Download

1 / 28

300 likes | 572 Views

Session 6: Capital Structure I. C15.0008 Corporate Finance Topics. Outline. Basic capital structure theory—irrelevance Debt and equity as options Tax effects Valuation. Introduction to Capital Structure.

E N D

Session 6: Capital Structure I C15.0008 Corporate Finance Topics

Outline • Basic capital structure theory—irrelevance • Debt and equity as options • Tax effects • Valuation

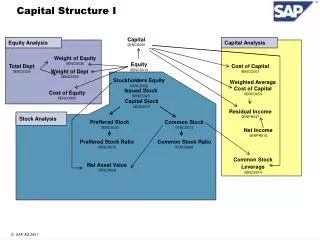

Introduction to Capital Structure Problem: What is the optimal mix of debt and equity, i.e., the capital structure that maximizes the value of the firm? Approach: Begin with a simple model (a framework) that identifies the relevant issues, then add realism.

A Road Map • Perfect markets (no taxes) capital structure is irrelevant • +corporate taxes more debt is better • +financial distress and agency costs optimal capital structure

Options and Corporate Finance Consider a firm that will liquidate in 1 year, with $10 million of 1-year zero coupon debt outstanding. If the firm is worth less than $10 million in 1 year, the debtholders receive everything and the stockholders receive nothing. Otherwise, the debtholders receive $10 million and the stockholders receive the residual.

Equity and Debt Payoffs Equity Debt Firm value Firm value 10 10 • Equity: a call option on the firm • Debt: firm - call = risk-free bond - put

Firm 99 60 44 An example A firm undertakes a risky, zero NPV project and will be worth either $99 mill. or $44 mill. in 1 year. Value of the unlevered firm is $60 mill. Risk free rate is 10%

Firm Equity Debt 99 44 55 60 ? ? 44 0 44 Introducing Debt The firm finances itself through Debt of $55 million to be paid after 1 year.

Replicating Equity Replicate equity with a position in the firm financed by borrowing: 99 H - 1.1 B* = 44 44 H - 1.1 B* = 0 H = 0.8, B* = 32 S = 0.8(60) - 32 = $16 million

Replicating Debt Replicate debt with a position in the firm and a position in risk-free debt: 99 H - 1.1 B* = 55 44 H - 1.1 B* = 44 H = 0.2, B* = -32 • B = 0.2(60) + 32 = $44 million • V = S + B = 16 + 44 = $60 mill. Remained the same!

Assumptions • Perfect capital markets (no taxes or transaction costs) • Personal and corporate borrowing at the same rate • No information effects

The Primary Result The value of the firm is independent of its capital structure, i.e., the financing mix is irrelevant (Miller & Modigliani). Proposition I: VU = VL

Intuition • Buying equity in the levered firm is firm-generated leverage • Buying equity in the unlevered firm and borrowing is do-it-yourself leverage • Conclusion: no one is willing to pay the firm for levering up when they are “free” to lever up individually

Discount Rates The value result also has implications for discount rates (r0 is the cost of unlevered equity). Proposition II: rS = r0 + (B/S)(r0 - rB) WACC = r0 The WACC is constant and the cost of equity can be decomposed into business risk and financial risk.

Valuation: The Dividend Discount Model • The stock price today should be the discounted value of expected future dividends P = t Dt/(1+rS)t • If dividends are growing at a constant rate, then the price of the stock (not including current dividend) is P0 = D1 / (rS - g)

Expected Returns, Growth and P/E Ratios • The valuation formula can be inverted to get expected returns: rS = (D1 / P0) + g • Where does growth come from?g = bROEb — earnings retention rate, i.e., D=(1-b)EROE—return on equity • What are the implied P/E ratios?P0 = D1 / (rS - g) = (1-b) E1 / (rS – b ROE) P0 / E1 = (1-b) / (rS – b ROE)

Equity Valuation The value of all the equity is just the aggregate value of all the shares outstanding, i.e., the discounted value of aggregate dividends. All the previous results apply.

Introducing Corporate Taxes • Earnings are taxed at the corporate rate • Interest expense is tax deductible • Dividends are not tax deductible • Tax rate: TC

Value Implications Proposition I: VL = VU + PV(tax shield) PV(tax shield) = t[TC(interest expense)t] / (1+ rB)t • Debt reduces the firm’s tax liability and therefore increases value • The more debt, the higher the value of the firm

An Example All equity firm with pre-tax earnings (cash flow) of $X in year 1, a retention rate of b, and growth rate g in perpetuity: VU = [(1-b)(1- TC)X] / (r0-g) If this firm adds $B of perpetual debt: PV(tax shield) = [TC (rB B)] / rB = TC B VL = VU + TC B

Discount Rates Prop. II: rS = r0 + (1- TC)(B/S)(r0 - rB) WACC = [(S+(1- TC)B)/(S+B)] r0 • Equity risk increases with leverage (but more slowly than in the no tax case) • WACC decreases as the amount of debt increases

Recapitalization: An Example Firm characteristics: • EBIT: 50% prob. of $1 million, 50% prob. of $2 million (in perpetuity) • Depreciation = Cap. Ex. • ΔNWC=0 • 100% payout (no growth, dividends = earnings) • r0 = 10% (required return on unlevered equity) • TC = 40%

Unlevered Value VU = [(1- TC)EBIT] / r0 = [(1-0.4)1.5] / 0.1 = $9 mill. n = 1 million (shares outstanding) Share price: P = VU / n = $9.00

Recapitalization Firm issues $5 million of perpetual debt (rB = 8%) and uses the proceeds to repurchase equity. On announcement: • Shareholders revalue the firm: VL = VU + TC B = 9 + 0.4 (5) = $11 million • Share price moves to $11/share $ 5 million repurchases 454.5 shares (n = 545.5)

Assignments • Reading • RWJ: Chapters 16.1-16.9, Appendix 16B • Problems: 16.2, 16.6, 16.8 • Problem sets • Problem Set 2 due monday • Cases • AHP due in 1 week