Download

1 / 13

150 likes | 298 Views

SOCIAL SECURITY. Mandatory spending vs. discretionary spending. Discretionary spending: Congress can adjust the amount spent on different programs through changes in annual appropriations bills. Mandatory spending: the federal government is legally required to spend the money. New Deal.

E N D

Mandatory spending vs. discretionary spending • Discretionary spending: Congress can adjust the amount spent on different programs through changes in annual appropriations bills. • Mandatory spending: the federal government is legally required to spend the money.

New Deal • Social Security was founded in 1935 as part of the Franklin D. Roosevelt Administration’s New Deal • Provides financial assistance to senior citizens, people with disabilities, and children whose wage-earning parents have died (the original intention was to take care of “widows and orphans”)

Entitlement program • Social Security is an entitlement program. Everyone who is eligible is legally entitled to receive benefits regardless of their means (even if they don’t need the money for their retirement/survival) – this differs from means-tested programs such as welfare. • The amount of benefits is determined by a formula, and the amount determined by the formula is legally required to be paid out. • Social Security and Medicare accounted for 36% of federal spending in 2011.

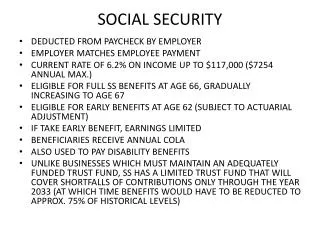

Payroll tax • Social Security is funded through a payroll tax. • Up to $110,000 of your income is subject to this tax. • Your employer pays 6.2% of your income in payroll taxes. • 4.2% of your income is deducted in payroll taxes – normally, it’s an even split but the worker share was reduced during the GW Bush Administration as part of their tax cut package • 1.45% is deducted from each side to fund Medicare • If you’re self-employed, you pay the whole thing yourself.

Trust fund • Workers pay in • 85% goes to retirement trust fund • 15% goes to disability trust fund • Retirees collect • 55 million current recipients • You can begin to collect at age 62, but can’t collect full benefits until later • Benefit level is based on what you paid in, based on your average income over 35 years of your career • Higher-income workers eventually collect higher SS benefits • Because of Cost-of-Living Adjustments and interest, you get out more than you paid in

Benefit levels • Average Social Security monthly benefit is $1230 as of 2012. • Supplemental Security Income (SSI) for those with disabilities who are unable to work • Maximum federal SSI benefit is $698 per month for an individual and $1048 for an eligible couple; states may supplement this with their own moneyNever intended to be your sole source of retirement income • Social Security benefits are not subject to federal income tax unless your income is above a certain level • The practical effect of this is that if SS is your primary source of income, you don’t pay federal income taxes

Trust fund surplus The program currently takes in more than it pays out. • The trust fund currently contains $2.5 Trillion. • BUT this money is borrowed from to fund other federal programs (makes the deficit look smaller than it actually is) • And there’s another problem…

Baby boomers • 76 million Americans born 1946-1964 • In the recent past, all of these people were at the peak of their earning capacity and paid large amounts into the trust fund over time • First boomers turned 65 in 2011 and are now drawing benefits (even though some of them are still working and paying into the system) • Eventually, this large group of people will be drawing benefits out instead of paying in.

When is the system going to run out of money? • Without changes, the system will no longer be able to pay full levels of benefits after 2033 • Without changes, the Medicare system will no longer be able to pay benefits after 2034 • Without changes, the retirement system will no longer be able to pay benefits after 2036

The problem • Fixing Social Security requires short-term pain (raising taxes) for long-term gain (benefits that won’t be realized for decades) • It’s easier for politicians to do nothing and kick the can down the road for future generations to solve. • The bad news: It’s YOUR problem. • The good news: You have 25 years to figure out how to fix it.

How to save it • Raise age at which you can begin to collect full benefits • Born prior to 1942: age 65 • 1943-1954: age 66 • Gradual increase to age 67 for those born in 1960 or later • May eventually be increased to age 70 • Raise/eliminate cap on amount of income subject to payroll tax (Bill Gates only pays payroll taxes on the first $110,000 of his income)

Alternatives • Privatization: Proposal by GW Bush and others to allow people to pay less into the SS trust fund and more into private individual retirement accounts that could be invested in the stock market • Potential for much greater return on investment than SS pays out • What if the stock market goes down? (This proposal hasn’t been discussed much since the recession began in 2008)