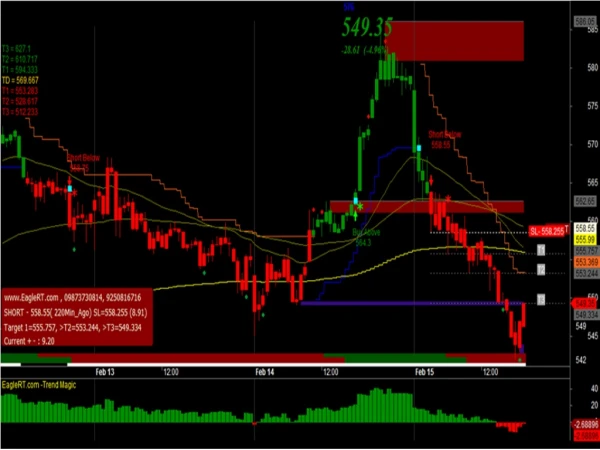

Download

1 / 11

110 likes | 244 Views

Machine learning and short positions in stock trading strategies . D.E Allen, R. Powell and A. K. Singh Edith Cowan University. Reading questions. What is short selling and why is it controversial? What are Support Vector Machines (SVM) and why are they a useful technique?

E N D

Machine learning and short positions in stock trading strategies D.E Allen, R. Powell and A. K. Singh Edith Cowan University

Reading questions • What is short selling and why is it controversial? • What are Support Vector Machines (SVM) and why are they a useful technique? • Explain what kernel estimation is. • Why are different kernel estimators available? • Explain what logistic regression is. • What does Beta Measure? • Why are Sharpe ratios a useful investment metric? • How does Beta differ from Sharpe ratios. • How do we measure mean absolute error? • Why is out of sample forecasting important?

Introduction • Forecasting future stock price movement using financial indicators. • Evidence from past for predictability power of financial factors e.g. Beta, E/P, B/M, past returns etc. • Support Vector Machines (SVM), capable of handling large amount of unstructured, noisy or nonlinear data. • SVM classification useful in prediction of future price direction (+1,-1).

SVM in Classification • SVM are characterized by • Mapping input vectors into higher dimensional feature space. • Structural risk minimization • Non linear modelling with Kernel Functions • Kernel density estimators are non-parametric density estimators with no fixed structure. They depend on all the data points to obtain an estimate. • Classification of classes using optimal separating hyperplane.

SVM Optimal Separating Hyperplane.

SVM • SVM use following kernel functions • Linear: • Polynomial: • Radial Basis Function (RBF): • Sigmoid: • Here and d are kernel parameters. • Study Uses RBF kernel for its robustness on non linear data.

Data Dow Jones Industrial Average sample Stocks’ daily data for a period of 5 years (1/03/2005-9/03/2010). Factors Used for forecasting

Methodology • Standardization of Data • Direction of price change classified into binary -1 and 1 using • Testing sample is created using last 130 days data. • Kernel parameters, cost and gamma are optimized using grid search. A systematic way of seeking optima. • The model is built on training data and is used for forecasting which is tested on out sample data (130 days) SVM results are compared with Logistic Regression results (with same training and testing data). • Simple investment strategy used to check the predicted directions

Investment Strategy Results The final net returns of the stocks are compared using the Sharpe Ratio.

Conclusion SVM classification outperforms logistic regression in classifying price direction. Simple stock trading strategy also reveals the efficiency of SVM in stock trading. Further applications can include prediction of other financial time series. SVM regression can be further tested for similar work