Download

1 / 10

100 likes | 226 Views

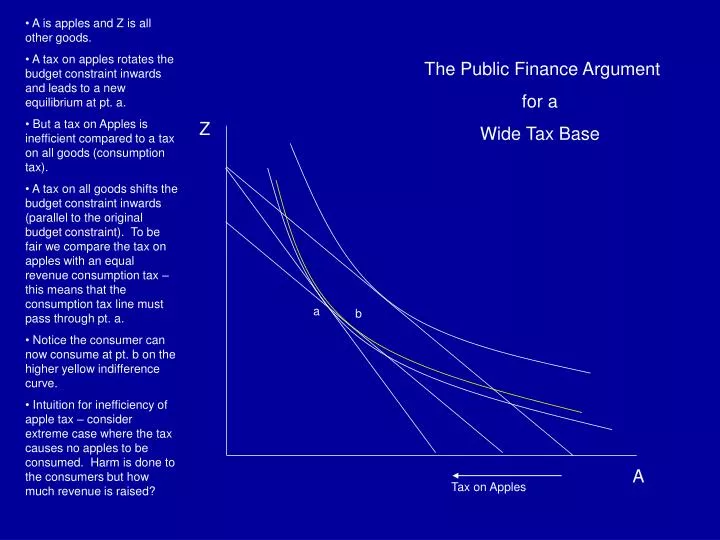

Z. a. b. Tax on Apples. A. A is apples and Z is all other goods. A tax on apples rotates the budget constraint inwards and leads to a new equilibrium at pt. a. But a tax on Apples is inefficient compared to a tax on all goods (consumption tax).

E N D

Z a b Tax on Apples A • A is apples and Z is all other goods. • A tax on apples rotates the budget constraint inwards and leads to a new equilibrium at pt. a. • But a tax on Apples is inefficient compared to a tax on all goods (consumption tax). • A tax on all goods shifts the budget constraint inwards (parallel to the original budget constraint). To be fair we compare the tax on apples with an equal revenue consumption tax – this means that the consumption tax line must pass through pt. a. • Notice the consumer can now consume at pt. b on the higher yellow indifference curve. • Intuition for inefficiency of apple tax – consider extreme case where the tax causes no apples to be consumed. Harm is done to the consumers but how much revenue is raised? The Public Finance Argument for a Wide Tax Base

Note that we can reinterpet Z and A from the previous slide in different ways. For example, A could be money income and Z leisure in which case the theory says that an efficient tax would include leisure, i.e. a lump sum tax. This is the broadest interpretation and the one that BB focus on but the logic is identical. • Key to the public finance approach is to find the tax that minimizes deadweight loss holding revenue constant. • But what kind of assumption is that! • Do you think that taxes would have been the same without the 16th Amendment to the Constitution – the income tax amendment? • When government has access to different tax bases we should assume that the amount of revenue the government will take will change. • BB assume a Leviathan government. Whatever the tax base is Leviathan will seek to maximize revenues – just like a monopolist. • BB’s assumption is analytically convenient. • True for most governments in the history of the world. • Necessary to understand why citizens may want to constraint government. It is not an objection to the Leviathan assumption, for example, to argue that the modern US government is not a Leviathan. To the extent that this is true it is true because of constitutional constraints, constitutional constraints that we want to explain.

First implication of the Leviathan model. Lump sum taxes are the worst! If Leviathan can lump sum tax, Leviathan will take everything beyond bare subsistence. • What happens if Leviathan is constitutionally constrained to money-income taxation only? What is the maximum that Leviathan can take?

