetary policy to stimulate the economy • We also know that (y$/y¥) is rising due to faster growth rate in USA • Two of the terms are rising?

(M¥/M$)(V¥/V$)(y$/y¥) • This means that (V¥/V$) must be falling rapidly enough to offset the other two terms • What do we know about velocity that could lead to that conclusion?

Let’s Talk About • R(F/$) = PF/P$ = (MF/M$)(VF/V$)(y$/yF) • F, of course, stands for Foreign currency. • What about the currencies of Korea, China, Europe?