Download

1 / 16

160 likes | 289 Views

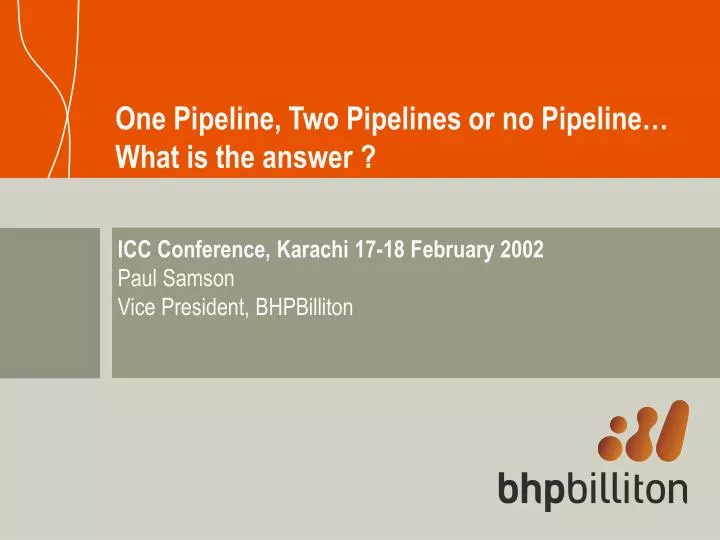

One Pipeline, Two Pipelines or no Pipeline… What is the answer ?. ICC Conference, Karachi 17-18 February 2002 Paul Samson Vice President, BHPBilliton. Outline. Pakistan Supply/Demand Options to fill the gap Iran to Pakistan Pipeline India Supply/Demand Options to fill the gap

E N D

One Pipeline, Two Pipelines or no Pipeline…What is the answer ? ICC Conference, Karachi 17-18 February 2002 Paul Samson Vice President, BHPBilliton

Outline • Pakistan • Supply/Demand • Options to fill the gap • Iran to Pakistan Pipeline • India • Supply/Demand • Options to fill the gap • Iran to Pakistan and India Pipeline • Conclusions

BCFD PAKISTAN 6000 4000 2000 Developing Existing 2000 2005 2010 2015 Pakistan: Supply & Demand Pakistan needs to add 1 Tcf/year just to replace the decline… Most Likely Demand

Pakistan – Options to fill the gap Increase the pace of exploration and development Average discovery since 1991 0.75Tcf/year

Pakistan – Options to fill the gap … if gas potential and investment are present Revised Petroleum Policy New Petroleum Policy FORECAST

Pakistan – The cost of not filling the gap @US$20/bbl DOMESTIC GAS H S F O 13% Fuel Oil 33% more 4% 8% 75% 18% 12% 14% 7% 8% 18% Foreign Exchange 67% more 22% Producer Take F&D Cost Royalty Tax GoP Equity GST T&D GST ODS Freight &Margin Imported fuel • or import gas from Turkmenistan, Iran, Qatar…

The Iran to Pakistan Pipeline Project • 0.5 to 1.5BCFD over 20 years • High CV gas • 32” Assaluyeh to AC1-X • Class 900 , x80 • MAOP 2220psig Tehran 760km 1115km CHINA $0.65b $1.25b Lahore IRAN PAKISTAN Delhi 32” NEPAL Assaluyah 32” South Pars Karachi QATAR HBJ UAE INDIA OMAN SAUDI ARABIA Arabian Sea 20°N Bombay Length 1875 km Hyderabad Total Cost $1.9b 0 500 km 60°E 80°E

BCFD 6000 4000 2000 2015 2000 2005 2010 India’s options to fill the gap Most Likely Demand New Developments Existing Production • Use domestic coal • Explore for more gas • Import fuel oil • Import LNG • Import pipeline gas from Bangladesh, Qatar, Iran

The Iran to India Project • 1.0 to 2.0BCFD over 20 years • 36” Assaluyeh to Delhi Tehran 760km 1115km 900km CHINA $1.2 $1.1b $1.5b Lahore IRAN PAKISTAN Delhi NEPAL 36” 36” Assaluyah South Pars 36” Karachi QATAR HBJ UAE INDIA OMAN SAUDI ARABIA Arabian Sea 20°N Bombay Length 2775 km Hyderabad Total Cost $3.8b 0 500 km 60°E 80°E

The Iran to Pakistan to India Project • Throughput: • 1.5 to 3.5BCFD • 3.8% pa growth • Class 900 , x80 • MAOP 2220psig • 44” to Indian border • 36”from border Tehran 760km 1115km 900km CHINA $1.10b $1.20b $1.86b Lahore IRAN PAKISTAN Delhi 44” 1-2 NEPAL 36” Assaluyah South Pars 44” Karachi QATAR HBJ UAE INDIA OMAN SAUDI ARABIA Arabian Sea 20°N Bombay Length 2775 km Hyderabad Total Cost $4.16b 0 500 km 60°E 80°E

The Value Proposition to Pakistan Delivered to ACX1 @ $18/bbl oil price Excludes any transit fees to Pakistan Imported HSFO Iran Pakistan Pipeline Gas @ Policy Price Iran Pakistan & India Pipeline FX Component

The Value Proposition to India Delivered to Delhi @ $18/bbl oil price Indifference point with imported coal for 1200MW baseload power generation based on US$30/tonne coal price LNG Current gas Market Prices Pipe Bangladesh GAIL Retail Pipe Iran

What needs to happen? • Explicit Government(s) support • Establish regulatory framework • Integrated participation of key sponsors from source to market • Update feasibility study • Enter into sales agreement with potential customers • Set up sponsors leading to consortium • Arrange financing • Execute • First gas to Pakistan: 36 months from financial closure

The Benefits Pakistan: • Affordable, unlimited supply • Internationally benchmarked compensation for transit • Abundant energy for uninhibited economic growth India: • Affordable, unlimited supply • Economic growth • Diversity of supply Iran: • Diversification from oil revenue • Long term foreign exchange earnings Regional Stability ???

Conclusions • One pipeline is better than two and much better than none… • Project fundamentals are strong • Provides long term affordable energy supply • Political hurdles can be overcome – economic incentives • There are a few visionary companies believing in the project

Role of BHPBilliton • BHPBilliton - world’s leading diversified resources company • Discovered and developed Zamzama gas field • Has been promoting gas exports from Iran since 1993 • Completed feasibility study from Iran to Pakistan in 1998 • BHPB mandated by NIOC to lead the study and execution