L Y L is leisure and Y is money income. When Leviathan cannot tax L the maximum tax revenue is Max. Tax. Why? Taxpayers are much better off than when lump-sum taxation is available. Note that Max. Tax is available only with a regressive tax. Leviathan must tax at the rate given by the slope of the Im indif. Curve. Interesting result: Regressive taxes are revenue maximizing! (Application to IO.) What happens if Leviathan is restricted to a proportional (flat tax) on money income? La Im Ym Ya • Max. Tax

L Y • A proportional tax rotates the budget line inwards. Thus find the “price consumption curve,” all the equilibrium pts for any tax. • Now find the proportional tax that raises the most revenue. • The most revenue that can be raised is Ya-Yp. • With tax rate (Ya-Yk)/Yk. • To avoid clutter we don’t show this but the revenue raised by the proportional tax will be less than the revenue raised by the optimally regressive tax. • Thus the tax constitution may want to include restrictions on regressivity. La PCC k Yp Ya Yk

Optimal Commodity Taxation: The Public Finance View • As usual the public finance perspective says optimal commodity taxation occurs when dead weight loss is minimized for a given revenue constraint. • Under some simplifying assumptions it can be shown that this implies that commodity tax rates should be set proportional to inverse elasticities. The Ramsey Rule. • First we derive an expression for deadweight loss in the simplified case where supply is perfectly elastic (constant returns to scale) and when demand curves are independent. DWL=½ ΔP*ΔQ =½ (tax amount)*ΔQ =½ (tax rate)*P*ΔQ ε=(ΔQ/Q)/(ΔP/P) Thus, ΔQ= ε*ΔP/P*Q =ε*(tax rate)*Q So DWL=(½ tax rate*P)*(ε*(tax rate)*Q) Or DWL=½ (tax rate)² *ε*pQ DWL Tax Amount =ΔP S ΔQ

Traditional View (con’t) DWL=½ (tax rate)² ε*pQ • Notice that DWL increases with the square of the tax rate so DWL is increasing at an increasing rate. Thus to minimize dead weight loss we will want to spread the tax across many commodities. • Also note that DWL is larger the higher is ε so we will want to tax low elasticity commodities (ε<1) more than high elasticity commodities (ε>1). • We can make the last point a bit more precise. We want to minimize DWL subject to a revenue constrant. E.g. consider two commodities then we want to: Min. (½ (t1)² ε1*p1Q1) + (½ (t2)² ε2*p2Q2) s.t. (ReqRev - t1*p1Q1 - t2*p2Q2 = 0)

From a Lagrangian: L=½ (t1)² ε1*p1Q1 + ½ (t2)² ε2*p2Q2 + λ(ReqRev - t1*p1Q1 - t2*p2Q2) FOC: t1 ε1 p1Q1- λp1Q1=0 t2 ε2 p2Q2- λp2Q2=0 Or t1 = λ/ε1 t2 = λ/ε2 The inverse elasticity version of the Ramsey rule.

Optimal Commodity Taxation: The Public Choice Perspective • The public finance view assumes that government has a fixed revenue constraint and that it will tax commodities using the Ramsey rule to minimize dead weight loss. • If instead government is a Leviathan it will act like a monopolist – it will tax low elasticity commodities more than high elasticity commodities (for the same reason that a monoplist charges more for goods with low elasticity demands) but it will maximize revenues not minimize dead weight loss. • It follows that it may be desirable to prevent Leviathan from taxing goods with inelastic demands! The opposite conclusion of the public finance perspective.

Should we have a Balanced Budget Amendment? • Public Finance: To minimize dead weight loss you want to spread taxes across many commodities. The same idea holds over time – to minimize dead weight loss you want to spread taxes across many time periods. Thus, the conventional public finance view says that debt finance can be a good things especially for extraordinary expenditures such as wars. • (There is also a Keynesian argument that budget deficits are necessary to stimulate the economy in times of recession.) • But wake up! We have had budget deficits almost continually since 1969. Deficits appear not to be used to smooth taxes but to reduce the apparent costs of spending (Democrats) or tax decreases (Republicans). • Budget deficits can also occur without fiscal illusion. Imagine a time of ideological division. A government that rules today may not rule tomorrow. By spending today and running up a debt, today’s government can constraint tomorrow’s government. More spending on defense today, for example, can mean less social spending tomorrow – and vice-versa. • Prediction – ideological divisive times and countries will see larger budget deficits. • Note that from behind a veil of ignorance all voters, even ideologically divided voters, would want a balanced budget rule. • What to do about occassional high expenditures?