Download

1 / 22

230 likes | 369 Views

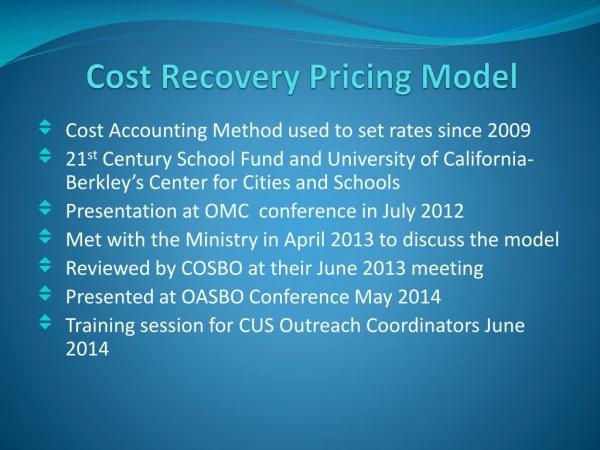

Full cost recovery an introduction. John O’Brien Community Accounting Plus. Three questions to start off…. 1. Who is paying for you to be here now? 2. How much does it cost your organisation (per hour) for you to be here today? 3. What things ‘contribute’ to this cost?. Overview.

E N D

Full cost recoveryan introduction John O’Brien Community Accounting Plus www.communityaccounting.co.uk

Three questions to start off… 1. Who is paying for you to be here now? 2. How much does it cost your organisation (per hour) for you to be here today? 3. What things ‘contribute’ to this cost? www.communityaccounting.co.uk

Overview • FCR is about activities – links to changes in charity accounting and funding arrangements • How much does it really cost you to do things? • If you don’t use FCR, what else is there? • It’s not just about grants and fees, it’s also about good management www.communityaccounting.co.uk

What do we do at CA Plus? • Preparation and independent examination of accounts • Payroll bureau • Bookkeeping • Employment advice service • Finance training • Consultancies • Administration or “support” www.communityaccounting.co.uk

Finance training • Dealing with questions by ‘phone, email • The website • One to one visits for support • One to one visits for training • Formal courses and seminars • Every Penny Counts • Consultancy www.communityaccounting.co.uk

Examples of Support Costs in CA Plus • Staff supervision, training, subscriptions • Senior staff reviewing the files, their own training, supervision, etc • The equipment used such as IT, phones etc (what about depreciation?) • Committee meetings • The heating • The audit fee • The redecoration of the office every 5 years www.communityaccounting.co.uk

Some jargon • Direct costs – costs that clearly relate to a specific activity • Support costs (overheads, shared, core etc) – costs that do NOT relate to a specific activity • Fixed costs – these don’t change if you do one more thing • Variable costs – these DO change if you do one more thing www.communityaccounting.co.uk

Marginal and Average costs • This is crucial and at the heart of this issue • Marginal cost is the cost of doing one more thing • Average cost is the cost of doing each thing. • An example ….. www.communityaccounting.co.uk

Today www.communityaccounting.co.uk

A new project www.communityaccounting.co.uk

Project B comes to an end www.communityaccounting.co.uk

What should you have charged funder D? • Funder D has only paid for ‘marginal’ cost • Total support costs were £12 before project D. They didn’t go up. • The ‘average’ cost of project D could, and should, have included an amount for support costs. • At £4, with project D, the group wins. When B closes, the group survives. • At £3, with project D, the group wins, but when B closes, the group still dies. www.communityaccounting.co.uk

So how much does it cost to do things? • The average cost of each unit of activity is simply the cost divided by the total amount of activity • If you only have one staff member and they advise 500 clients a year, it’s simply your organisation’s costs divided by 500, which will give you the average cost per client. www.communityaccounting.co.uk

If it’s complicated… • identify all your different activities • Allocate any ‘direct’ costs to each activity. This might include the salary costs of the particular staff involved, the travel costs, specific materials, specific audit costs, etc www.communityaccounting.co.uk

Think about what generates or causes the costs in each activity. (For many voluntary organisations it will be primarily the employment of staff, but you can get more complicated if you want) • Allocate the ‘support’ costs, between the activities. You can break these down into sections. This involves a choice… www.communityaccounting.co.uk

Allocating the support costs between activities • Per person • In proportion to time spent on the activity • In proportion to direct costs, floor space, funding, salary costs etc • The point is… • Be reasonable • Be consistent • Think about what generates the costs www.communityaccounting.co.uk

What can you do now you know the full cost? • If you know how much time you spend on each activity you can see the cost per hour • You can move on to ask how you finance this activity…by grants, contracts, fees, fundraising etc • If you charge fees for some services, you can see the minimum you should charge to break even. www.communityaccounting.co.uk

What can you see? • The output that might be reasonably expected for the funding • The targets for fees as well as the outputs for each activity – useful for monitoring and management • The activities that are giving you a financial problem • The activities that are keeping you solvent www.communityaccounting.co.uk

Grants & fees • It’s unusual to get grants to pay for you to go to meetings, but these are real costs that need to be covered. • Most funders want an output or even an “outcome”. • You need to make sure that all your support costs are paid for by whoever is funding the activity. This could be a grant for a project, a fee for a service, or a price for a product • If not, is this OK? www.communityaccounting.co.uk

The problem with accepting ‘core funding’ • You may think it’s good to have pure ‘core’ funding – money just to be there. But there is a risk. • It allows you to do other projects or activities in return for marginal funding, with these funders or clients not paying the ‘full cost’ • But what happens when the core funding is reduced? www.communityaccounting.co.uk

Is this all real? • There are lots of assumptions in all this • If you don’t do this, how do you know whether the income is sufficient. • If you have a financial problem, you need to know where the problem lies. www.communityaccounting.co.uk

And finally If in doubt, call it £40 an hour www.communityaccounting.co.uk